Thahbib Rahman

Research Analyst

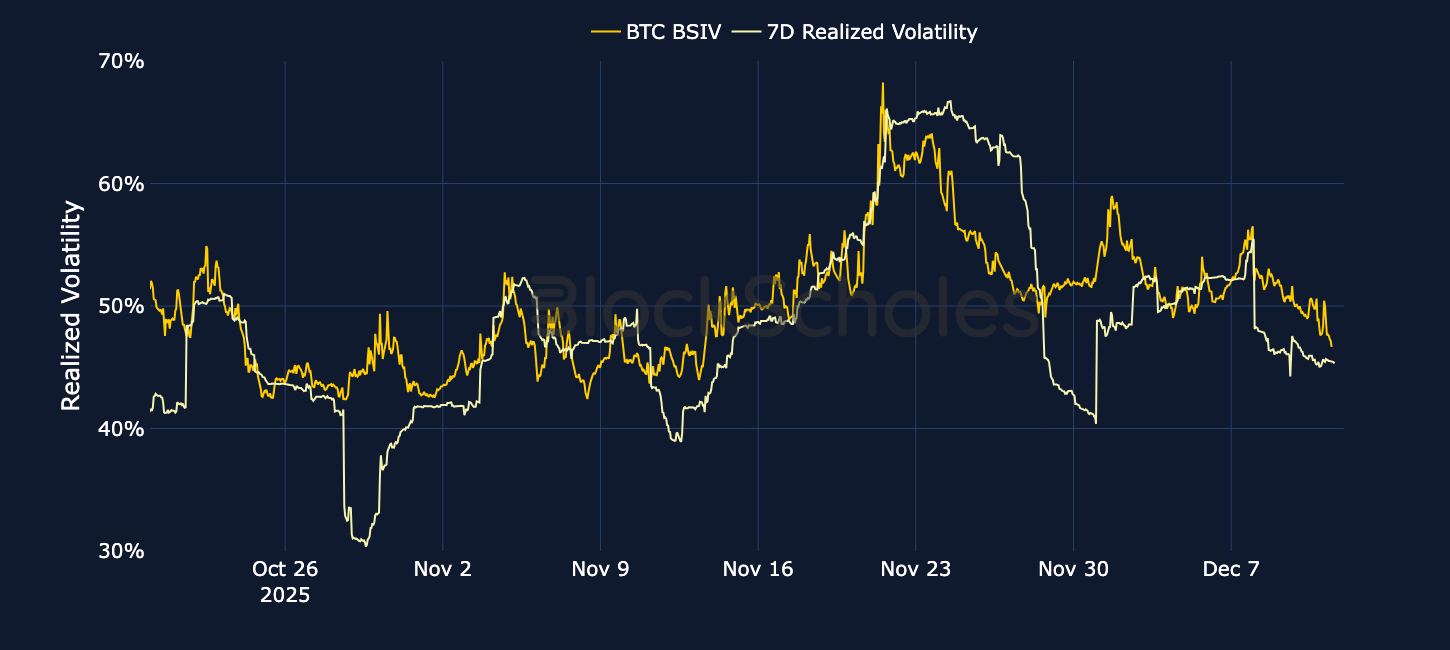

The week’s main event, the FOMC’s final meeting of the year, saw policymakers deliver a 25bps rate cut – an outcome largely expected by markets. Chair Powell delivered a moderately hawkish press conference, leaving the door both open to a rate cut or a pause in the January 2026 meeting. The outcome for crypto markets? Certainly no “firework” reactions. Open interest in perpetual swap contracts has mostly been sideways for the entire week, implied volatility in options markets had steadily fallen lower even ahead of the meeting and perpetual swap funding rates for BTC showed a lack of participation for leveraged position taking. Even after the Fed delivered its third cut of the year and provided a more optimistic outlook on the US economy via the Summary of Economic Projections, volatility smiles in options markets continue to point bearishly – skewed towards OTM puts.

The week’s main event, the FOMC’s final meeting of the year, saw policymakers deliver a 25bps rate cut – an outcome largely expected by markets. Chair Powell delivered a moderately hawkish press conference, leaving the door both open to a rate cut or a pause in the January 2026 meeting. The outcome for crypto markets? Certainly no “firework” reactions. Open interest in perpetual swap contracts has mostly been sideways for the entire week, implied volatility in options markets had steadily fallen lower even ahead of the meeting and perpetual swap funding rates for BTC showed a lack of participation for leveraged position taking. Even after the Fed delivered its third cut of the year and provided a more optimistic outlook on the US economy via the Summary of Economic Projections, volatility smiles in options markets continue to point bearishly – skewed towards OTM puts.

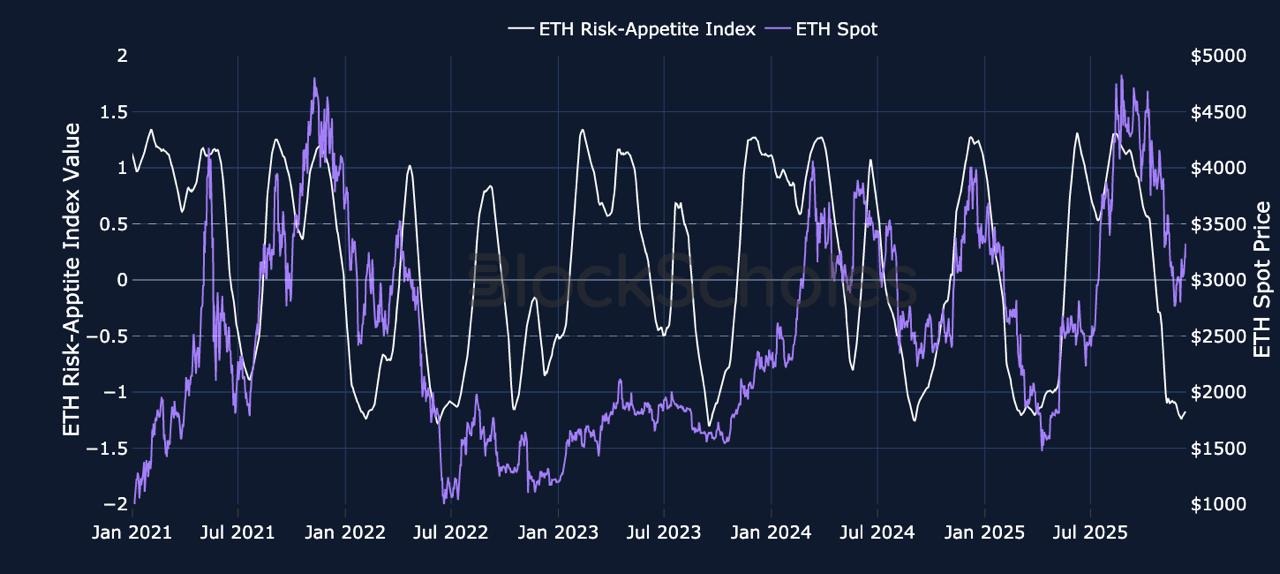

Block Scholes’ Risk Appetite Index measures the level of euphoria (above 1) or panic (below -1) in the spot market. Momentum in this index shows a strong relationship to spot returns.

Quantum Resistant Ledger (QRL) is a Layer-1 blockchain designed to provide long-term protection against the potential impact of large-scale quantum computers on public-key cryptography. Most existing blockchains rely on numerical based cryptography, such as elliptic-curve signatures (a type of public-key cryptography based on mathematical problems involving elliptic curves) or RSA signatures (a cryptographic system built on the difficulty of factoring large integers). However both of these are theoretically vulnerable to Shor’s algorithm, a quantum algorithm capable of breaking number-theoretic systems.

QRL uses post-quantum cryptography (PQC) by adopting XMSS (eXtended Merkle Signature Scheme), a hash-based signature system approved by NIST, the U.S. agency that sets cryptographic standards. Because XMSS relies on hash functions rather than mathematical problems, QRL’s signatures provide stronger protection against quantum attacks, as these hash functions are harder for quantum algorithms to solve.

QRL originated in 2016 and launched its mainnet in June 2018, becoming one of the first blockchains to use quantum-secure signatures from inception. It operates using Proof-of-Work with the RandomX algorithm, a CPU-friendly, ASIC-resistant method for validating blocks, which aims to keep mining more decentralized by reducing reliance on specialised hardware and letting more users participate.

The native token QRL is capped at 105 million tokens and enters circulation through block rewards, which miners receive under a predefined emission schedule. Each mined block issues a set amount of QRL, and these rewards gradually decrease over time following a long-term decay curve. All newly created QRL is released only through this mining process.

The chain has run continuously since launch, and development is now focused on Project Zond, a planned upgrade introducing a quantum-secure Proof-of-Stake model and lattice-based smart contracts, expanding QRL from a transfer-only network into a full execution environment.

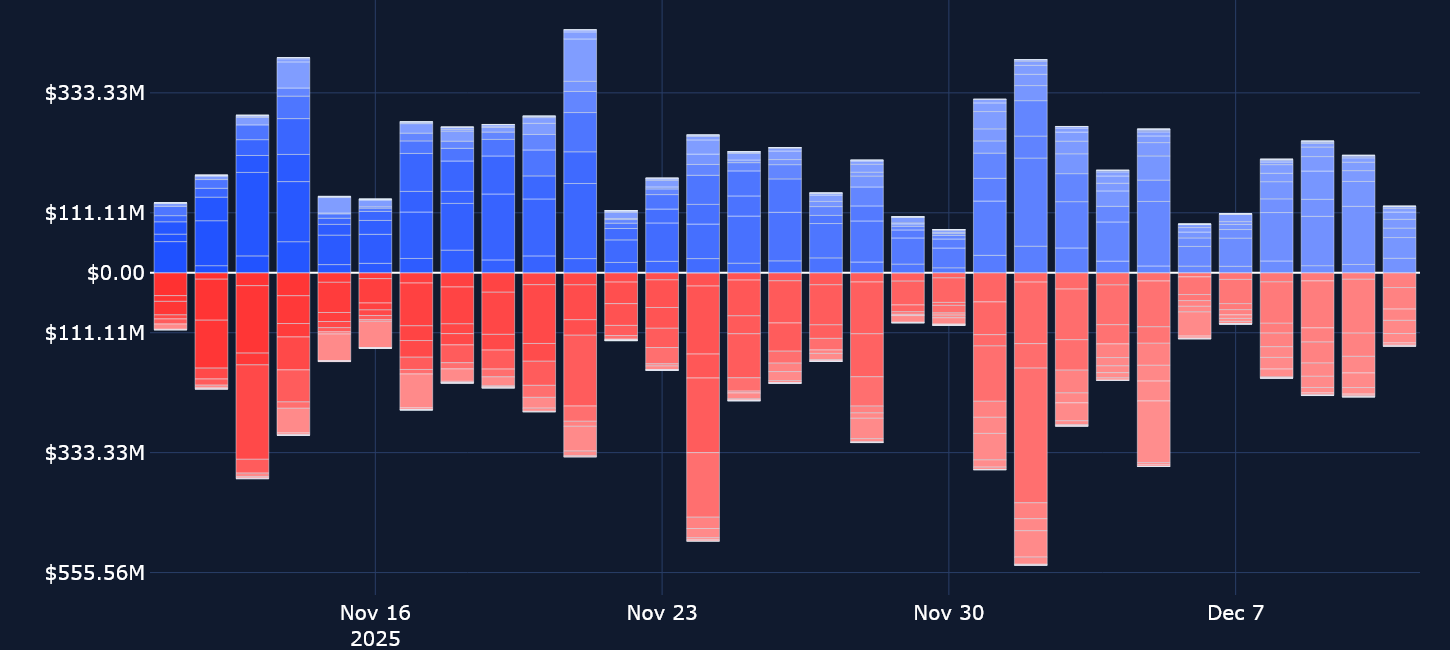

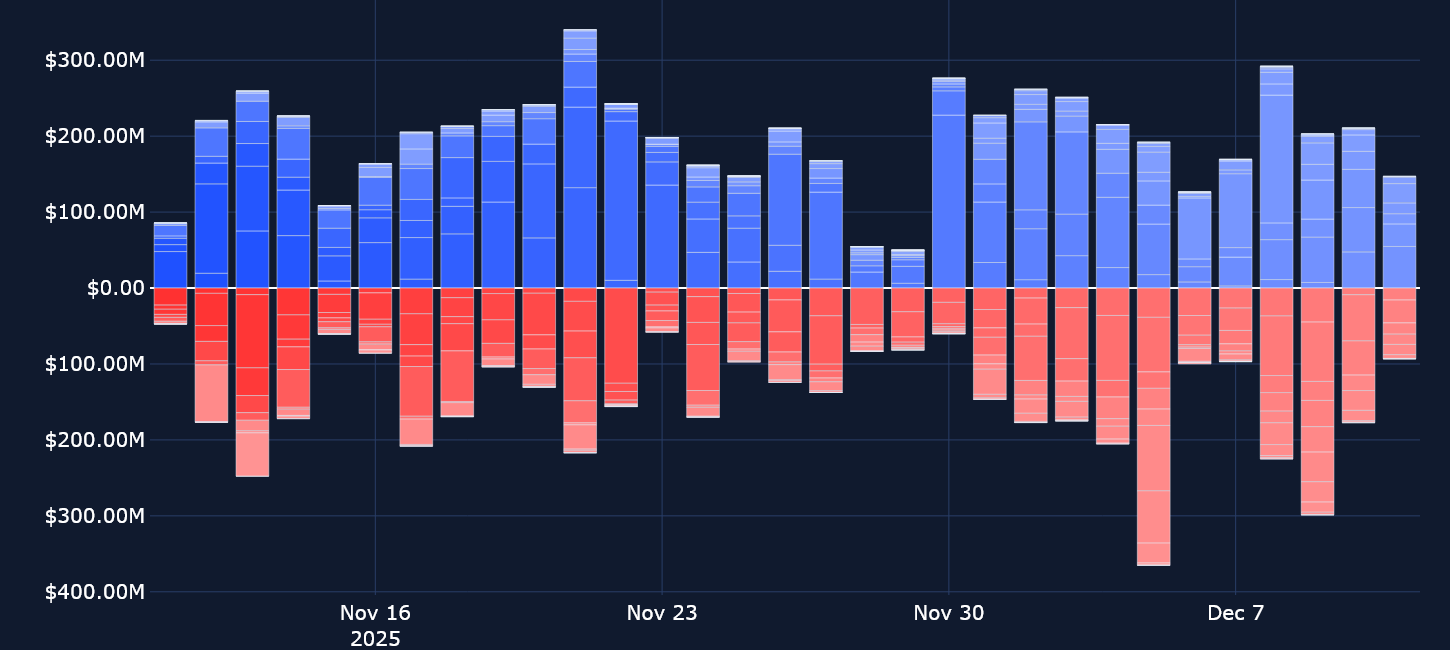

The FOMC’s final meeting of the year saw policymakers cut interest rates for the third time in 2025, in line with market expectations. On the whole, Chair Powell delivered a moderately hawkish press conference, keeping both the option of a pause and a cut open for the January meeting. We see very little firework reactions in leveraged swap contracts open interest and trade volumes both in the days leading up to the meeting, and in its aftermath. Open interest had mainly stayed flat around $8B for most of this week, with a small drop in early Asian trading hours on Dec 11, 2025 as BTC spot price slowly sunk from $94.5K to $90K post Chair Powell’s press conference.

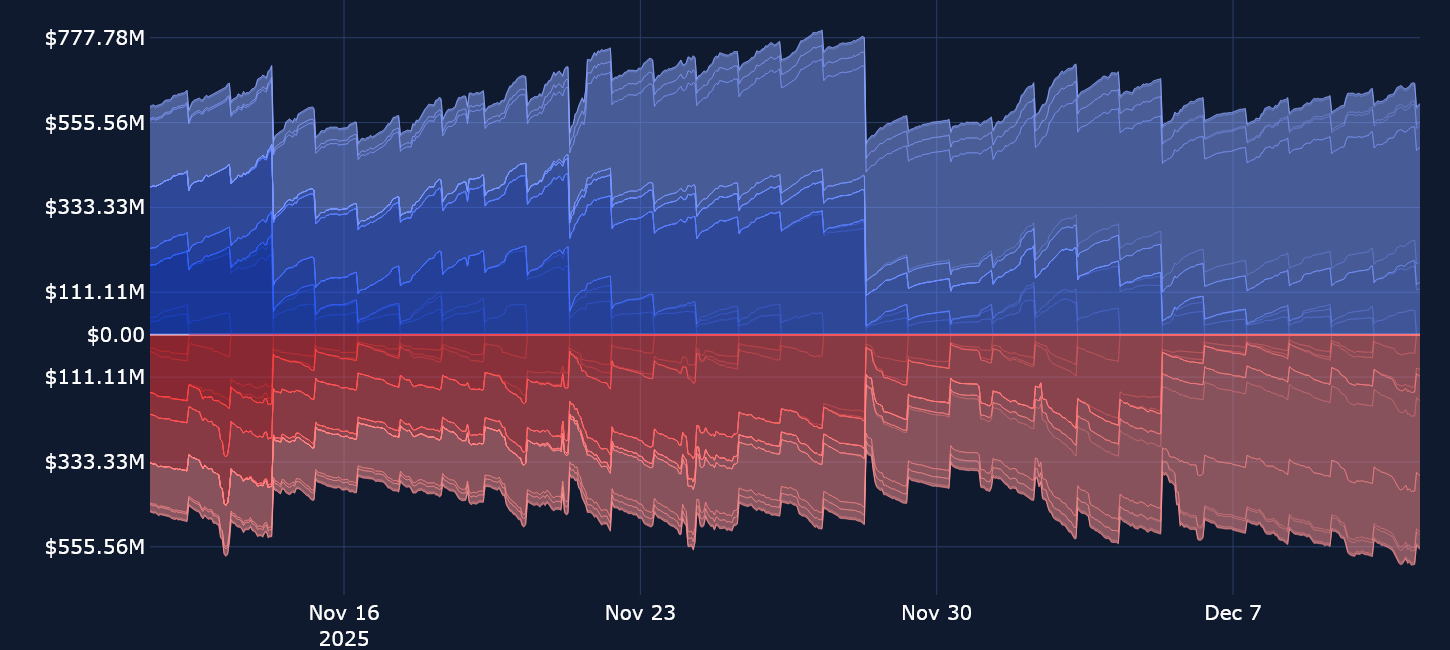

Overall, as we have continued to observe on a weekly basis with BTC’s spot price still 28% below its ATH, traders are not showing much appetite to re-enter leveraged positions, and we see few signs of any major liquidations this week. Both open interest levels and trade volumes are far lower than their peaks pre-Oct 10, 2025.

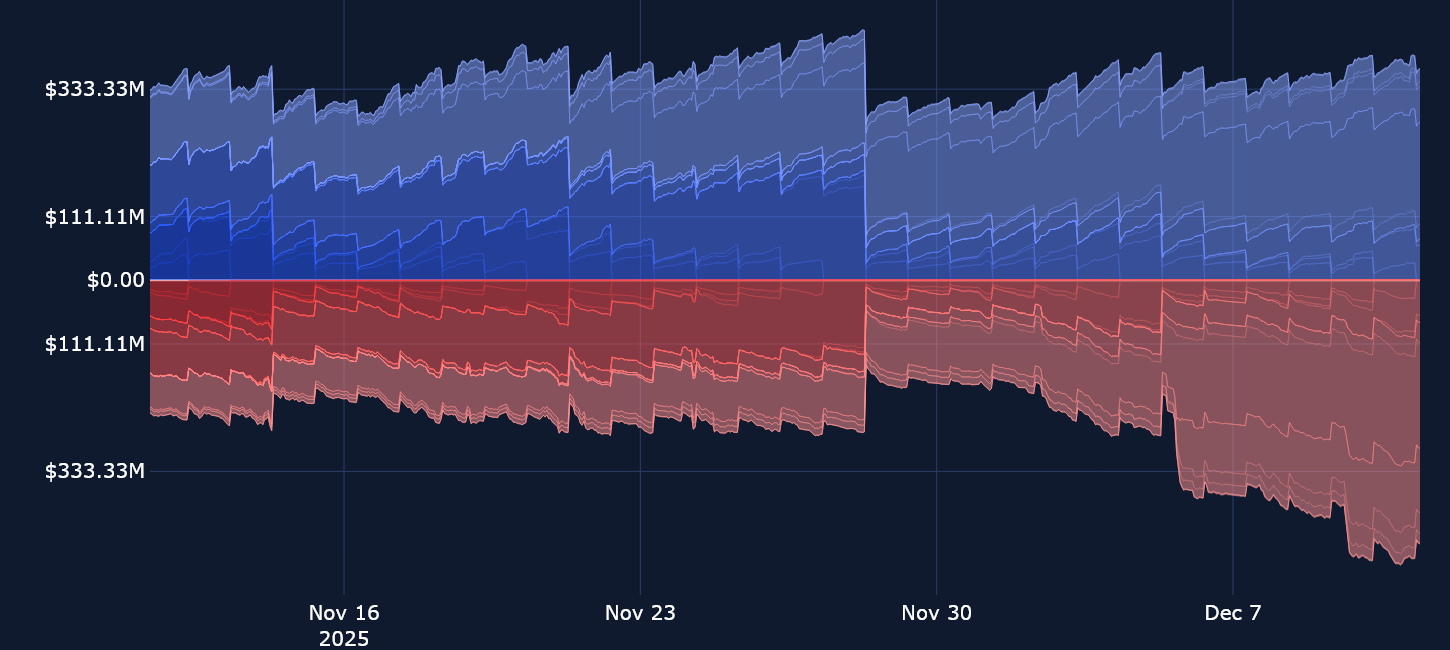

This week’s sideways movement in open interest levels has been accompanied by very modest funding rates in BTC, further reflecting a lack of participation in leveraged position taking. BTC funding rates have been very flat since the start of the month as spot price struggles to break out past $95K.

Looking at blue-chip altcoins, we mostly see bearish positioning: ETH funding rates have fluctuated between positive and negative values since the start of the month, while SOL has recently registered a number of negative rates, as has XRP. Negative funding rates are indicative of traders willing to pay a premium in order to maintain their leveraged short positions.

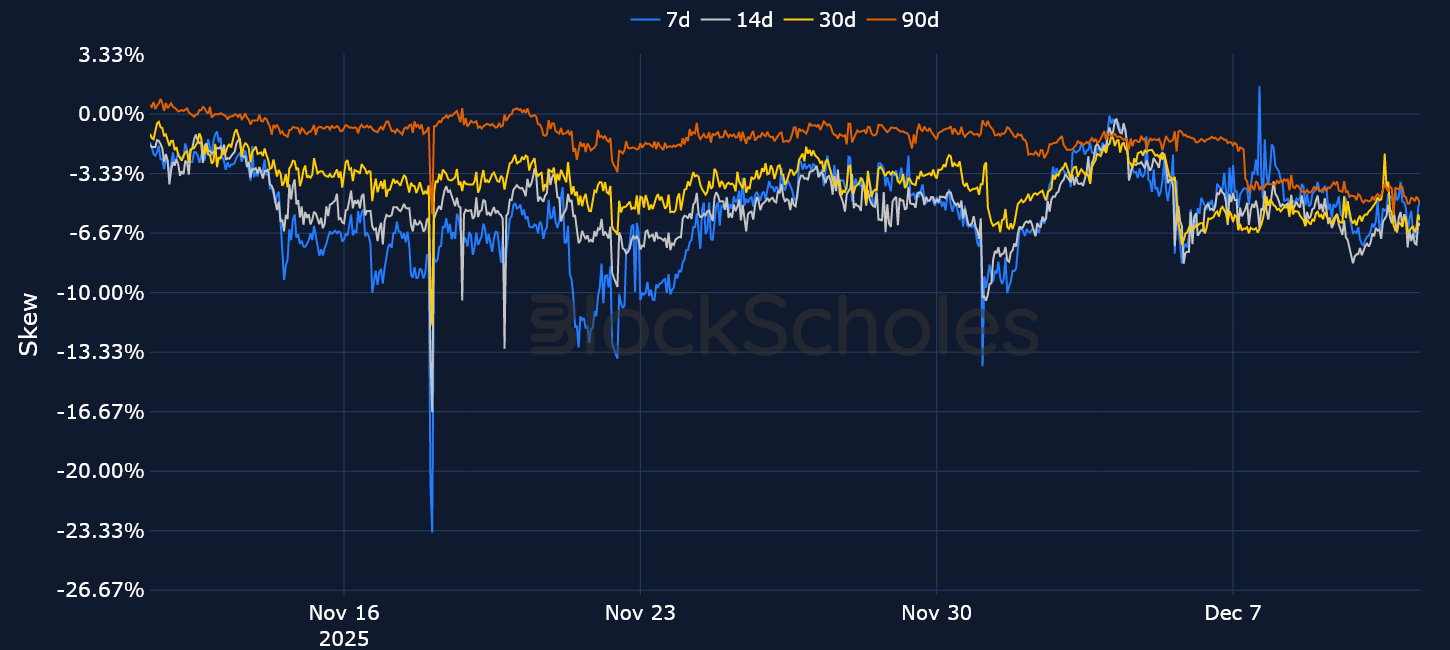

Looking at these tokens year-to-date performances, the negative rates are somewhat unsurprising: ETH trades 4% below the level it entered the year with, while SOL is down 30% YTD, and XRP is down 3%. Those negative funding rates also mirror bearish positioning in options markets, where volatility smiles for BTC and ETH are skewed towards protection against further collapses in spot price. For now, positioning in derivatives markets suggests a higher bar for a ‘Santa rally’ before year-end.

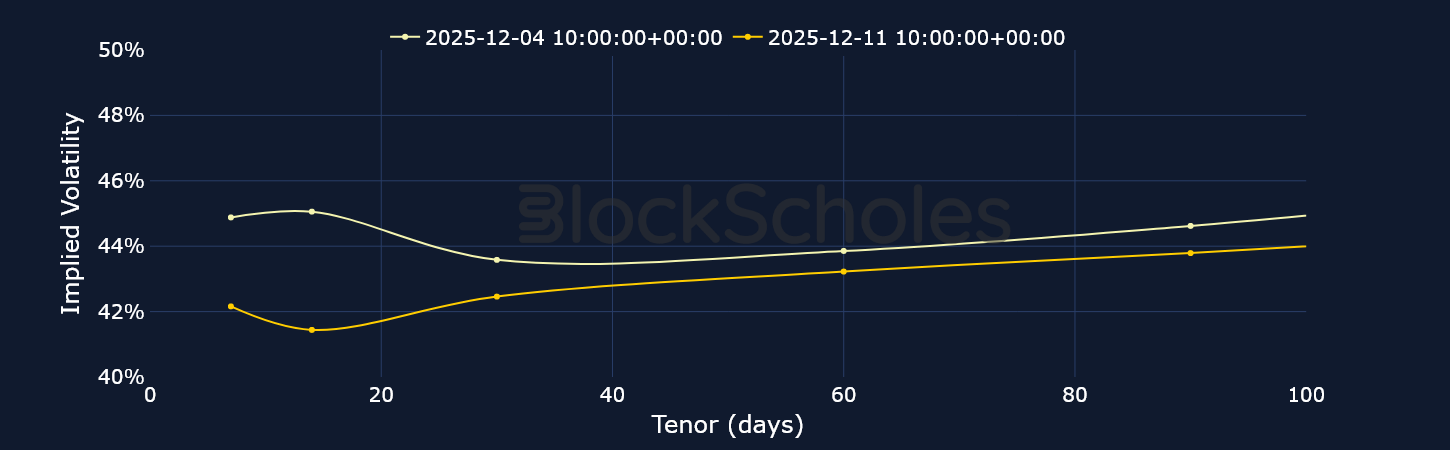

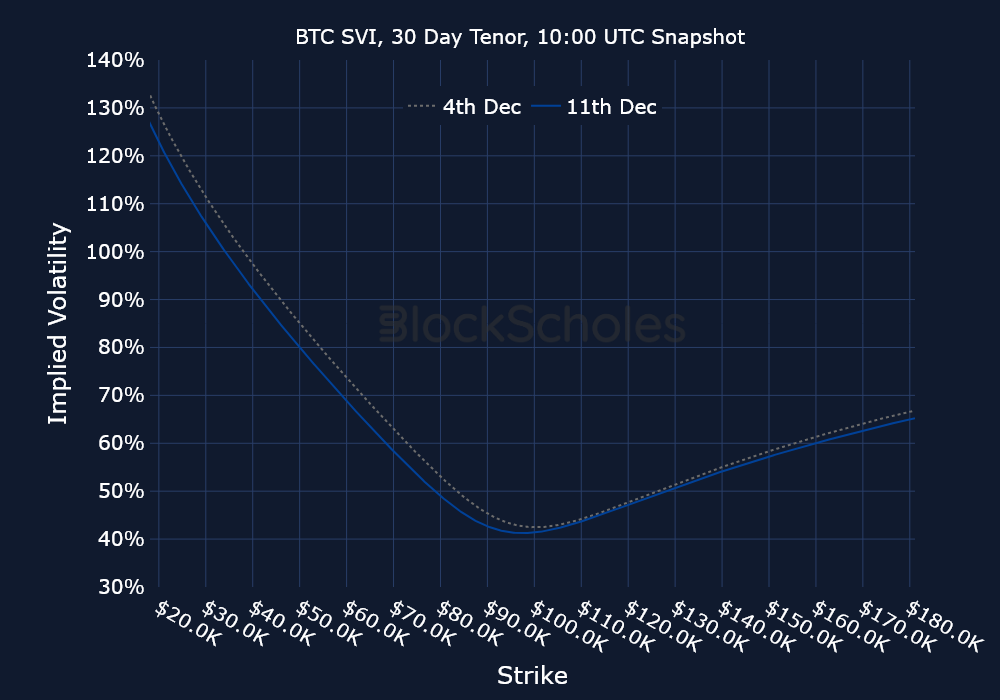

This week’s main event was the final FOMC meeting of the year. However, we did not see any obvious signs of the Fed’s meeting in the term structure of volatility. In fact, since Dec 7, 2025, ATM IV levels were on a steady downwards path. As such, the inversion in the term structure of volatility was very short-lived and since that local peak in early-December, the 7-day implied volatility level has fallen more than 13 points, currently trading at 42%. Both options volumes and trade volumes show an equal balance between calls and puts, a departure from last week where volumes in puts dominated BTC began the week trading sideways between $89K and $92K alongside US risk-on equities. That sideways trading might have been an indication of an unwillingness from traders to make any outsized bets ahead of the Fed’s meeting. However, by Tuesday 9 Dec, 2025, BTC eschewed the no-risk taking stance that defined price movement in US equities and rallied into the FOMC meeting, jumping past $94K. After the meeting however, we saw a slow drift in spot price back to $90K.

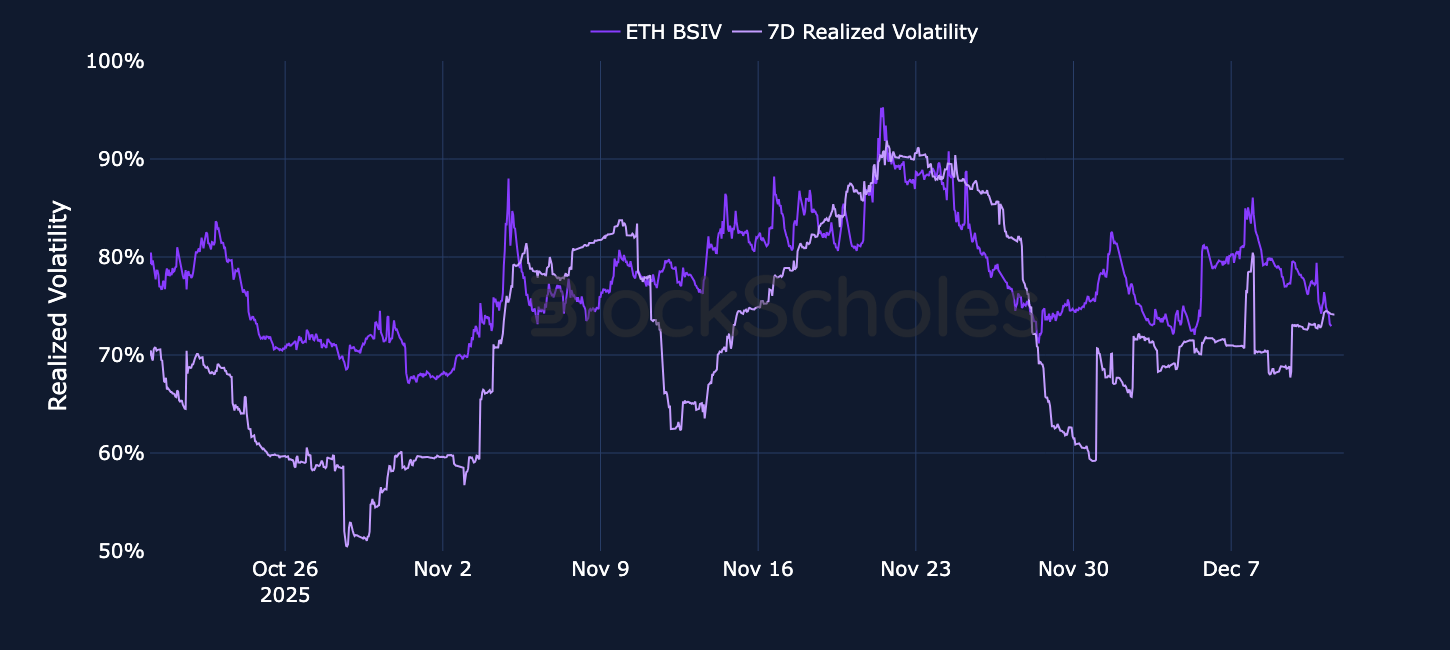

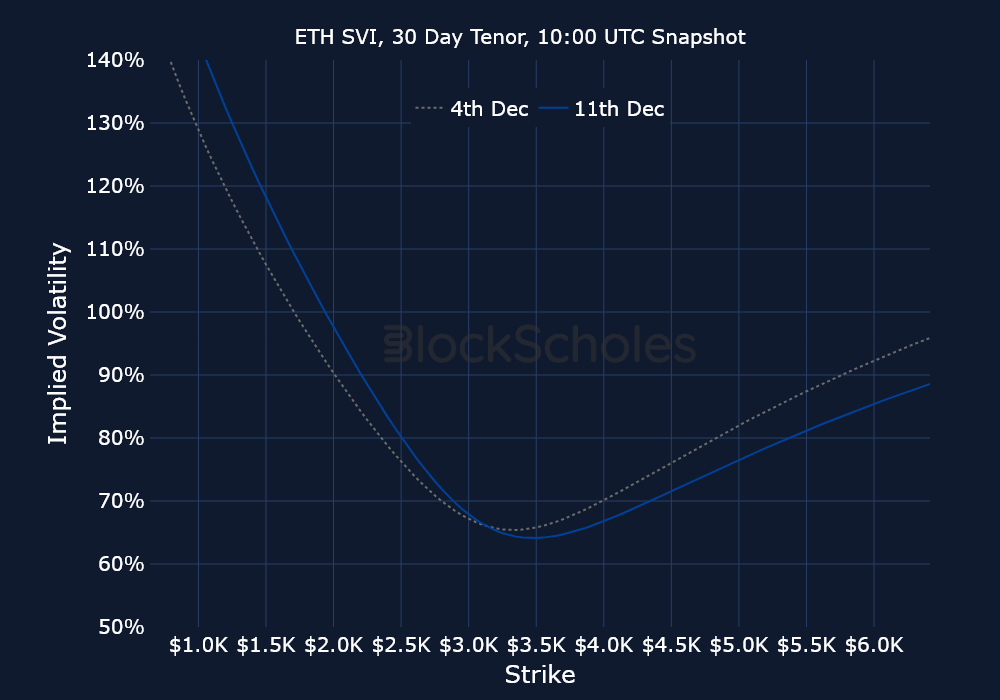

ETH’s term structure of volatility has exhibited very similar behavior to that of BTC, just at higher absolute levels. As such, we saw a similar short-lived inversion on Dec 7, 2025 during a late weekend rally in spot prices, before IV levels slowly drifted lower. For ETH, it means that 7D IV has fallen over 20 percentage points from the Dec 7, 2025 level of 78%. Over the past week, ETH’s spot price is up only 0.56%, with most of the pre-FOMC rally now having been pared back.

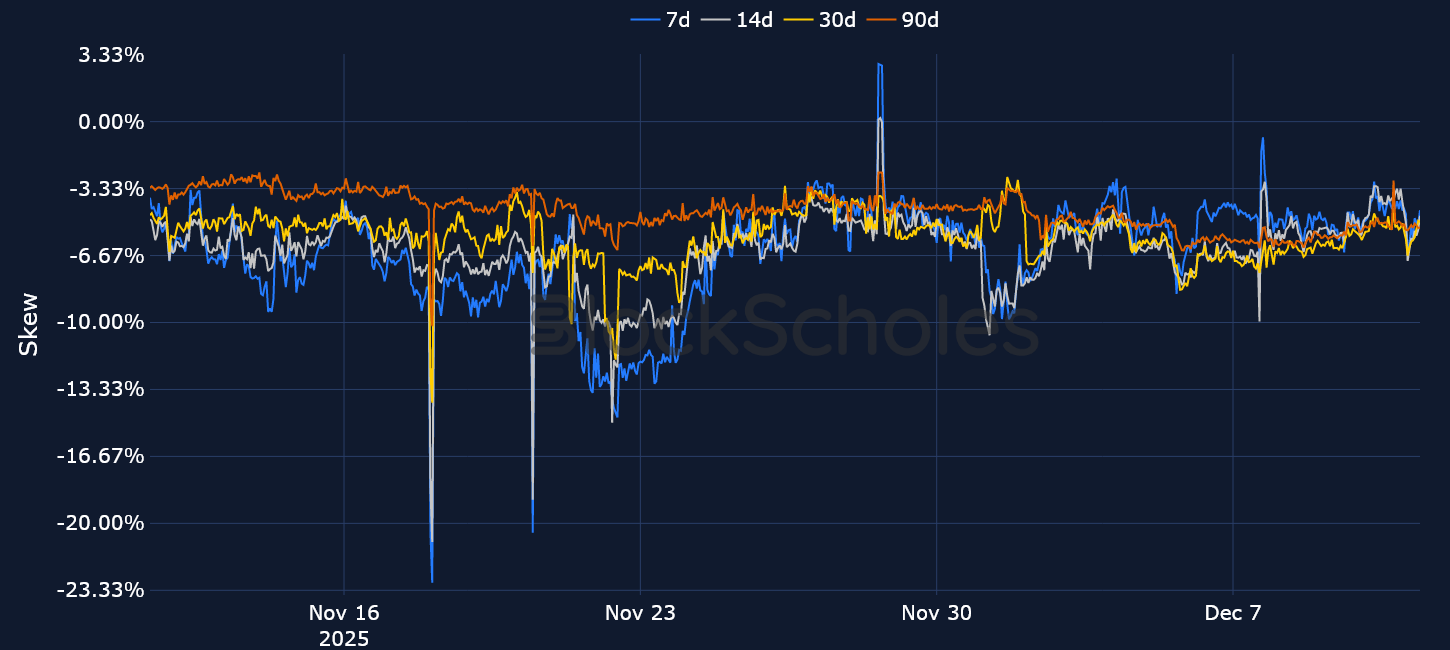

That sideways movement in spot price has meant that, even in spite of a press conference which could have certainly been more hawkish from Chair Powell, options traders are still not expecting any big upward moves in spot price before the end of the year. Implied volatility levels are dropping across the curve at all tenors, and volatility smiles continue to exhibit a significant premium for OTM puts.

Options markets are suggesting a tempering of expectations for those hoping for the ‘Santa rally’ that has typically accompanied previous BTC cycles. The December FOMC’s Summary of Economic Projections suggests that the median FOMC participant sees only one rate cut as appropriate in 2026, though markets (according to CME Fed Funds futures contracts) are still pricing in for two. Chair Powell said in his Q&A that “the effects of the 75bps will only begin to be coming in”, suggesting the cumulative three cuts this year by the Fed will continue to work their way through the economy.

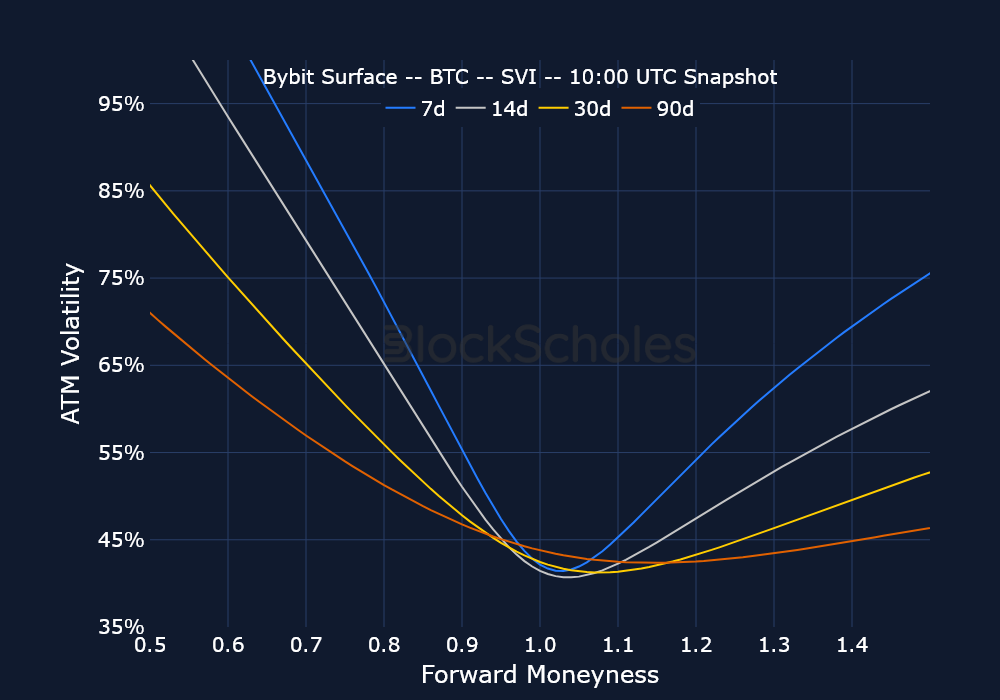

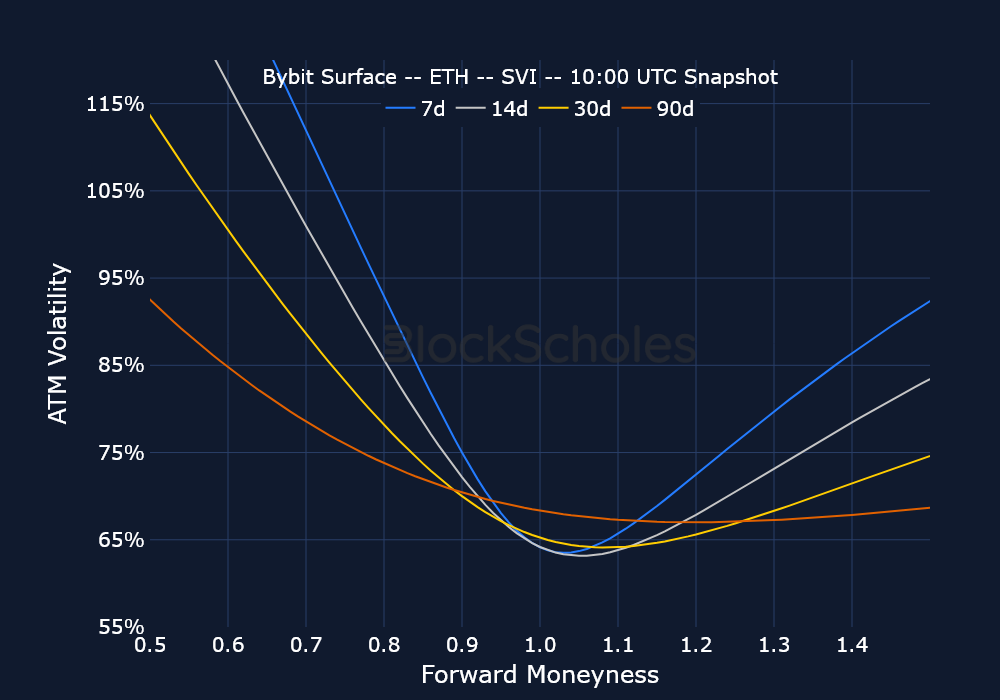

Still, volatility smiles paint a bearish picture across every time horizon: short-tenor smiles for BTC and ETH are skewed towards OTM puts by 4.4% and 4.8% respectively, while longer-dated 90-day options show a 5.3% premium and 5.0% premium towards put contracts, respectively. Ultimately, for now, traders are not seeing enough catalysts to help support the case of a Santa rally.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)