Thahbib Rahman

Research Analyst

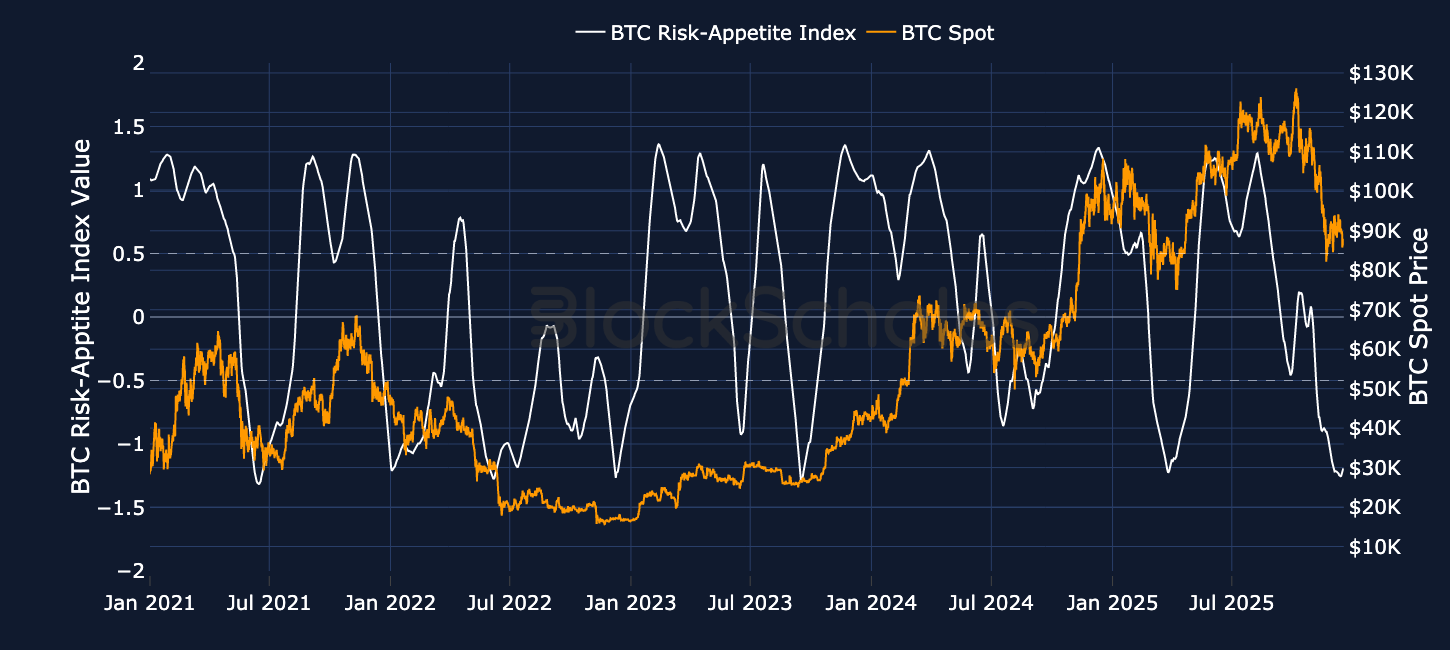

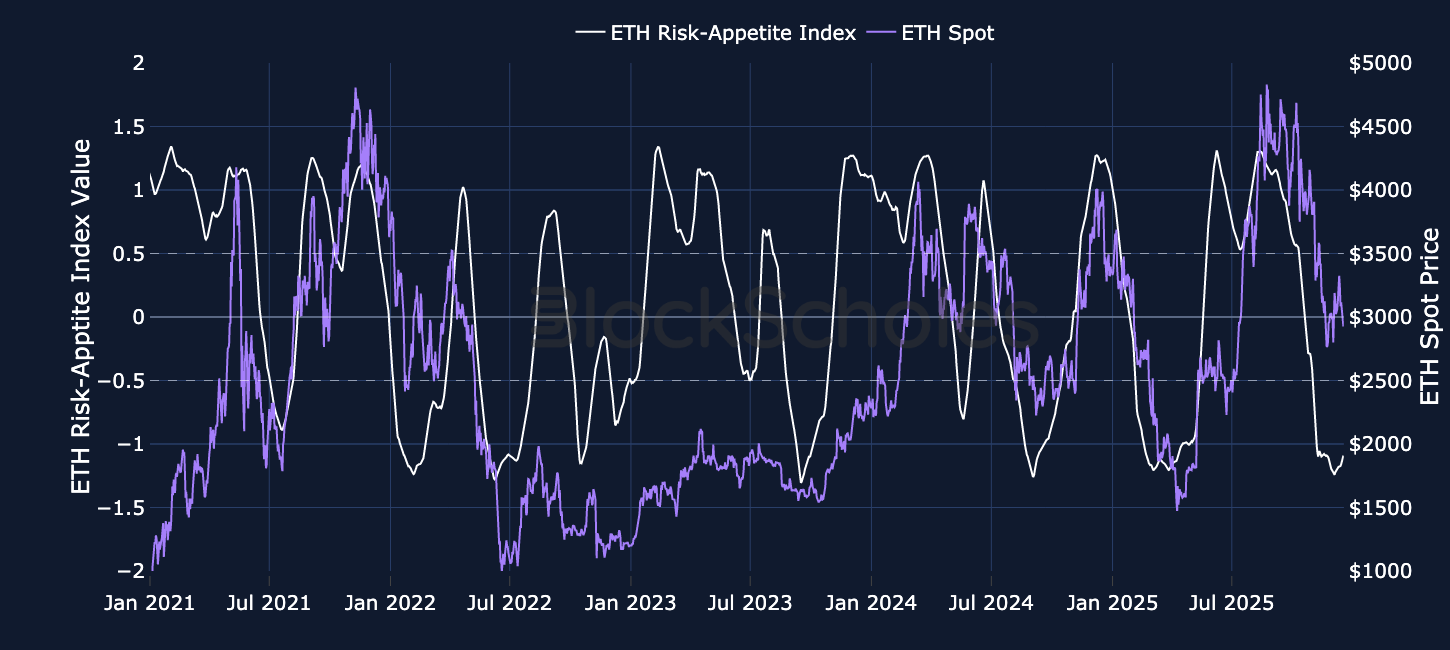

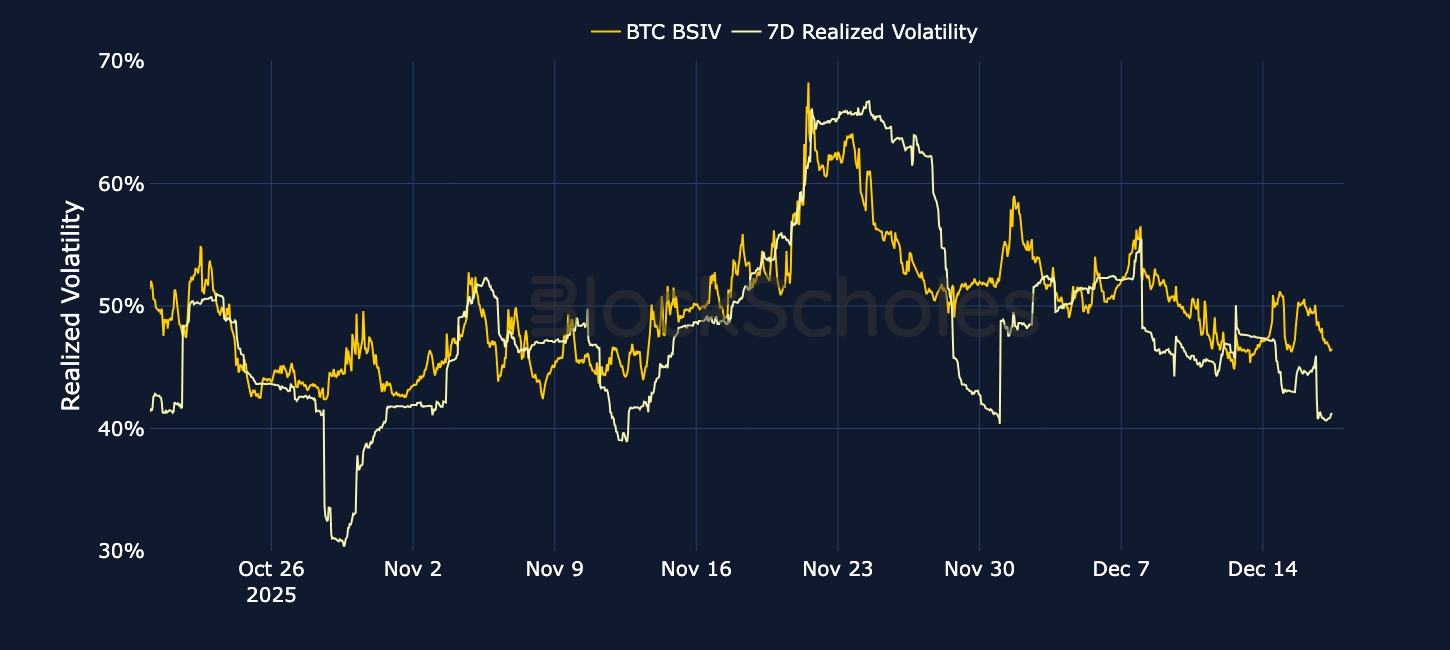

Despite the Fed delivering their third consecutive cut to interest rates as was widely expected on Dec 10, 2025, and subsequent labor market data showing that US unemployment had ticked up to its highest level since September 2021 at 4.6%, sentiment in crypto remains at extreme lows. BTC and ETH remain 30% and 40% below their 2025 high water marks, and seem unable to sustain any meaningful recovery rally for longer than 24 hours. As a result, participation levels in derivatives markets remain low, with subdued levels of trade volumes and a drop in volatility expectations. What positioning does remain is bearish, with a skew of volatility smiles towards puts suggesting strong demand for put options at expiries well into the new year.

Despite the Fed delivering their third consecutive cut to interest rates as was widely expected on Dec 10, 2025, and subsequent labor market data showing that US unemployment had ticked up to its highest level since September 2021 at 4.6%, sentiment in crypto remains at extreme lows. BTC and ETH remain 30% and 40% below their 2025 high water marks, and seem unable to sustain any meaningful recovery rally for longer than 24 hours.

As a result, participation levels in derivatives markets remain low, with subdued levels of trade volumes and a drop in volatility expectations. What positioning does remain is bearish, with a skew of volatility smiles towards puts suggesting strong demand for put options at expiries well into the new year.

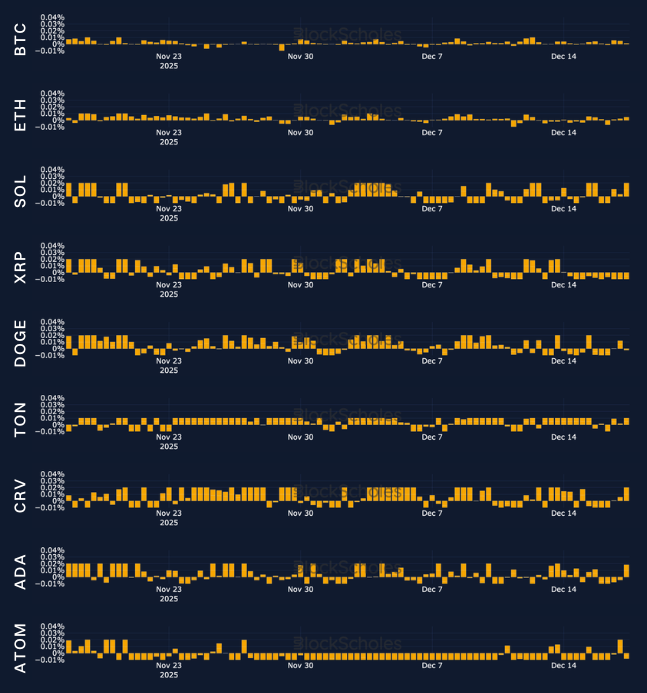

Block Scholes’ Risk Appetite Index measures the level of euphoria (above 1) or panic (below -1) in the spot market. Momentum in this index shows a strong relationship to spot returns.

The Energy Web Chain (EWC) is an EVM-compatible Layer-1 blockchain designed to enable digital coordination across the global energy sector. It operates with its own validator set, independent state and ledger, and a native Proof-of-Authority consensus mechanism, with an average block time of approximately 5 seconds. The network is purpose-built for energy market participants such as utilities, grid operators, renewable asset owners, EV charging providers, and consumers, providing shared infrastructure to support decentralisation, and digitisation of energy systems with a strong emphasis on reliability, governance, and regulatory compatibility.

EWC is fully Ethereum Virtual Machine compatible, allowing developers to deploy standard smart contracts while remaining interoperable with existing Ethereum tooling. Network activity is predominantly machine-to-machine rather than user-to-user, with the blockchain functioning as a coordination layer for energy infrastructure. Such use cases include EV chargers and vehicles authenticating before charging, proving identity and permissions to provide grid services, and renewable assets registering credentials or reporting status updates. EWC is also used to anchor off-chain data, and coordinate secure messaging between energy systems, enabling automated interaction between machines and operators without central intermediaries.

Consensus on Energy Web Chain is maintained by around 30 active permissioned validators, primarily consisting of utilities, grid operators, energy companies, and energy-focused technology providers. Energy Web Token (EWT) is the native token of the network, with a fixed maximum supply of 100M tokens, and is used to pay transaction fees and interact with smart contracts.

Although EWT is used for staking, validators do not participate in a Proof-of-Stake mechanism. Instead, EWT staking supports decentralised software services on the Utility Layer, where authorised community members, known as Patrons, stake EWT to back Service Providers operating nodes that deliver identity, messaging, and other core services. Providers and their supporting Patrons can earn rewards when services are delivered quickly, reliably, and securely, with staking designed to align incentives around service quality rather than consensus.

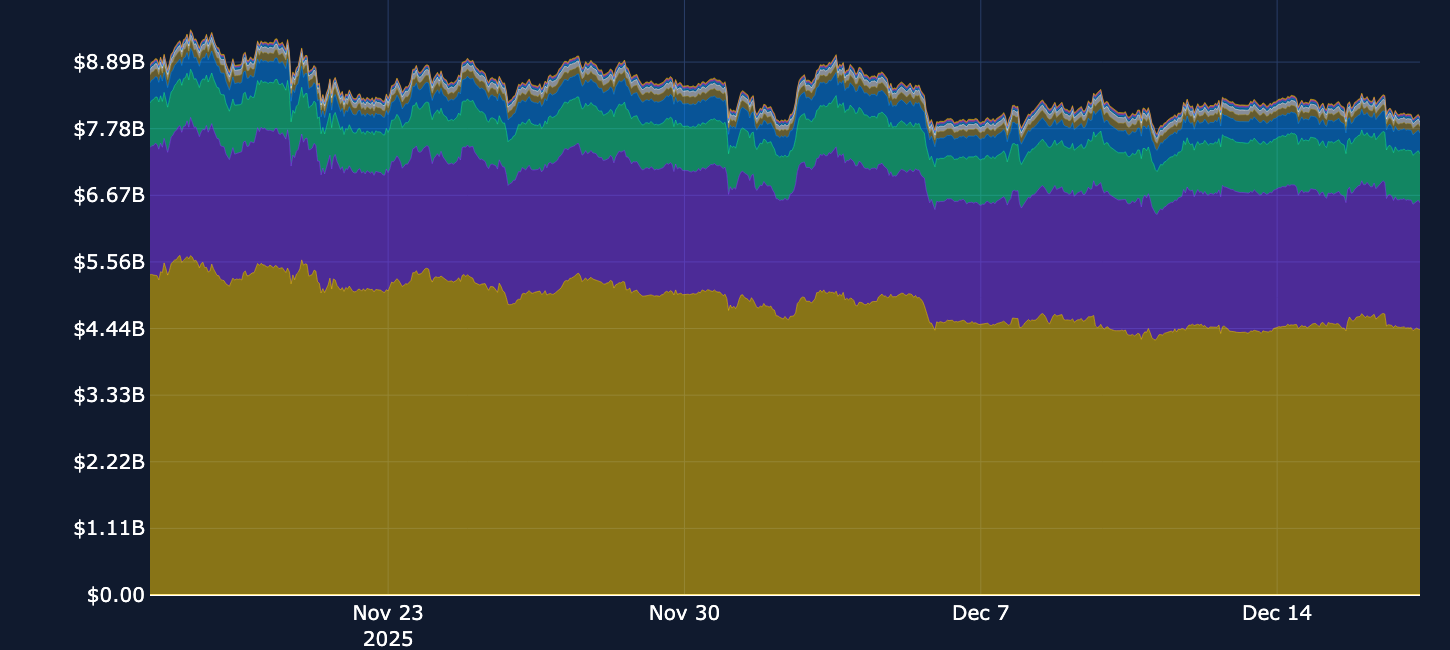

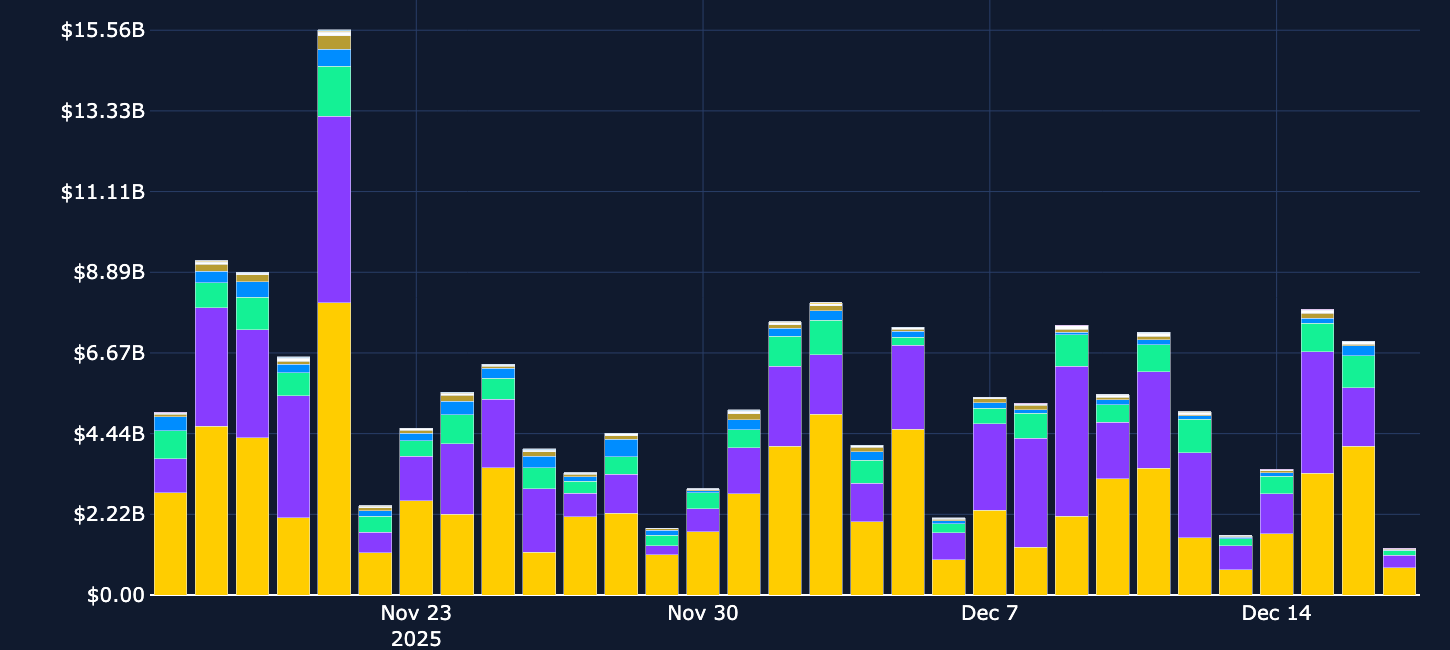

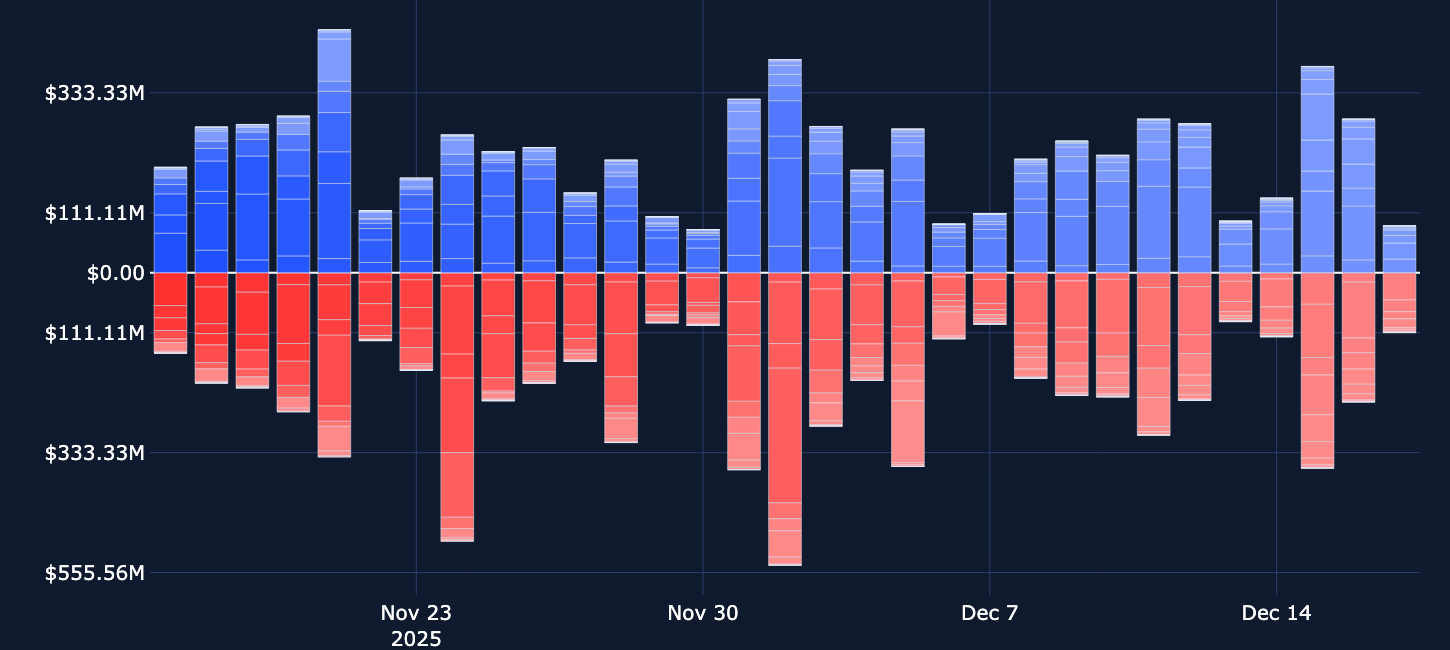

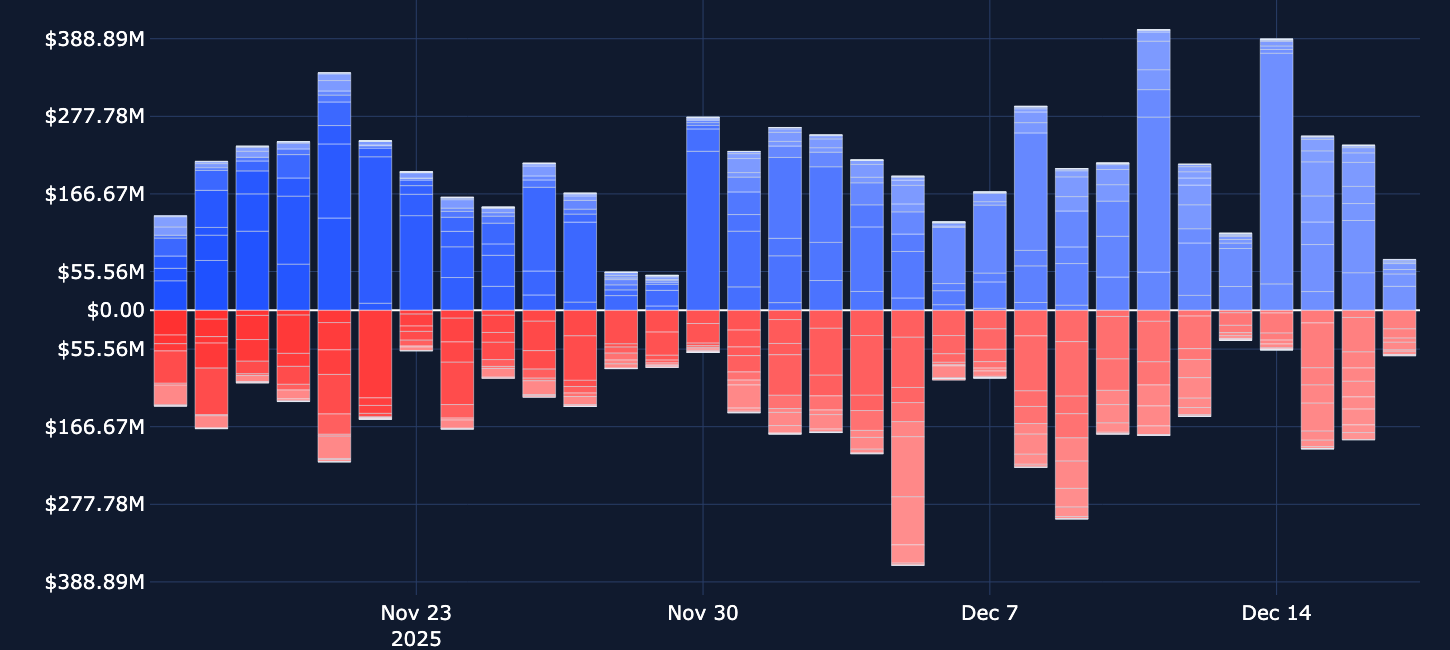

Open interest levels have moved sideways as tokens across crypto markets fail to sustain any meaningful recovery rally before returning to lower levels. BTC trades around $87K and ETH below its psychological $3K level, about 30% and 40% below their 2025 highs respectively. Altcoins have fared worse, despite the launch of the first altcoin Spot ETF products in the US. As a result, we see low levels of participation and position-taking across derivatives markets, a matter likely exacerbated by the arrival of the Christmas period without any signs of the “Santa Rally” that many may have hoped for.

Funding rates continue to paint a different picture to other measures of sentiment, such as options markets activity and ETF inflows. BTC’s funding rate has been charged to short positions in only two 8-hour windows since Nov 29, 2025. Since that date, BTC spot price has moved mostly sideways with each recovery rally matched by a subsequent sell-off in each case. Altcoin funding rates, however, have been far more changeable and reflect the extra volatility that they have experienced over the last two weeks.

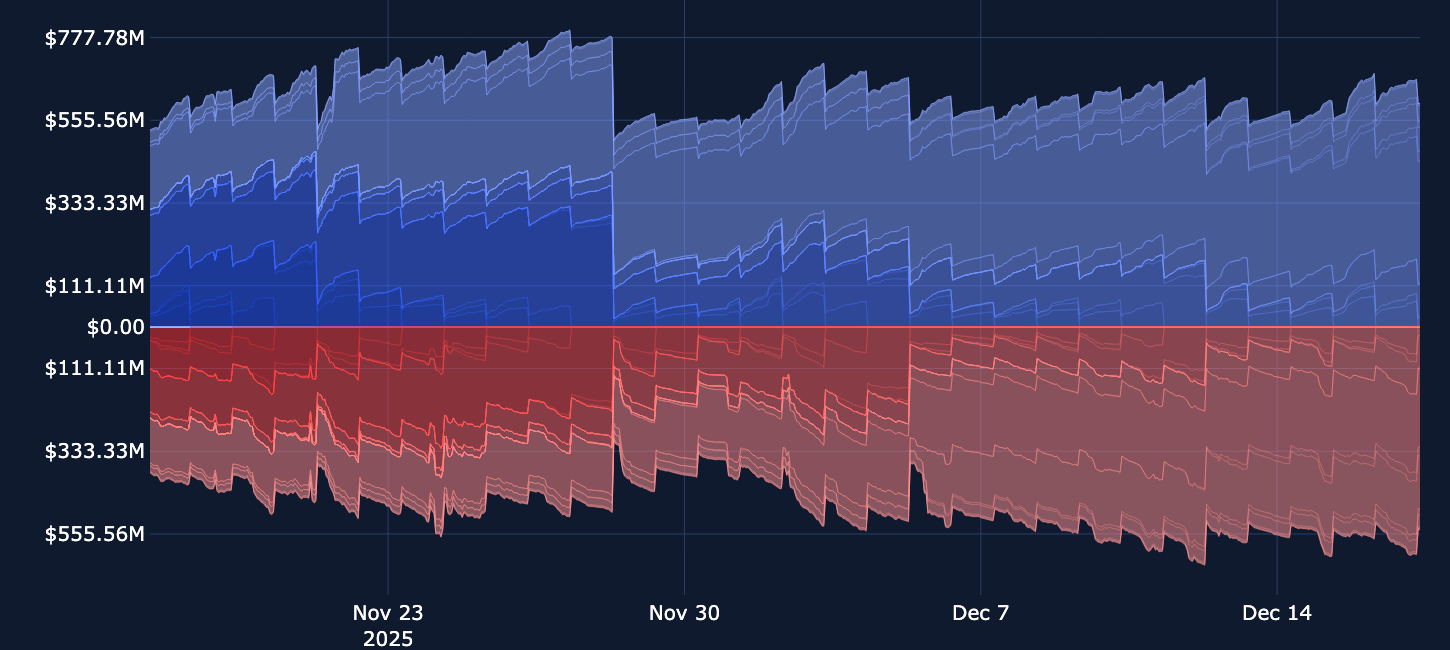

This information, coupled with almost no change in the levels of open interest in perpetual swaps, indicates a far lower level of position-taking and participation than we have seen for most of 2025 across all tokens.

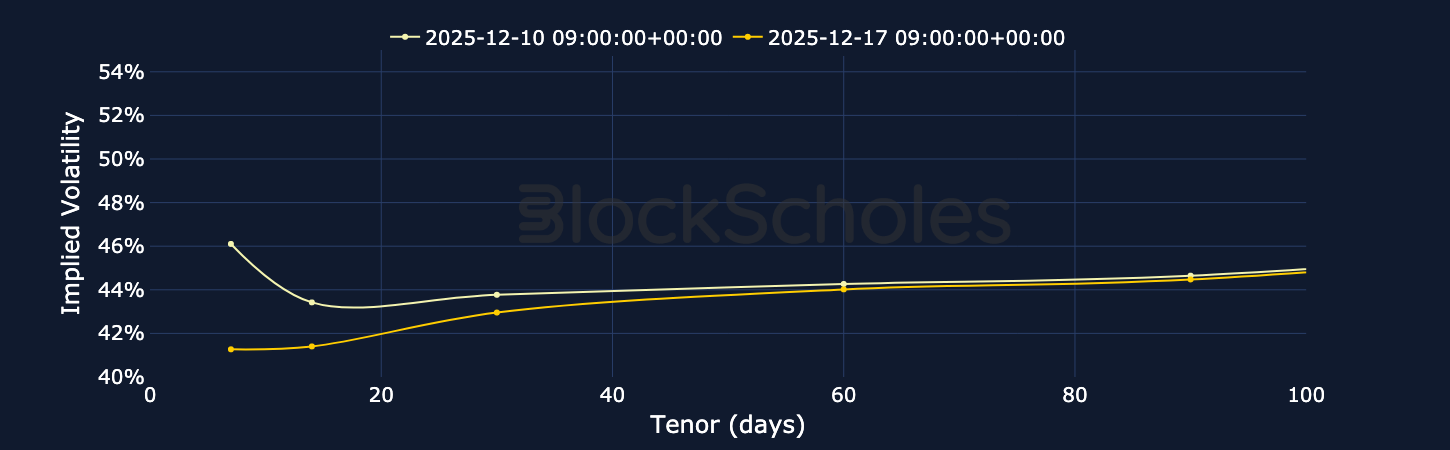

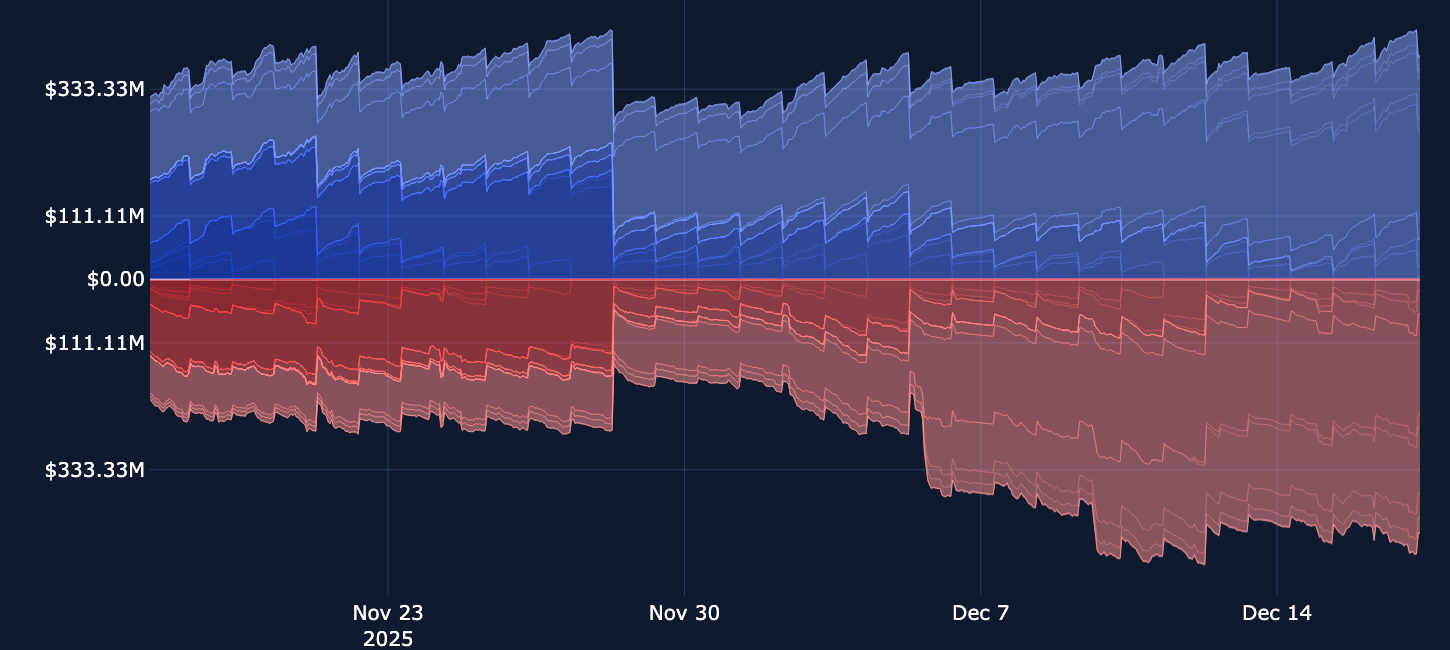

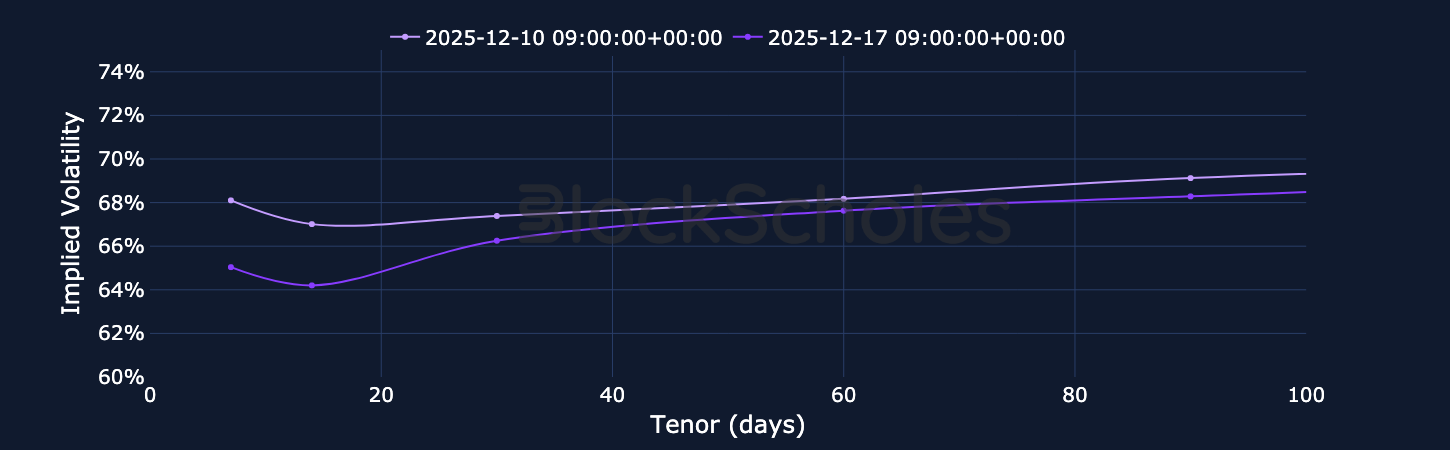

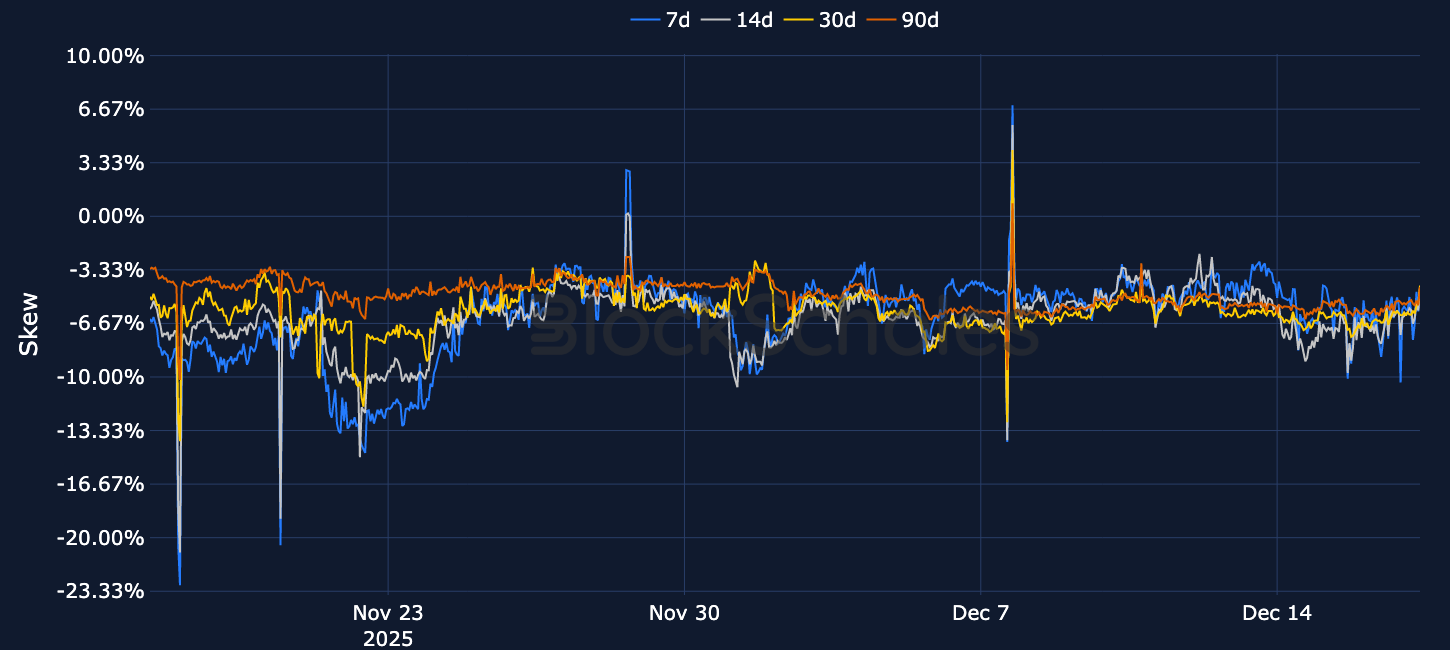

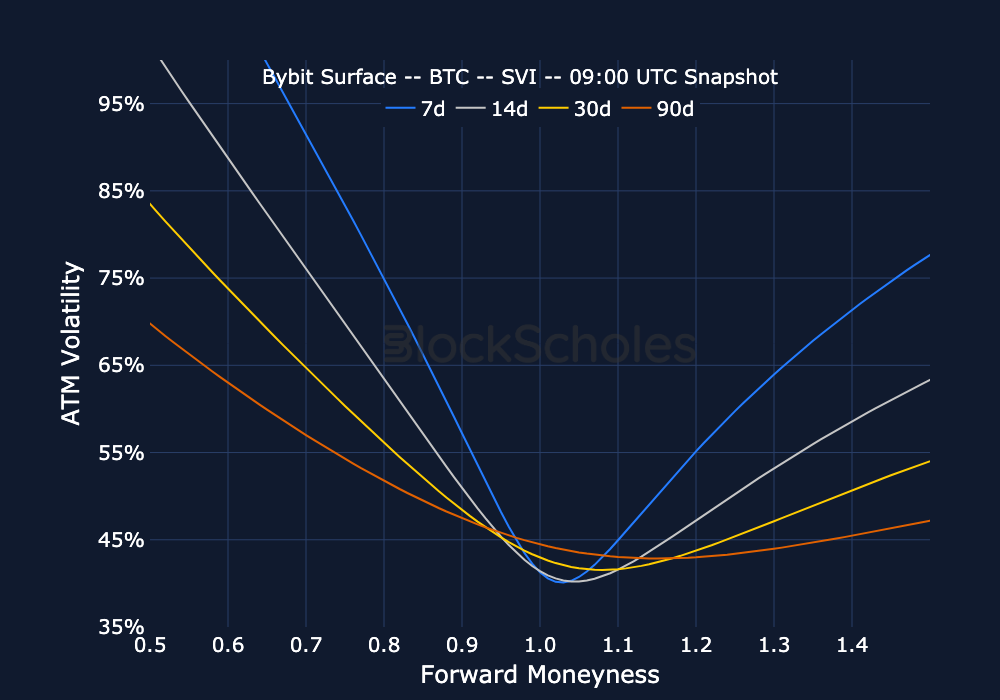

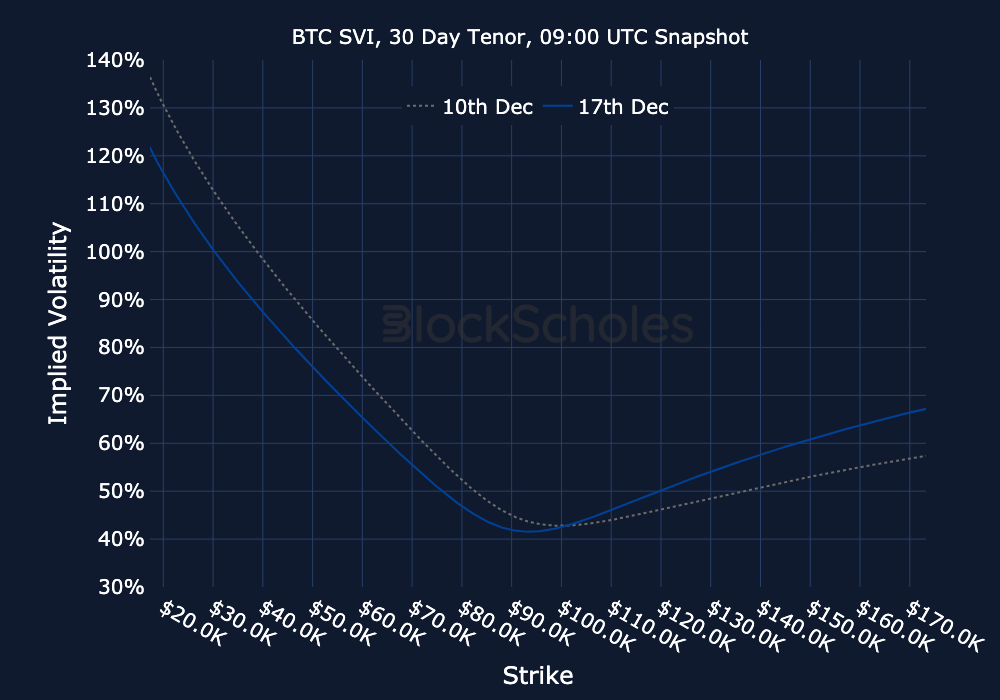

BTC Spot ETFs have seen $634.8M in outflows in the last two days alone, matching the dismal sentiment in spot that has seen BTC give up its recovery rally gains and trade at $87K. Derivatives markets reflect no real hopes of a late 2025 Santa rally, as open interest in call options remains unchanged and volatility smiles skew significantly towards put options. Volatility expectations remain elevated alongside realized volatility levels, but with a far steeper term structure of at-the-money volatility that shows no signs of exposure-taking in the short term.

The bearish positioning reflects movements in spot price, but is at odds with macroeconomic conditions that saw the Federal Reserve cut interest rates for a third consecutive meeting on Dec 10, 2025, and recent weak labor market data, with unemployment in the US rising to its highest level since September 2021 at 4.6%.

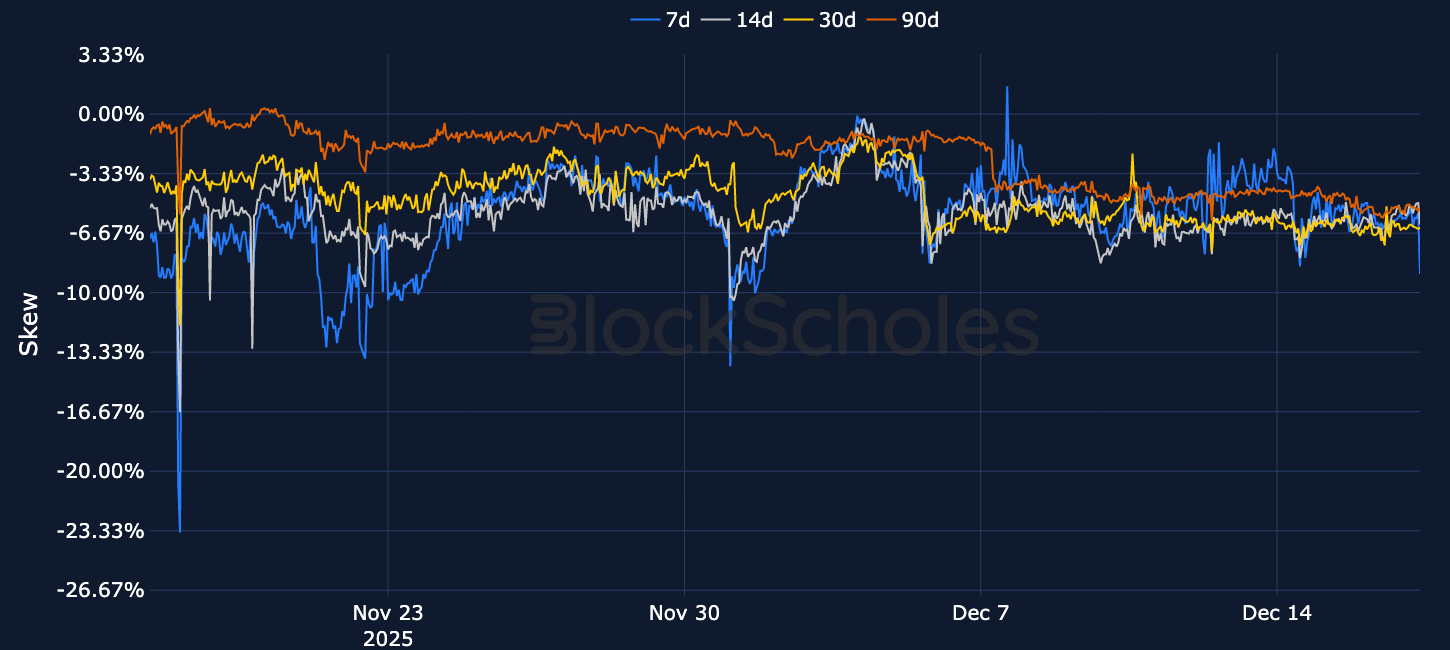

Open interest in put options has grown at pace to outweigh the open interest in call options, as traders have looked to protect against further downside over the Christmas period. This is reflected in the skew of volatility smiles towards puts, further indicating the increased relative demand for put options.

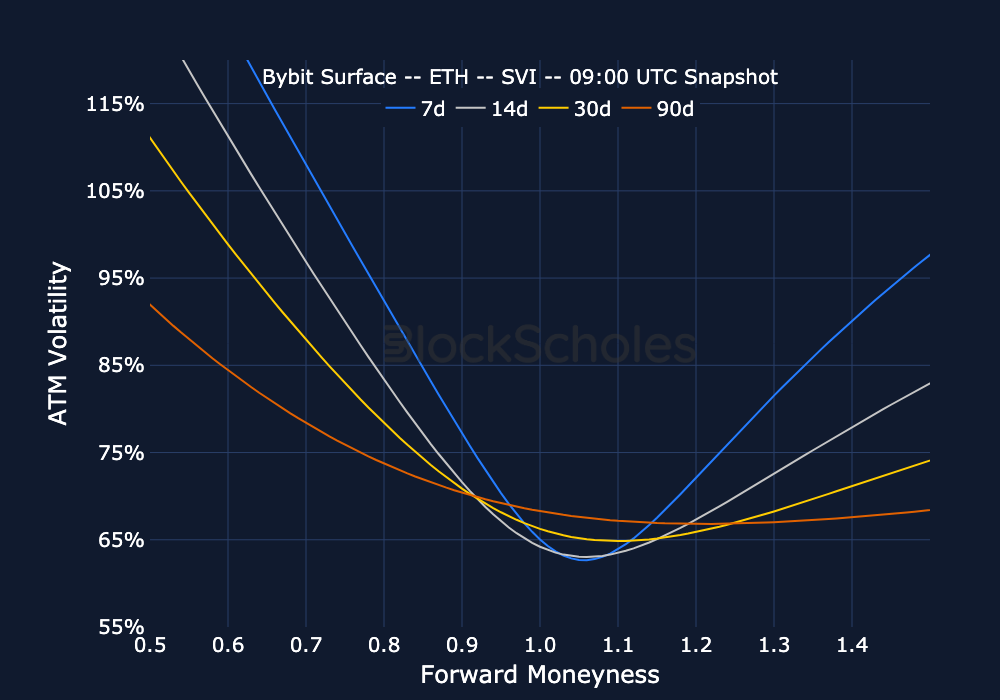

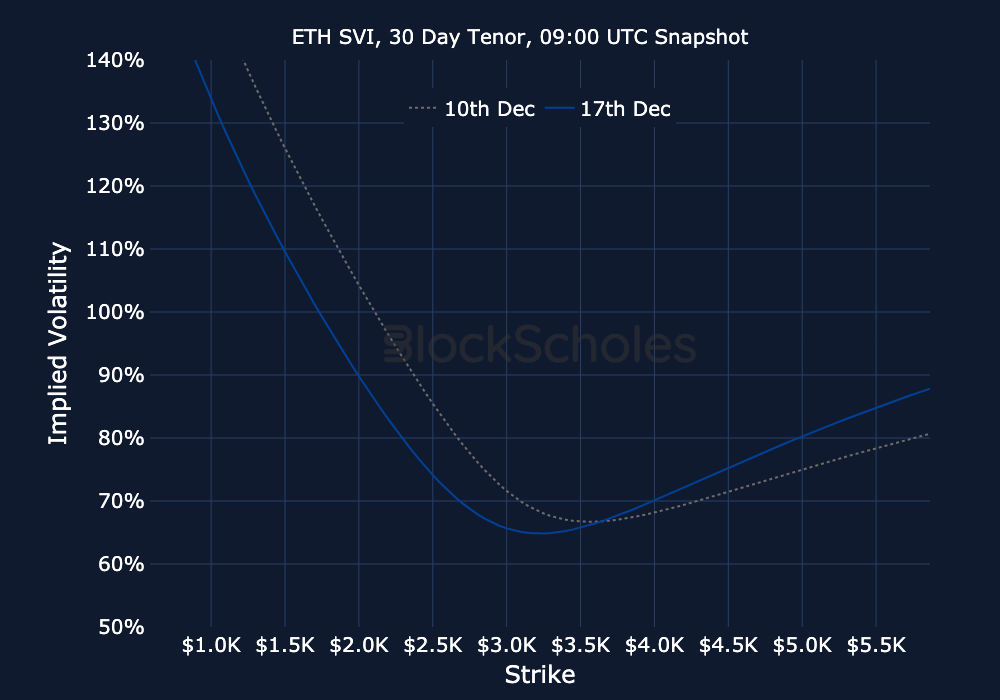

However, implied volatility has reversed its most extreme levels seen in the midst of the late-November sell-off, particularly at short tenors. Therefore, as ETH’s spot price trades sideways and struggles to sustain any meaningful recovery rally, derivatives markets are bracing for further downside rather than seeking exposure to an explosive move higher. This sentiment reflects that of ETH spot ETFs, which have seen $510M in outflows over the last four consecutive trading days.

Volatility smile skews for all tokens have held a consistent skew towards OTM puts that is present across all tenors, as both BTC and ETH markets are pricing puts at more than a 6 point volatility point premium. This is in contrast to the funding rates of their perpetual swap tokens, which do not show signs of clear directional sentiment.

The bearishness in options markets, coupled with signs of low positioning in other derivatives metrics, is likely a reflection of traders expecting spot prices’ slow, sideways slog to continue in the near future, rather than pricing-in a specific upcoming event risk.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)