Andrew Melville

Research Analyst

A slowdown in spot prices this week has seen short-tenor BTC and ETH options assign a slight volatility premium to out-of-the-money (OTM) put options, a signal of bearish sentiment. This contrasts with the bullish outlook portrayed in perpetual futures markets, in which funding rates for BTC, ETH and a slew of other tokens have been persistently positive. BTC has traded range-bound between $115K and $120K, reaching that lower bound on Jul 25, 2025 — coinciding with a sale of 80,000 Bitcoins facilitated by Galaxy Digital from a “Satoshi-era investor.” BTC’s spot price quickly recovered from that low, but has since failed to break past $120K.

A slowdown in spot prices this week has seen short-tenor BTC and ETH options assign a slight volatility premium to out-of-the-money (OTM) put options, a signal of bearish sentiment. This contrasts with the bullish outlook portrayed in perpetual futures markets, in which funding rates for BTC, ETH and a slew of other tokens have been persistently positive. BTC has traded range-bound between $115K and $120K, reaching that lower bound on Jul 25, 2025 — coinciding with a sale of 80,000 Bitcoins facilitated by Galaxy Digital from a “Satoshi-era investor.” BTC’s spot price quickly recovered from that low, but has since failed to break past $120K.

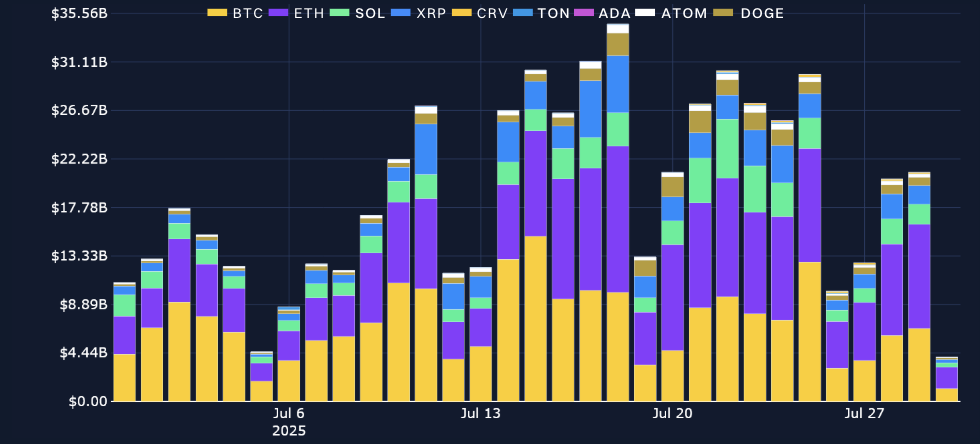

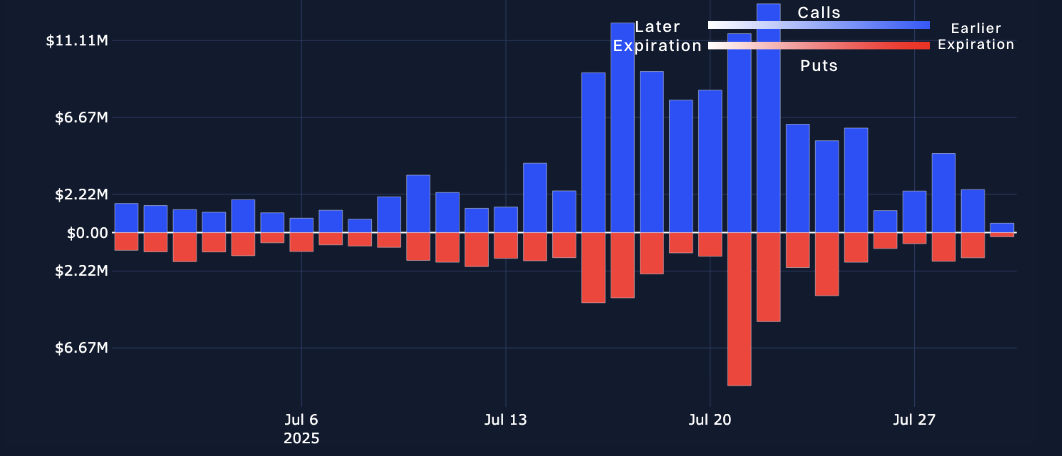

Perpetuals: On Jul 25, 2025, open interest for perpetual contracts increased almost linearly for BTC and altcoins, exceeding $15.5B.

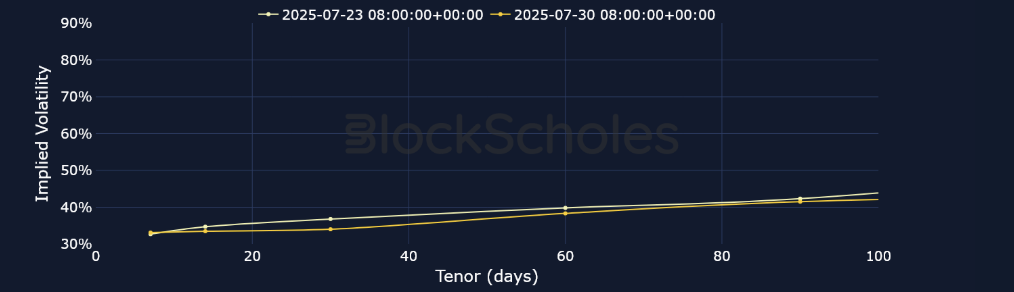

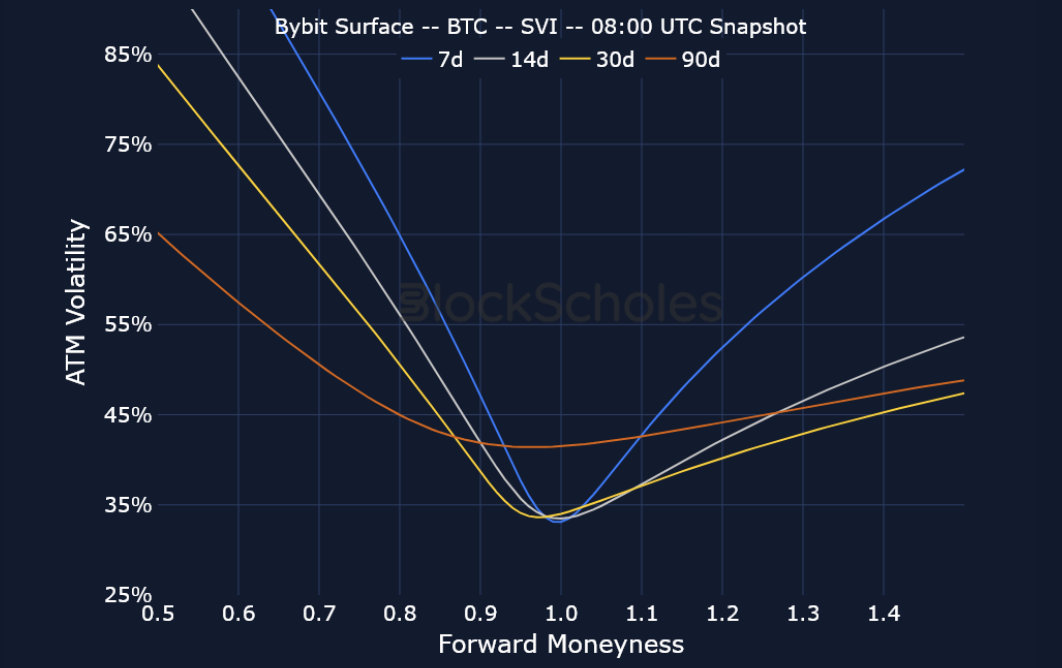

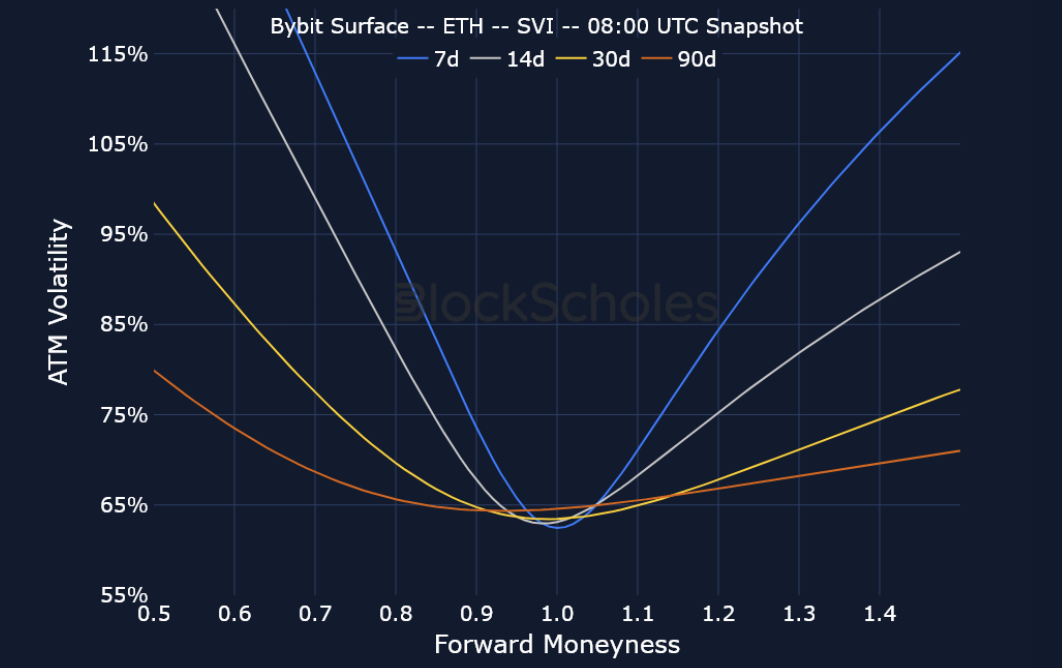

Options: ETH’s compressed and flat term structure of volatility contrasts with the upward slope in BTC’s term structure, while short-tenor volatility smiles for both assets are exhibiting a bearish-to-neutral sentiment. SOL’s spot price is down 9% over the past seven days, however options volumes are still dominated in calls and volatility smiles continue to assign a volatility premium to out-of-the-money (OTM) call options.

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

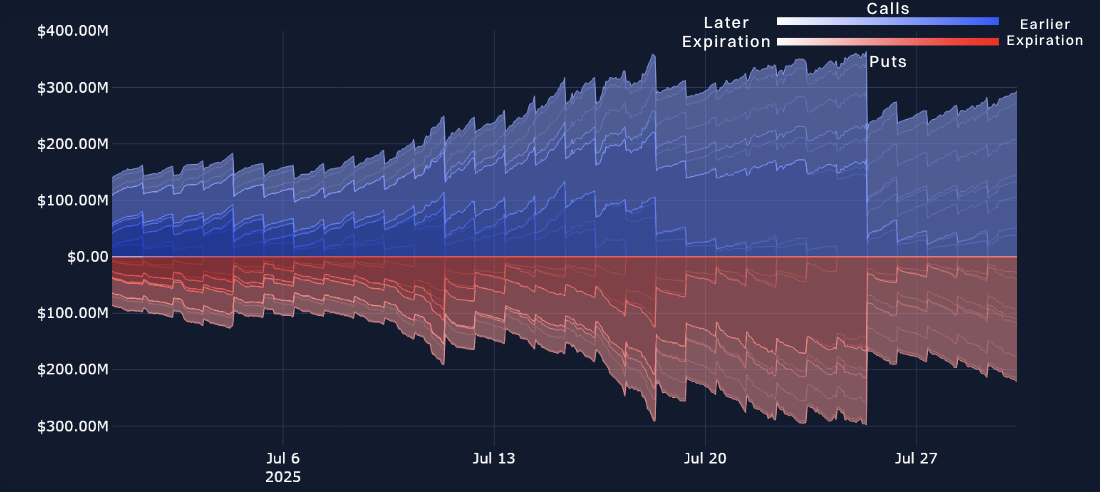

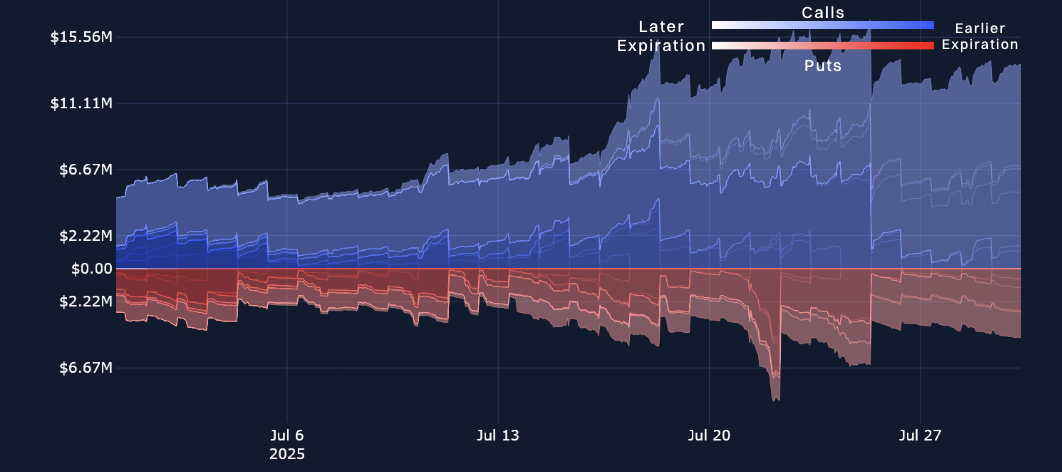

Only two weeks ago, BTC rose to a new all-time high as market sentiment rocketed amidst what the US president and a congressional committee dubbed “Crypto Week” from Jul 14–18, 2025. Later that week, altcoins such as Ether and XRP started to surge, and indeed the widely followed BTC dominance metric saw a five percentage point decline. Alongside that rally in spot prices, open interest rose to $15B, then surged once more in a near-linear fashion to above $15.5B on Jul 25, 2025. Interestingly, that increase occurred while BTC’s spot price fell to $115K, a sell-off that coincided with Galaxy Digital helping facilitate the sale of 80,000 bitcoins.

Since that high, open interest in perpetual contracts for BTC has fallen, while open interest in altcoins has fallen at a lag. For BTC perpetuals, open interest has been declining since Jul 25, 2025, and yet for altcoins — such as ETH, SOL and XRP — open interest had initially held firm until Jul 28, 2025 when it started to decline. For example, total open interest for ETH contracts peaked at $4.4B and held flat before dropping to $4B. In comparison, open interest for BTC perps dropped from $8B to $6.9B almost continuously between Jul 25, 2025 and today.

The past week has seen a mixed performance from altcoins, particularly after the week that preceded it, when a temporary drop in BTC dominance to the low-60% region boosted talks of an impending altcoin season. Instead, it seems that the catch-up rally for altcoins may have seen some traders take profits, resulting in spot prices pulling back. For example, XRP is down 11% from Jul 23, 2025, while SOL is down 10% from the same date. Among the top 10 altcoins by market cap, ETH and TRON are trading higher — with the former up just over 3% and the latter rallying 5%.

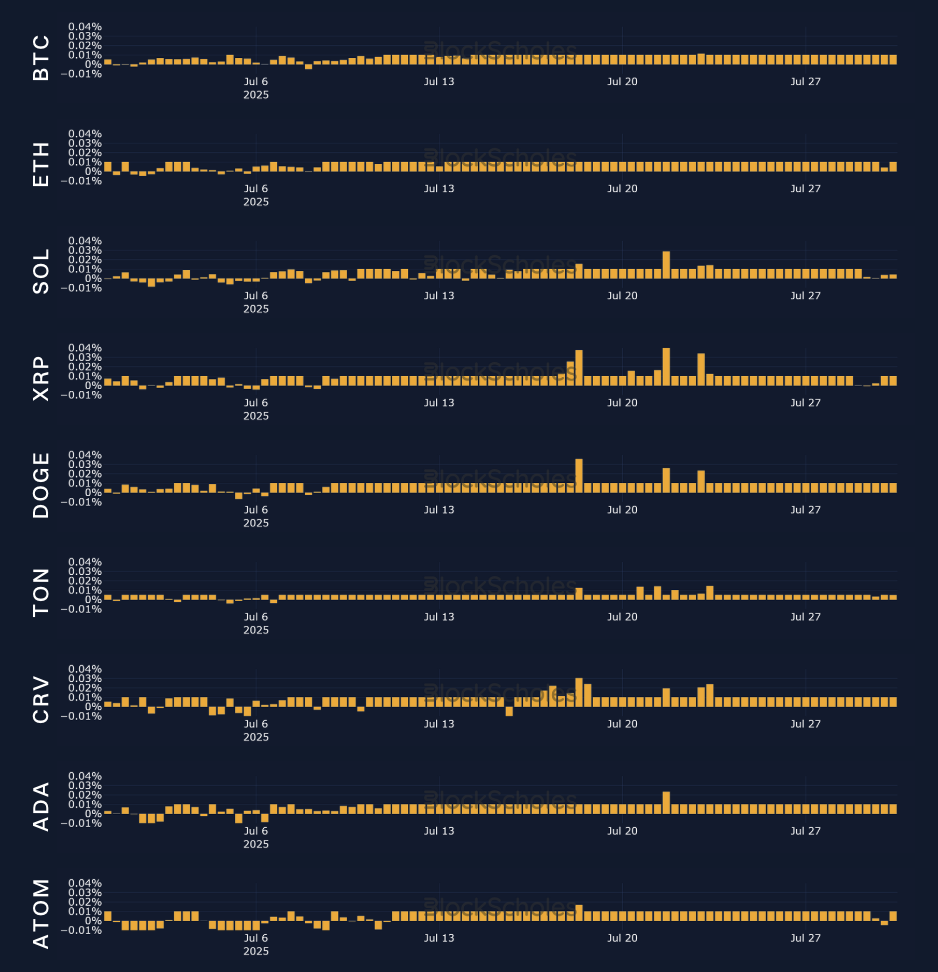

Despite a temporary pullback in spot prices, funding rates haven’t shown signs of slowing down. Just as we saw last week across the observed tokens, funding rates are exuberantly positive. BTC and ETH haven’t registered a single negative eight-hour funding rate since Jul 7, 2025. DOGE and XRP, two tokens benefiting from the recent market optimism, even had rates exceeding 0.03% on an eight-hourly basis. XRP has recently rallied alongside a basket of other payment-related tokens amid the signing into law of the GENIUS Act in the US, while DOGE, the original meme coin token, is up 34% over the past 30 days.

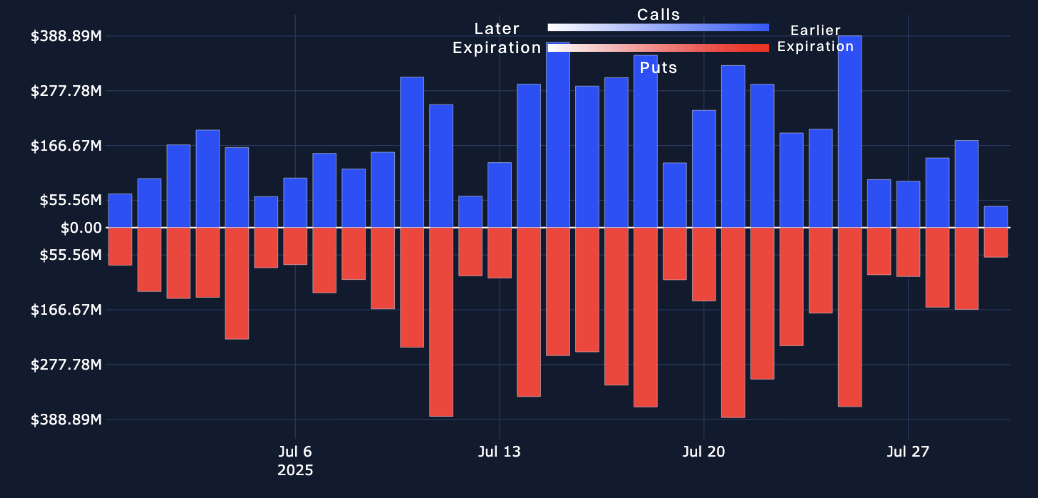

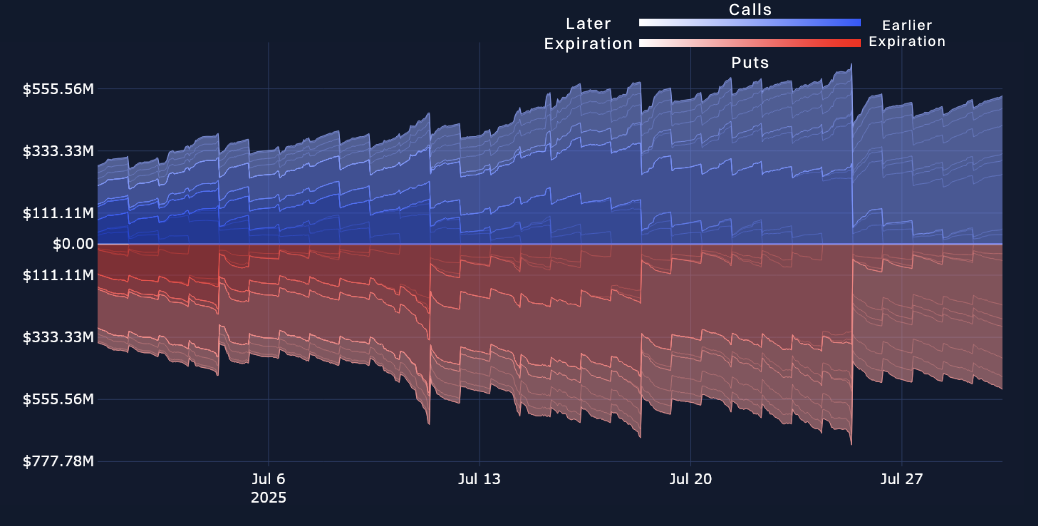

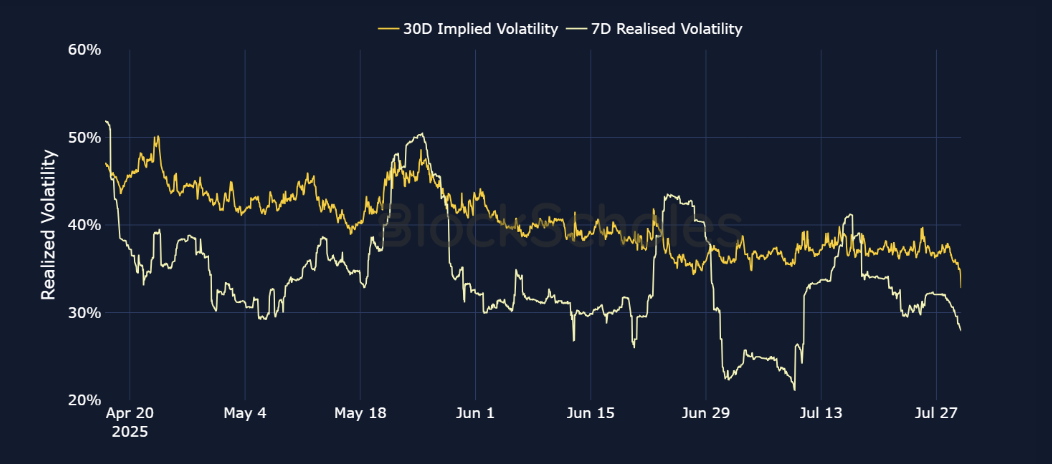

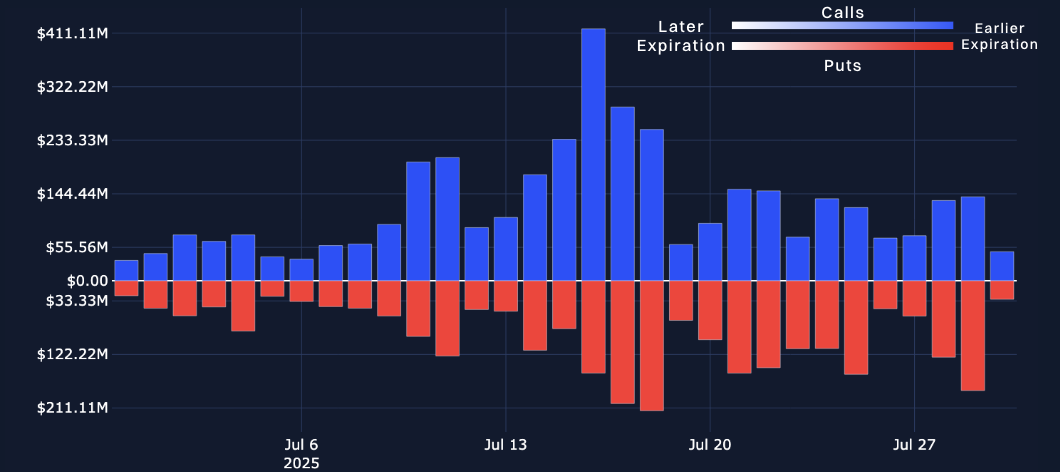

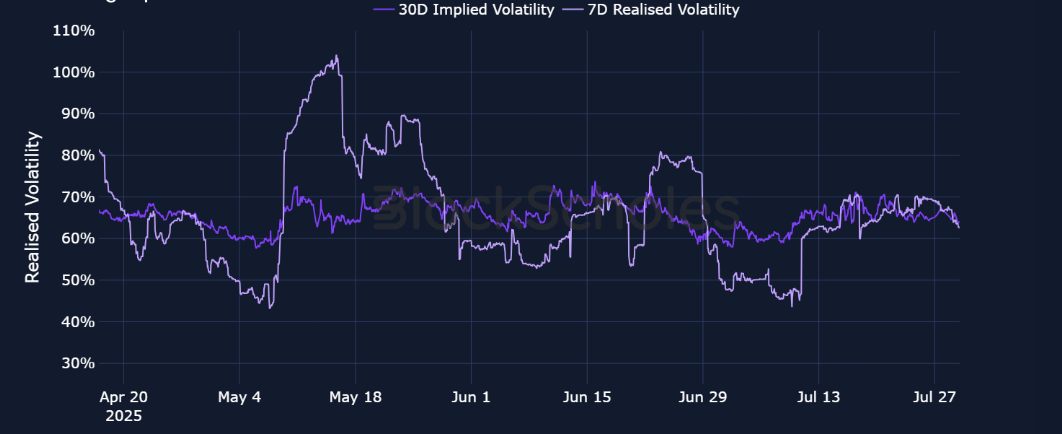

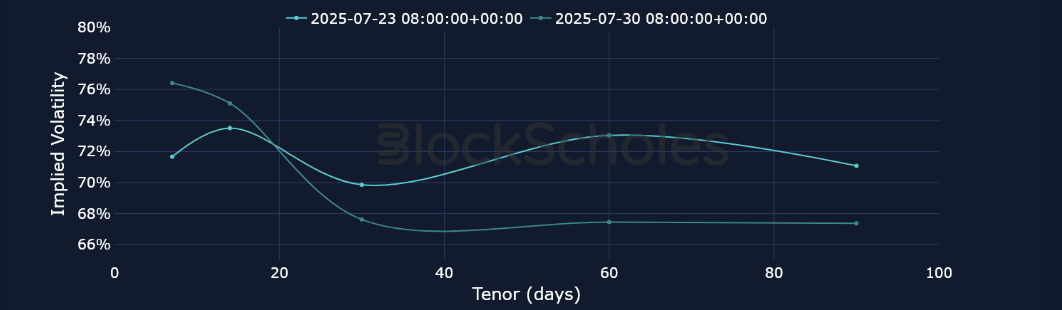

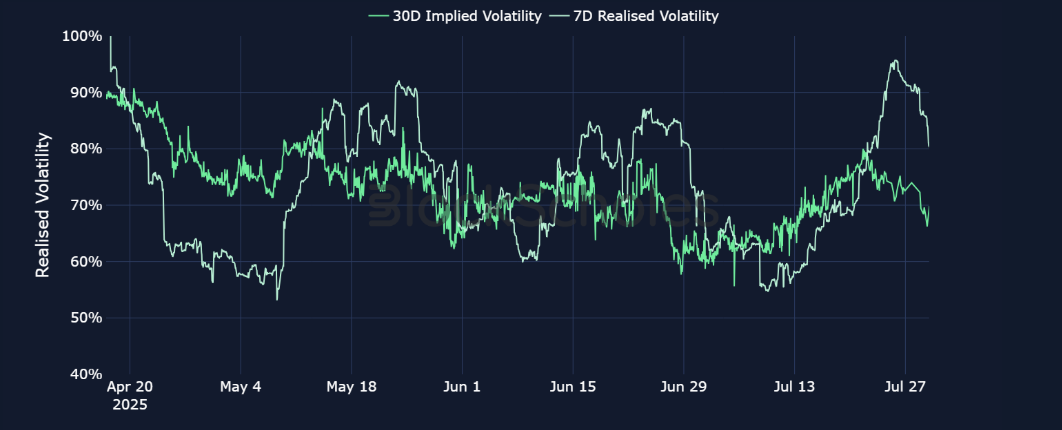

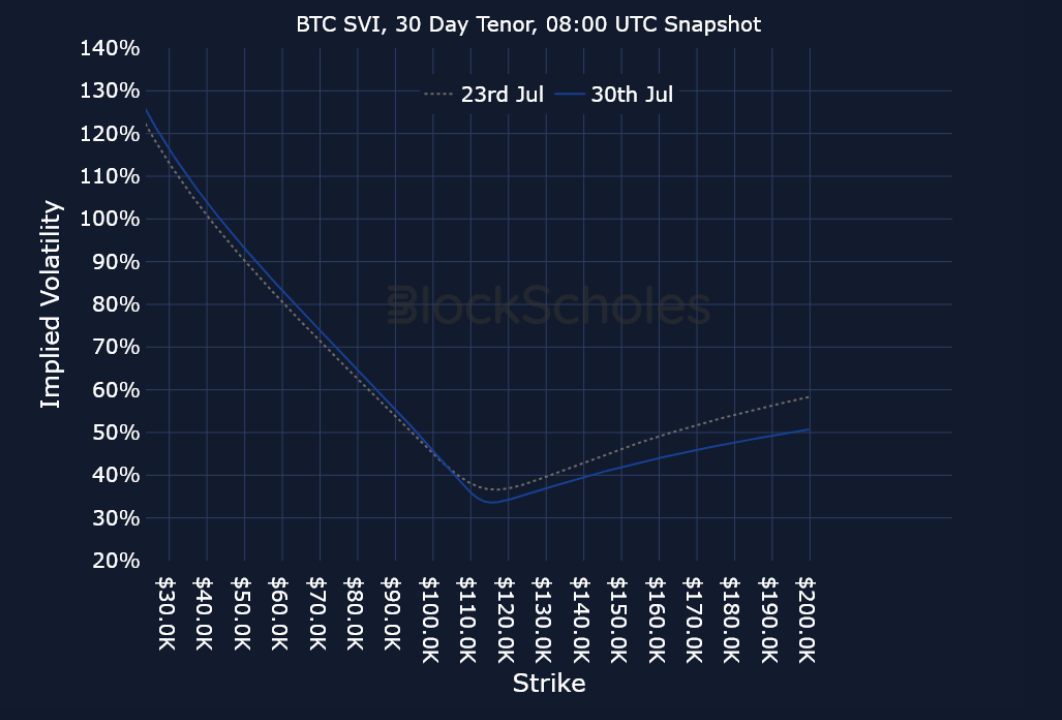

After reaching a new all-time high of $123K, BTC has been trading between $115K and $120K. While that range-bound price action may seem like a slow sideways slog, by zooming out we can see that BTC is up nearly 30% since the start of the year, an outperformance relative to both gold and US risk-on assets. Meanwhile, the lower bound of the current sideways spot activity coincides with a major 80,000 Bitcoin sale on Jul 25, 2025, facilitated by Galaxy Digital on behalf of a “Satoshi-era investor.” Traders quickly “bought the dip,” and BTC’s spot price bounced off the local low sharply, though it hasn’t jumped enough to break past $120K. Volumes in BTC options exploded on Jul 25, 2025, reaching as high as $390M. Since then, volumes have looked minuscule in comparison. The next largest day for BTC options volume was Jul 29, 2025, though the $170M recorded was more than half that on July 25. Similar to spot price, the implied volatility on 7-day BTC options has traded between 31% and 37%.

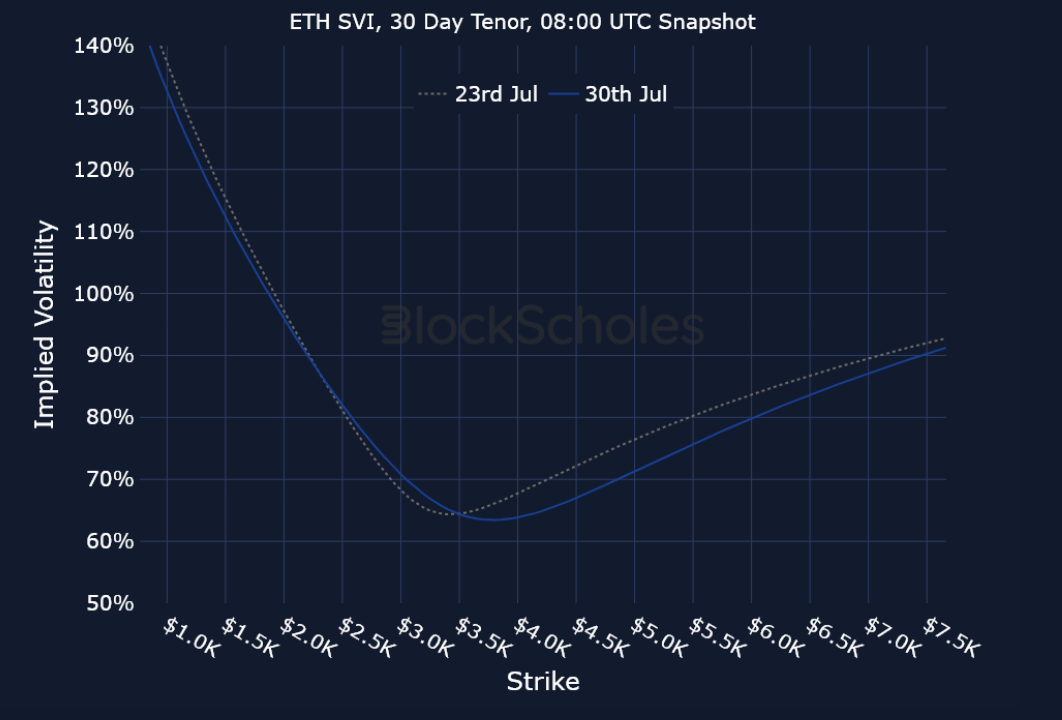

After reaching its highest levels since December 2024, ETH’s spot price has pulled back slightly, and is currently trading at under $3,800. The second-largest cryptocurrency by market cap is up 3.5% over the past week, however, outperforming BTC, which is flat since one week ago. Trading volumes for ETH options have remained consistent at above $120M over the past week, while open interest is nearly $100M larger in call options than in puts. ETH’s term structure of volatility is currently flat, with implied volatility across short- and long-tenor options having compressed at 64%.

Derivatives markets on the whole are demonstrating a bullish outlook on ETH over a longer horizon, funding rates have been consistently positive since early July and volatility smiles for options that expire in more than 30 days are firmly skewed toward OTM call options. Alongside that, Spot ETH ETFs continue to demonstrate an insatiable appetite for Ether exposure, having purchased $218.6M of the token yesterday, Jul 29, 2025.

Traders likely capitalized on SOL’s rally above $200 last week, as it’s now trading below $180. The Solana blockchain’s native token is currently down 9% over the past seven days; however, it’s rallied nearly 20% in the past 30 days. It is, however, still underperforming a basket of alternative “Ethereum killers” — and ETH itself. For example, TRON is up more than 22%, SUI more than 33% and ADA up 36%, all within the past month. ETH, in contrast, has surged 50%, thereby illustrating the relative underperformance for SOL holders.

Nonetheless, SOL volatility smiles still firmly assign a volatility premium to out-of-the-money (OTM) call options, and both options volumes and open interest — as is often the case for SOL — remain firmly dominated by calls.

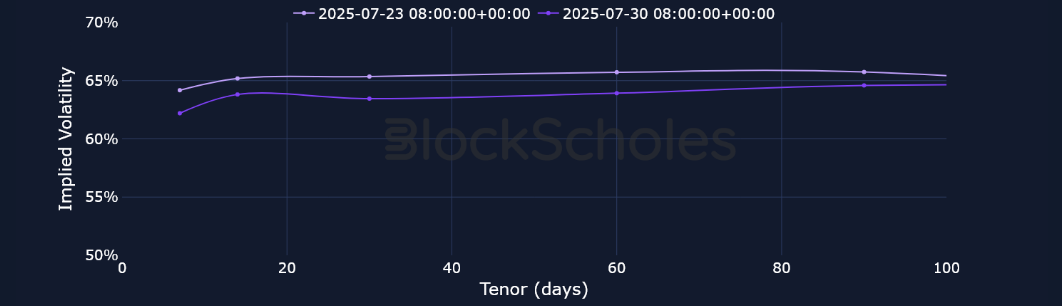

Amidst a market-wide slowdown in spot prices, short-tenor BTC and ETH options are now showing a slightly bearish-to-neutral outlook, contrasting with the sentiment exhibited in perpetual futures markets. Meanwhile, 7-day ETH options currently have a put-call skew of −3.6%, though expirations beyond 30 days are still projecting bullish, positive sentiment for Ether (ETH). At the same time, BTC’s volatility smiles for 7-day tenor options are neutral at 0%, while 14-day options assign a 0.5 percentage point premium to OTM put options.

As mentioned, this is in direct contrast to the animal spirits on display in perpetual swap funding contracts, which for both BTC and ETH have been consistently positive, indicating that long traders have been willing to pay a premium to get upside exposure to spot price since early July.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)