Thahbib Rahman

Research Analyst

An outsized shock in Japanese government bonds that coincided with a similarly extreme move in longer-dated US Treasuries has seen risk-on sentiment in US equities, and crypto alike, lower. However, the move in crypto has not been anywhere near as cataclysmic as sell-offs as recently as the Oct 10, 2025 liquidation cascade. While major altcoins have underperformed BTC despite idiosyncratic catalysts, derivatives markets do not show marked increase in bearish positioning nor a meaningful pick-up in implied volatility.

An outsized shock in Japanese government bonds that coincided with a similarly extreme move in longer-dated US Treasuries has seen risk-on sentiment in US equities, and crypto alike, lower. However, the move in crypto has not been anywhere near as cataclysmic as sell-offs as recently as the Oct 10, 2025 liquidation cascade. While major altcoins have underperformed BTC despite idiosyncratic catalysts, derivatives markets do not show marked increase in bearish positioning nor a meaningful pick-up in implied volatility.

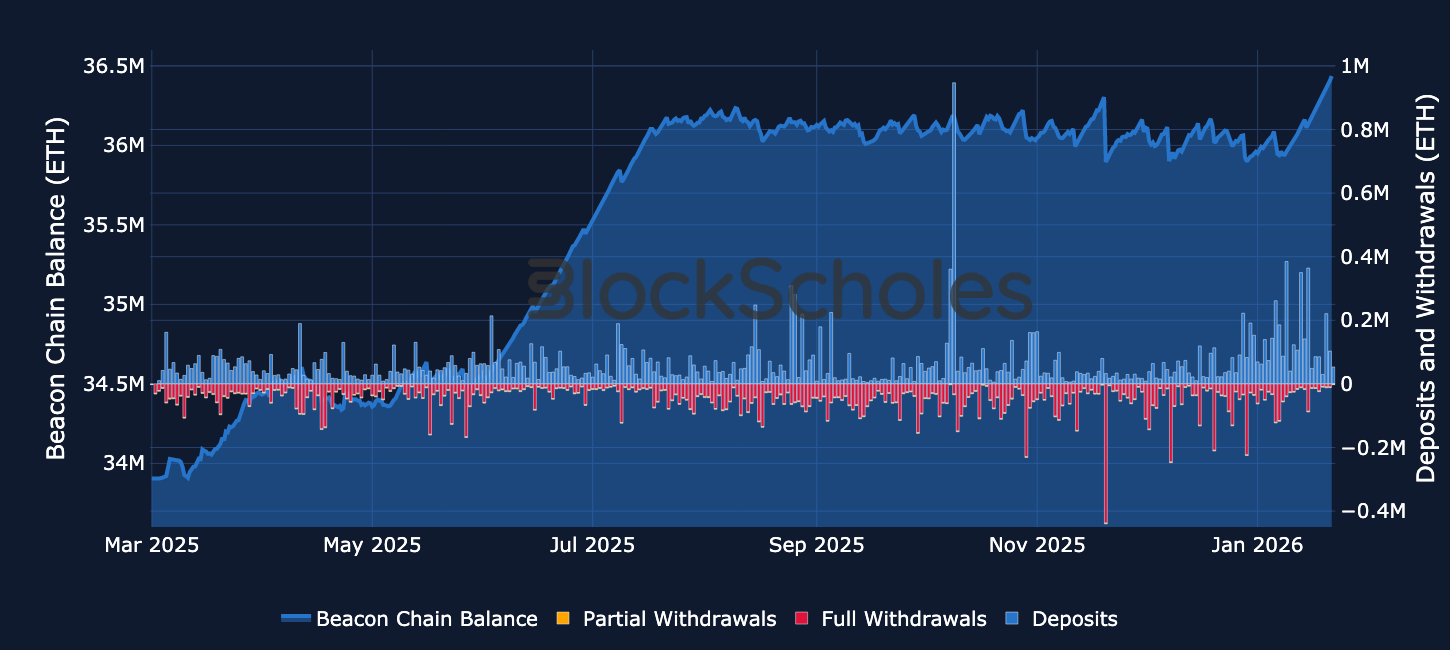

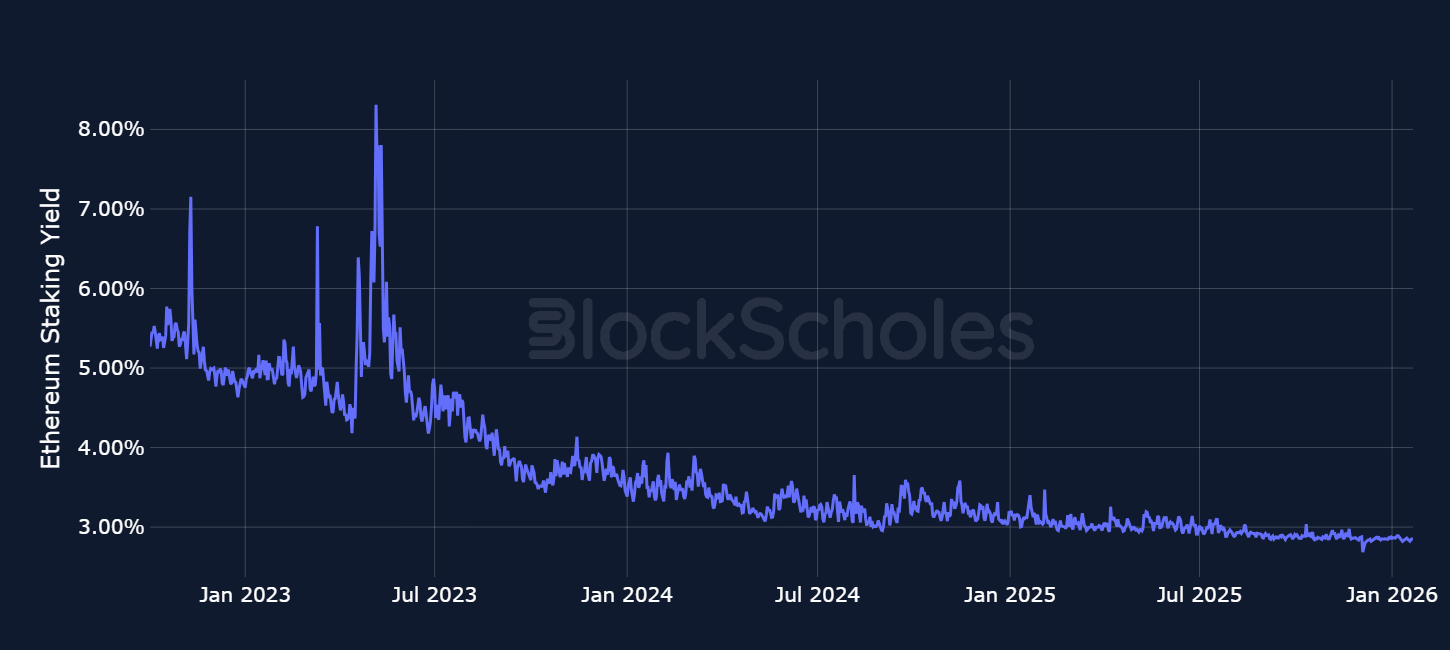

Despite a choppy macro backdrop, staking activity in Ethereum continues to see increased institutional demand – DAT heavyweights BitMine have staked more of their stockpile (3.5% of circulating supply) and applications for staking-enabled ETH ETPs are supporting staking demand. But while the Beacon chain balance is set to grow considerably, staking yields are drifting below 3% as total active stake rises. Increased supply of staked ETH adds to Ethereum network upgrades aimed at cheapening blockspace, meaning higher L1 throughput is bullish for network usage but not a clear catalyst for higher staking returns.

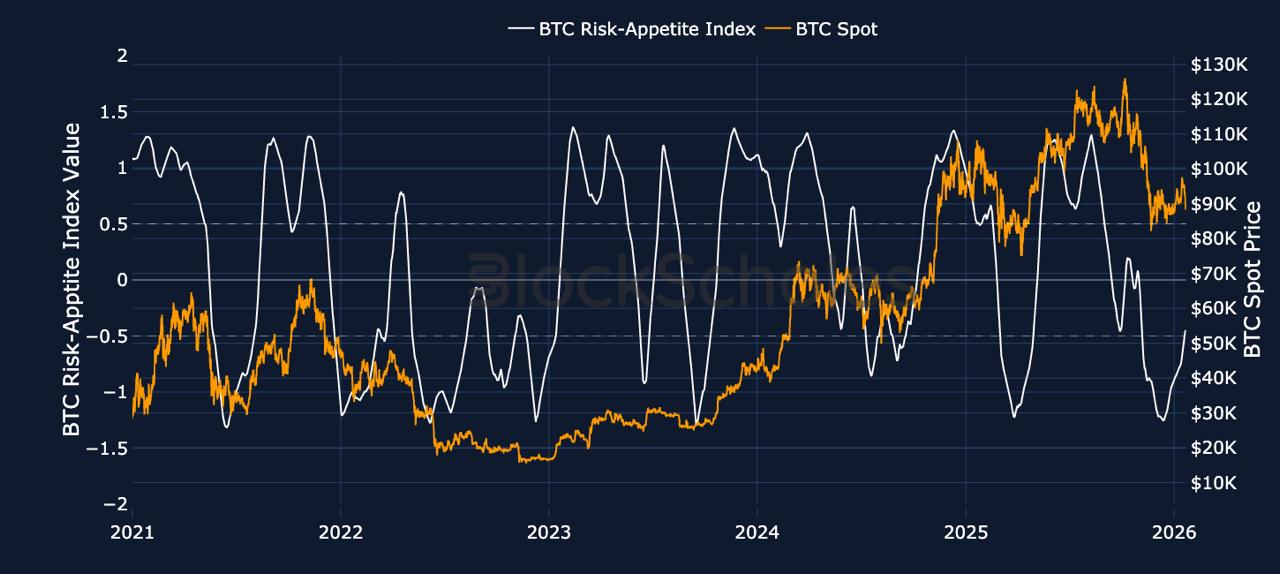

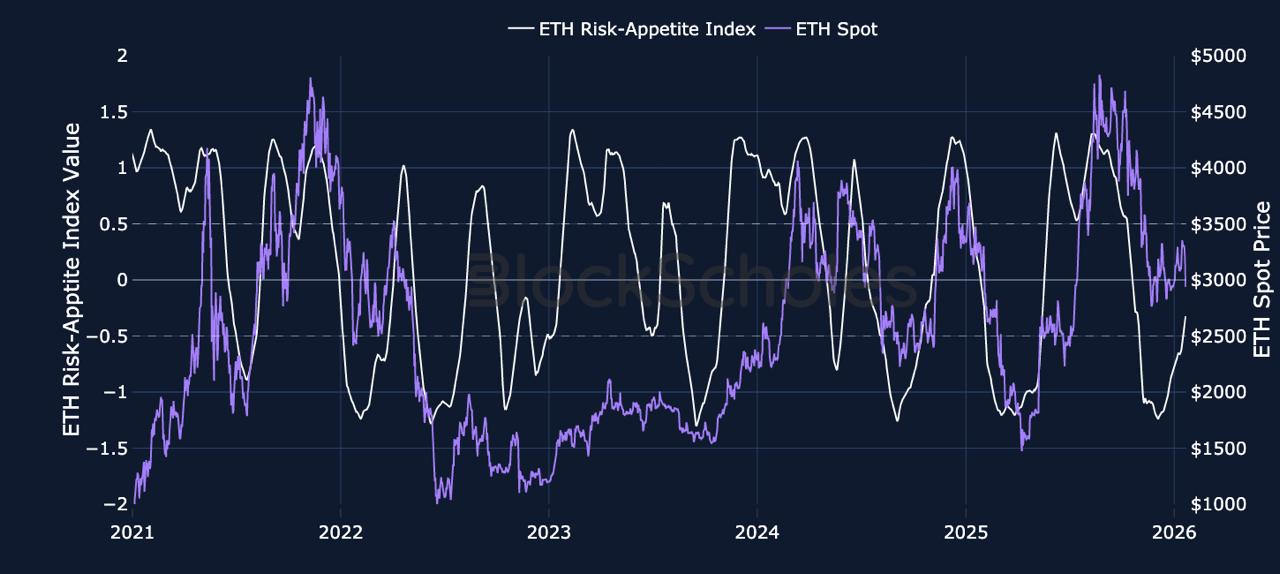

Block Scholes’ Risk Appetite Index measures the level of euphoria (above 1) or panic (below -1) in the spot market. Momentum in this index shows a strong relationship to spot returns.

Geopolitical tensions have impacted risk sentiment in crypto markets over the past week. A reignition of tariff tensions between Europe and the US over the acquisition of Greenland – as well as what Treasury Secretary Scott Bessent referred to as a “six standard deviation” move in Japanese government bond (JGB) markets – has seen BTC fall from $97K to $87K, while ETH now trades below the $3K psychological threshold at $2,700.

US equities also moved lower coinciding with BTC’s revisit to $90K. The S&P 500 declined 2% on Tuesday’s trading session. However, overall we see evidence that the selloff has mostly been contained, with the extreme moves so far being limited to US-Japan bond markets.

One factor that partly explains why the selloff in BTC has so far been relatively contained is the massive decline in leverage in crypto markets post Oct 10, 2025.

Over the past 24 hours, open interest in perpetual futures contracts for BTC have declined close to $400M, but total open interest across the altcoins we track is still more than half of pre-Oct 10 levels. Since that liquidation event more than three months ago, many retail traders have shown little appetite to take on leveraged positions anew, mitigating the impact of further liquidation-cascade driven selloffs.

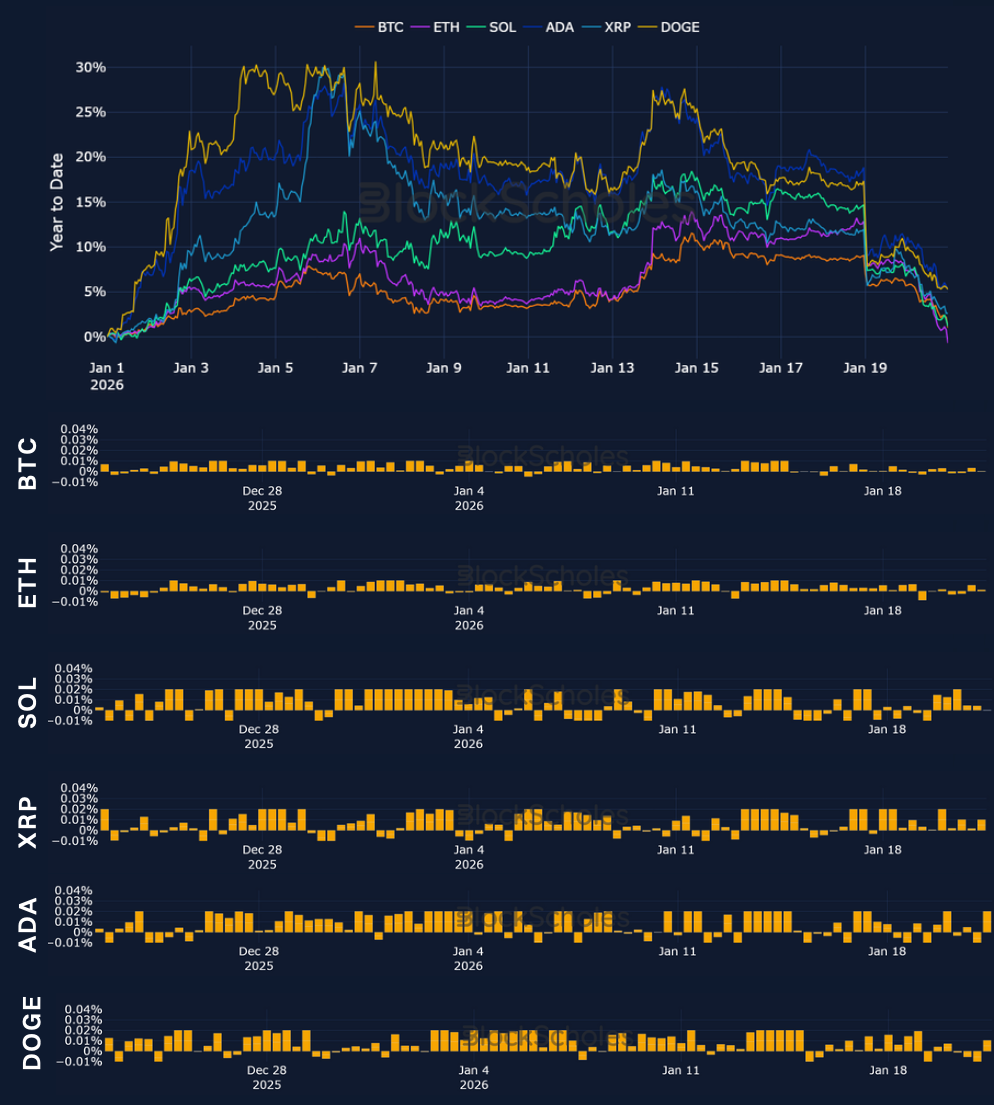

Altcoins further up the risk curve responded more negatively to the sudden deterioration in the macro environment, despite some tokens having their own tailwind idiosyncratic drivers. BTC is down 6% since the weekend when President Trump first announced the Greenland-related tariffs, ADA and DOGE each shed 8%, ETH has fallen 9%, and SOL down 10%.

The House of Doge (the official corporate arm of the Dogecoin Foundation) recently announced plans to launch a new Dogecoin app, named Such, in an effort to expand the token’s utility into everyday payments. Additionally, on Jan 15, 2025, the CME Group, announced plans to launch futures contracts on a number of altcoins, including ADA (Cardano). On a year-to-date basis, SOL, ADA, XRP and DOGE have outperformed BTC, while ETH is flat on the year so far.

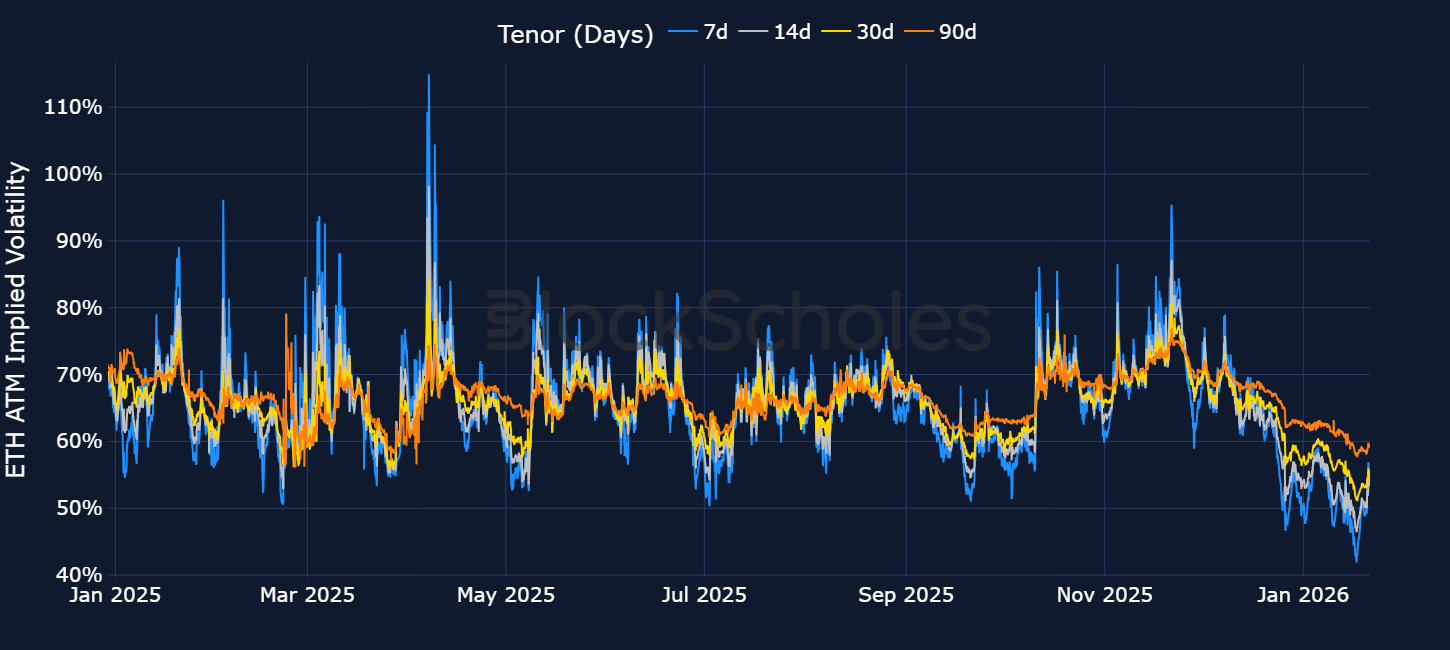

Positioning in options markets so far reveals a lack of major panic beyond the immediate near term. Since the start of the weekend, at-the-money implied volatility at both mid- to long-dated tenors for BTC and ETH have registered only a slight increase. One-month BTC expiries for example have seen ATM IV rise from 37% to 40% for BTC and 51% to 54% for ETH. Expiries further out such as 60-day options have jumped by only 2 vol points.

Macro-inspired volatility has shown a marked impact only at shorter tenors. The 7-day ATM IV, for example, jumped from 31% to 40% for BTC and 42% to 52% for ETH. However, on a longer lookback, recent jumps at the front end of the term structure have done very little to abate the overall trend of lower volatility since the local high in late November 2025.

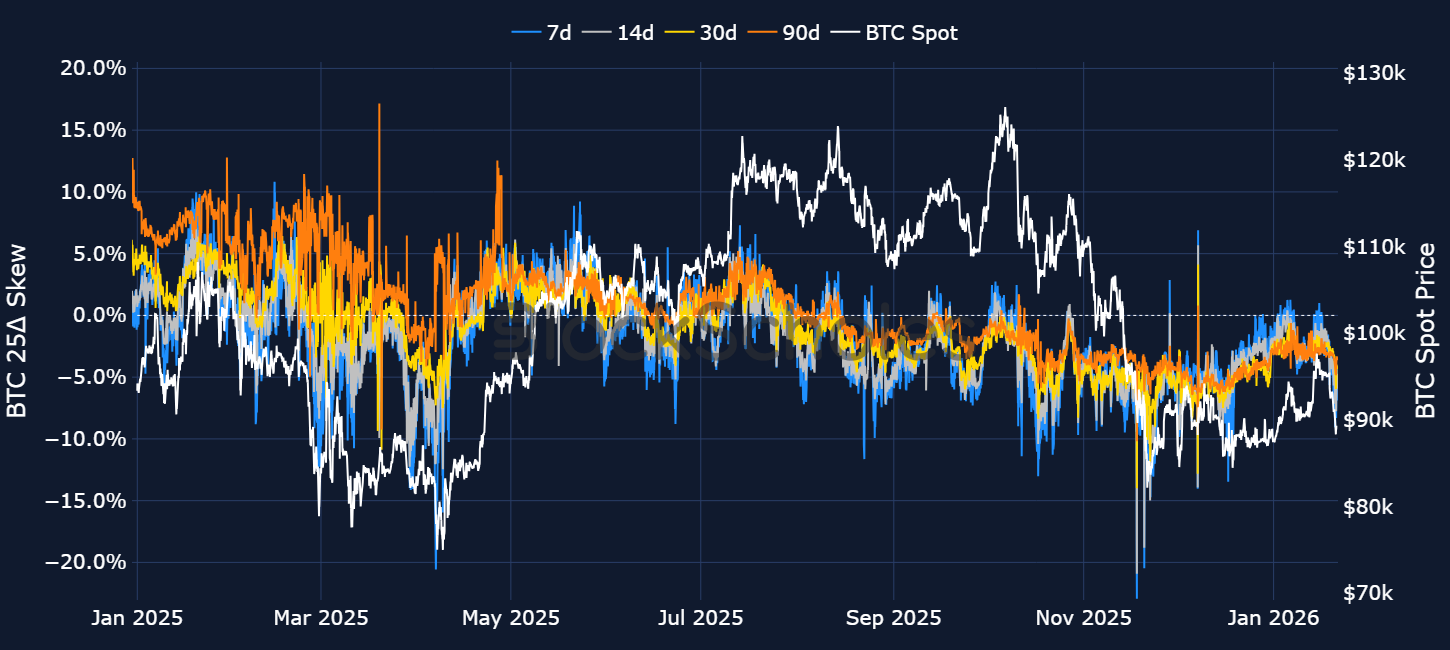

The dislocation between longer-dated and shorter-dated options is also in the skew of BTC and ETH’s volatility smiles.

Short-dated smiles show signs of extreme short-term panic – traders in options markets are not willing to bet against the fact that $87K may not have marked the bottom. As such, 7-day volatility smiles currently show a put-call skew of -7.5%, i.e., 7-day OTM puts trading with a 7.5 volatility point premium over calls at similar moneyness. That ratio reached as low as -9.1%, marking the lowest 7D BTC skew since mid-December 2025 when BTC reached a local bottom of $85K.

For BTC tenors above 30-days, we see less extreme signs of bearish sentiment than in shorter-dated options. The put-call skew ratio is trading below -5%, levels last seen on Dec 30, 2025.

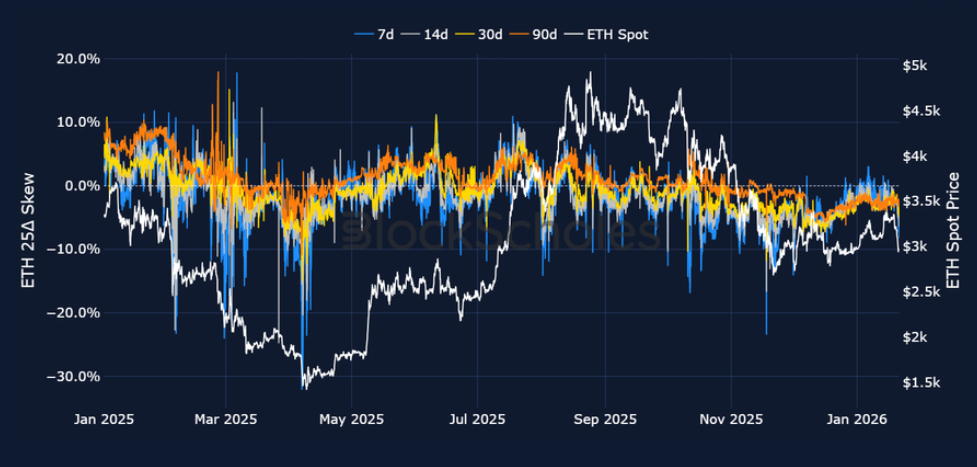

The dislocation is even clearer in ETH. One-week volatility smiles show a put-call skew ratio of -5.6%, the most bearish premium towards ETH put contracts since Dec 20, 2025. However, when we look at the volatility smile of one-month expiries, we see very few signs of any additional panic stemming from recent macro developments. The 30-day put-call skew ratio trades at -4.0%, a level we have seen it bounce off on Jan 7, Jan 8, Jan 11 and Jan 15, 2026 alone.

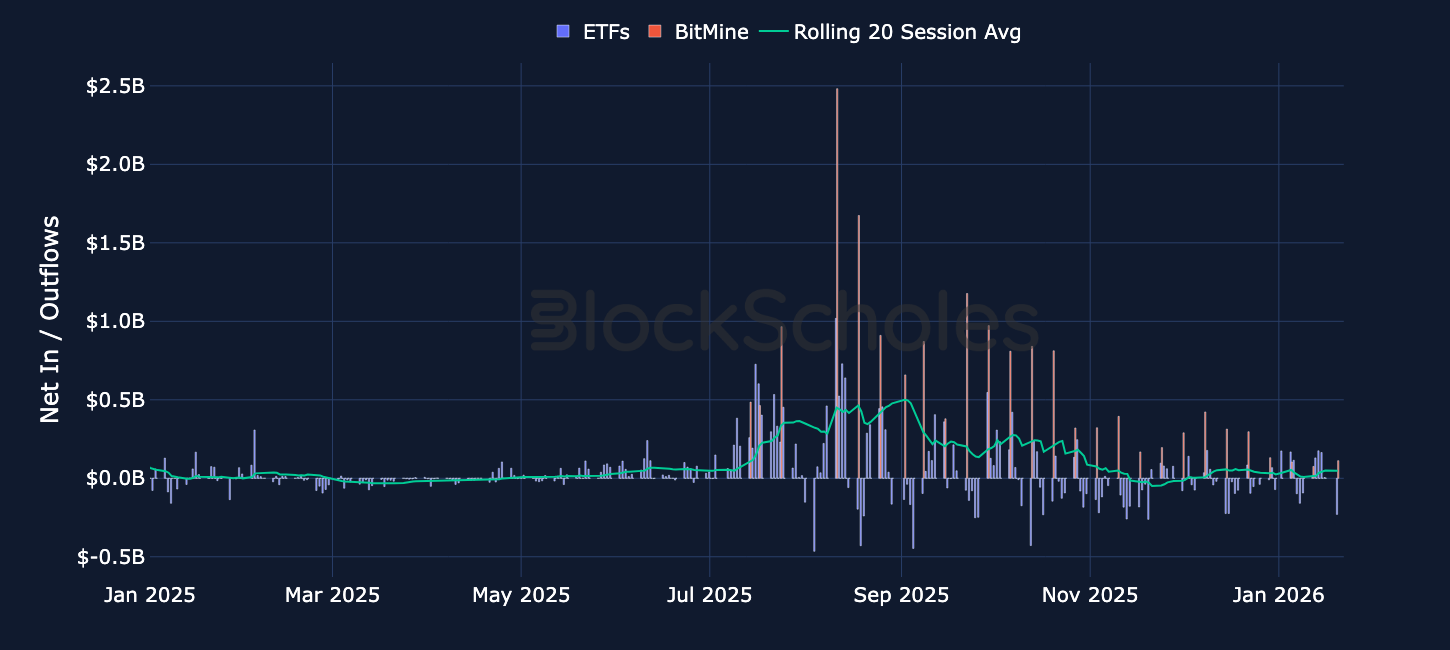

Ethereum staking has seen strong growth in January 2026, driven by large-scale DAT staking that includes major players BitMine and SharpLink Gaming allocating large chunks of treasury holdings. In particular, BitMine reported total ETH holdings of 4,203,036 ETH, with 1,838,003 ETH staked (up 581,920 in the past week) and 35,268 ETH acquired in the past week (as of Jan 19, 2026), targeting an estimated annualized staking yield of 2.81%. BitMine’s total staked ETH is expected to grow as it advances its validator strategy and prepares to launch its MAVAN initiative (Made in America Validator Network), which the company says is on track for Q1 2026. Additionally, SharpLink Gaming disclosed 11,614 ETH of cumulative staking rewards since launching its Ethereum treasury on June 2.

Rising institutional participation and the rollout of staking-enabled ETH ETPs also support the elevated Ethereum staking demand. Grayscale’s Ethereum Staking ETF made its first staking distribution this month, paying roughly $9.4M in total (about $0.083178 per share) to shareholders.

Other spot Ethereum ETF issuers are also moving in this direction: BlackRock, Fidelity, and Bitwise have filed to add staking and are currently awaiting SEC action. The shift in institutional staking was sparked by the SEC Division of Corporation Finance’s May 29, 2025 staff statement (“Statement on Certain Protocol Staking Activities”), which outlined the staff’s view that certain protocol-level staking arrangements do not constitute the offer or sale of securities under federal securities laws.

Staking remains a strong use case for digital asset treasuries and other long-term ETH holders, as it provides passive yield on otherwise idle holdings. However, as DAT holdings grow (e.g., BitMine aims to accumulate towards 5% of total ETH supply) so too does the amount staked on the Beacon chain. Ethereum’s staking reward rate scales inversely with the square root of total active stake, since more rewards are distributed across a larger pool of staked ETH.

With ETH staking yield now comfortably below 3% and continuing to decline, the value proposition of staking as a yield-bearing strategy may weaken, impacting future profitability for DATs, institutions, and especially retail participants who can easily access alternative assets offering higher staking yields.

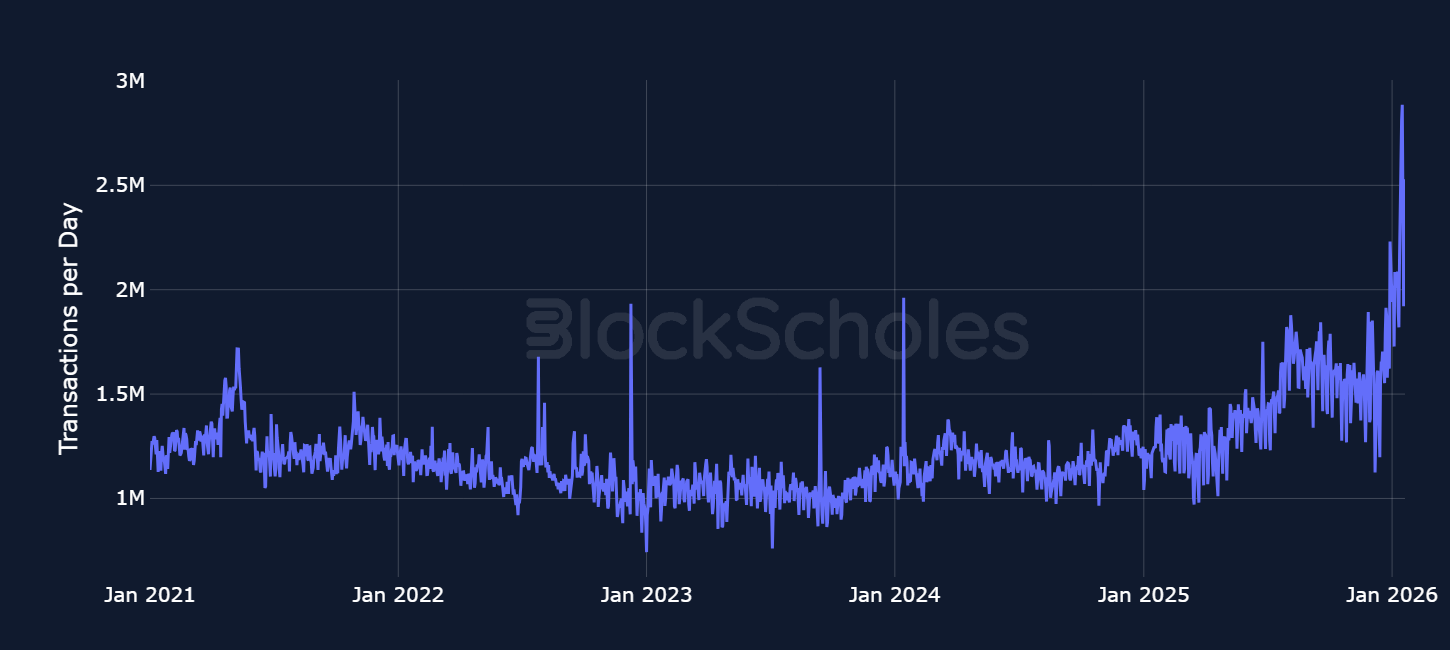

Data shows Ethereum L1 transaction throughput reaching a new high in 2026, while average gas fees are close to multi-year lows.

Higher transaction counts do correlate with higher validator income, but since transaction fees are burned as per the protocol (EIP-1559), a rise in transactions only improves staking returns if it meaningfully affects tips and MEV opportunities for validators. Ethereum’s developments have reduced the need to tip by increasing effective blockspace, with EIP-1559’s elastic blocks allowing capacity to expand above the target during demand spikes and validators voting to raise the block gas limit from around 45M to around 60M in Nov 2025. Additionally, these validator incentives will be split across a growing proportion of staked ETH. Therefore staking profitability is still dominated by Ethereum’s consensus-layer issuance and the size of the staked set. Higher transaction volumes are bullish for Ethereum’s utility, reflecting greater usage and reliance on the Ethereum mainnet, but it is not a catalyst for higher staking returns which will ultimately diminish as DATs account for a larger share of the beacon chain balance.

Seeker (SKR) is the native token of Solana Mobile’s Seeker ecosystem, which is being positioned as a decentralised mobile platform designed to reduce the power of traditional mobile gatekeepers and enable broader access to crypto applications.

Seeker’s goal is a community-owned mobile stack where developers can reach users more directly, governance is decentralised, and platform rules are set by the community rather than a single corporate intermediary. A core part of the technical narrative is built around TEEPIN (Trusted Execution Environment Platform Infrastructure Network), a three-layer architecture that uses trusted execution environments and cryptographic attestation to verify devices and software and enable a more open, trust-minimised mobile ecosystem.

SKR is intended to align incentives across users, developers, and ecosystem partners and to support governance. Solana Mobile describes a governance model that includes “Guardians”, who are expected to help verify device authenticity, coordinate app review/certification processes, and enforce community standards. Users can delegate SKR to Guardians, with staking rewards and governance participation tied to that delegation.

Its recent catalyst has been the token’s mainnet launch and initial distribution. Solana Mobile announced the launch of SKR on Solana mainnet alongside an airdrop distribution directed at Seeker Season 1 users and developers, with reporting indicating roughly 2B SKR allocated to the airdrop and a defined claim window.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)