Thahbib Rahman

Research Analyst

A sideways slog in spot prices over the past week means that the bearishness in options markets positionings for both BTC and ETH continues. Volatility smiles across the term structure for BTC continue to price OTM puts at a premium to call options, while short-dated ETH options are also maintaining their expectations for further downside price action. The main driver of spot prices this week has been macro-induced events, on both sides of the Fed’s dual mandate. An ever so slightly hotter than expected CPI print pushed BTC lower after it tapped $114K, though it quickly recovered. The inflation print came after a slew of data releases pointed to a marked weakening in the US jobs market: including JOLTs data and NFP. Markets are now bracing for three rate cuts by the Federal Reserve by the end of the year.

A sideways slog in spot prices over the past week means that the bearishness in options markets positionings for both BTC and ETH continues. Volatility smiles across the term structure for BTC continue to price OTM puts at a premium to call options, while short-dated ETH options are also maintaining their expectations for further downside price action. The main driver of spot prices this week has been macro-induced events, on both sides of the Fed’s dual mandate. An ever so slightly hotter than expected CPI print pushed BTC lower after it tapped $114K, though it quickly recovered. The inflation print came after a slew of data releases pointed to a marked weakening in the US jobs market: including JOLTs data and NFP. Markets are now bracing for three rate cuts by the Federal Reserve by the end of the year.

The expected injection of liquidity from rate cuts has sparked a bigger upwards move in altcoins and less so in the majors BTC and ETH. Standout performers this week include SOL, which is up 11% on the week, and Worldcoin (WLD), both of which have outperformed on digital asset treasury announcements. A relatively unknown inventory-and-packaging company named Eightco Holdings was the company to announce the world’s first Worldcoin digital asset treasury, which sent its share price soaring higher too.

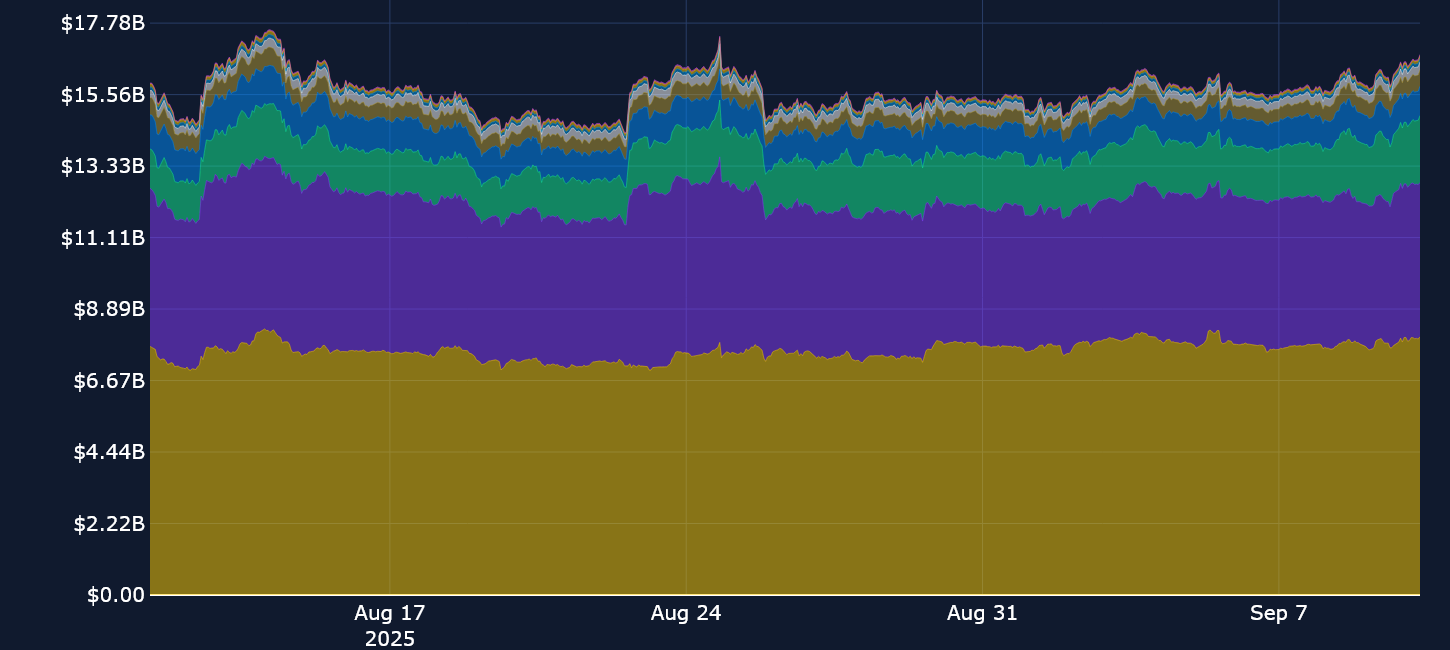

Perpetuals: Open interest in perpetuals has picked up from last week’s flat $15B, while daily trading volumes reached their monthly high following an anemic jobs data report from the US last Friday.

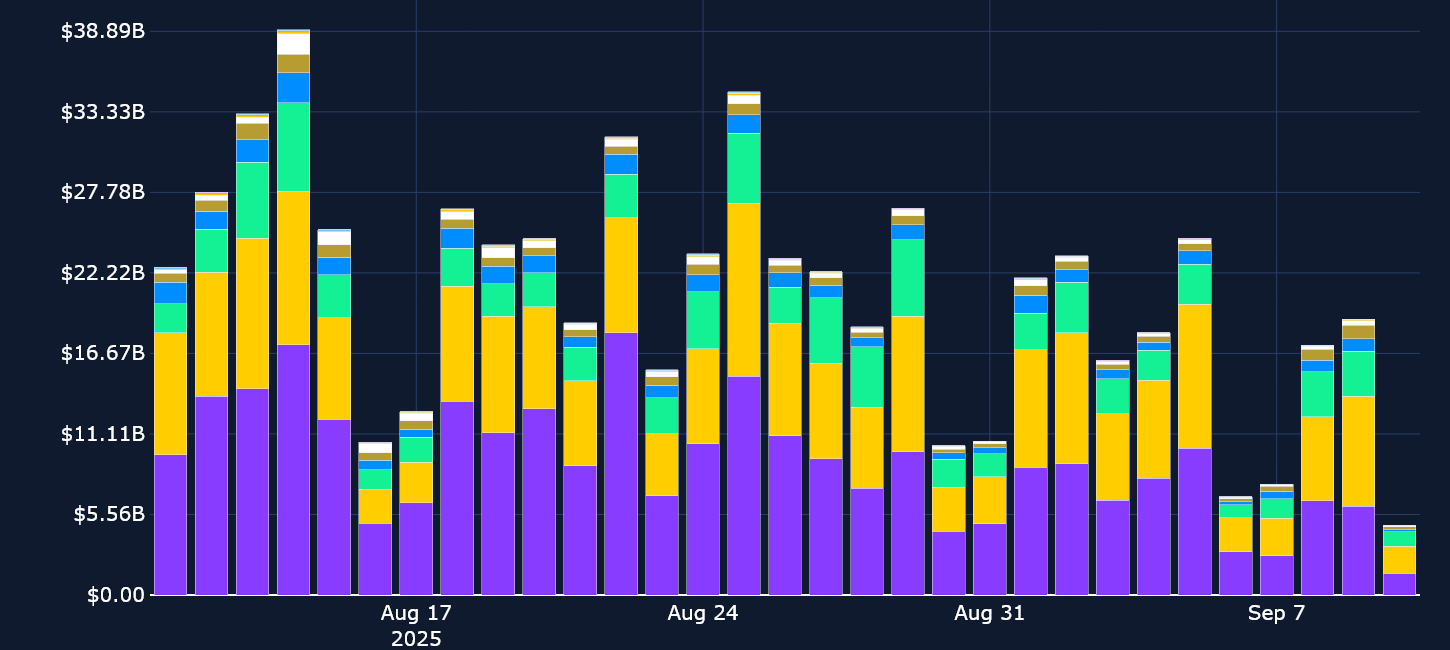

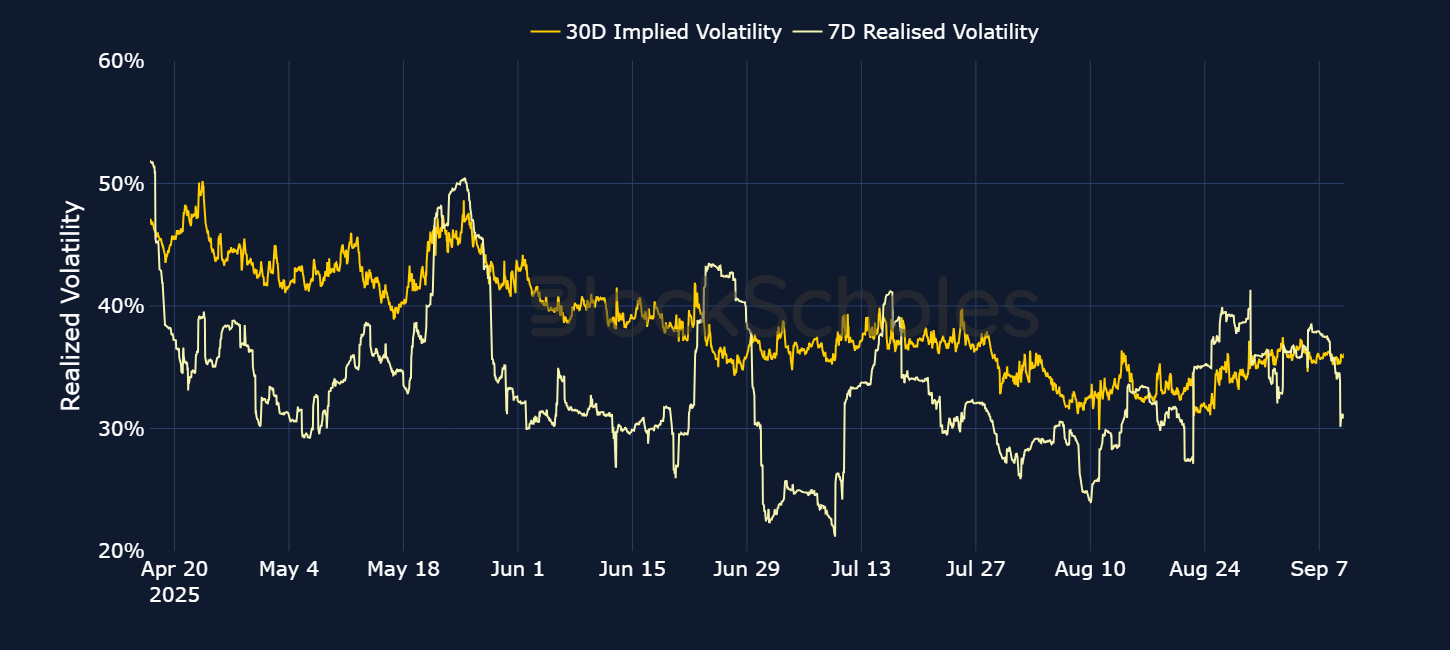

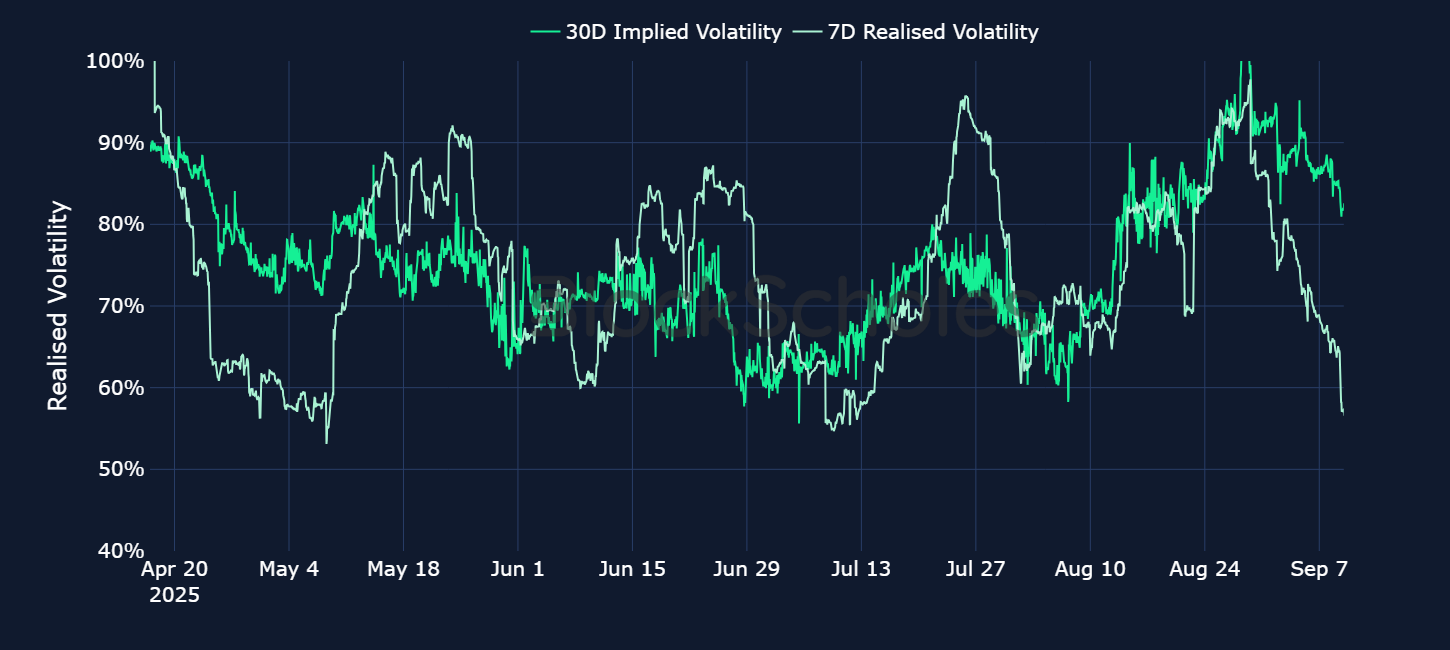

Options: It’s been another week of bearish positioning in options markets, which hasn’t been aided by range-bound spot prices. Both delivered and implied volatility across BTC, ETH and SOL have fallen over the past week.

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

Eightco Holdings, an inventory capital and management platform for e-commerce sellers, has surged as much as 2,700% over the past five days after announcing plans of a shares sale of $250M to buy and hold Worldcoin (WLD). WLD is the cryptocurrency behind the biometric digital identity project of OpenAI’s CEO, Sam Altman. Eightco Holdings said it would “implement the first-of-its-kind Worldcoin treasury strategy.” The largest ETH treasury company, Bitmine Immersion Technologies, Inc., has purchased 13.7 million common shares of Eightco for $20M, a sign of its backing of the project.

Together, the news sparked a dramatic move in Worldcoin’s token. Over the past seven days, frenzied buying has sent the WLD token 111% higher. On Sep 8, 2025, prior to the announcement, WLD had been trading sideways between $0.90 and $1 for the past six months.

Despite an eye-watering rally however, those who had purchased Worldcoin back in March 2024 — during the peak of meme coin mania and a market-wide crypto rally following the launch of BTC Spot ETFs — are still down significantly. The WLD token reached its all-time high of $11.74 on Mar 11, 2024, and has since lost nearly 90% of its value.

Open interest in leveraged swaps markets has risen by just over $1B after lingering last week around the $15B mark. Then, it was macro uncertainty and a global rise in government bond yields that stopped traders from placing any outsized bets. This week, the slight increase in open interest has occurred despite a backdrop of mainly range-bound spot prices. Over the past seven days, BTC mainly traded between $109K and $113K, and only broke out to $114K in early Asian trading hours on Sep 11, 2025. Meanwhile, Ether has continued to trade at between $4,200 and $4,500 over the past week, and is up 3% on the month, relative to a 4% decline for BTC.

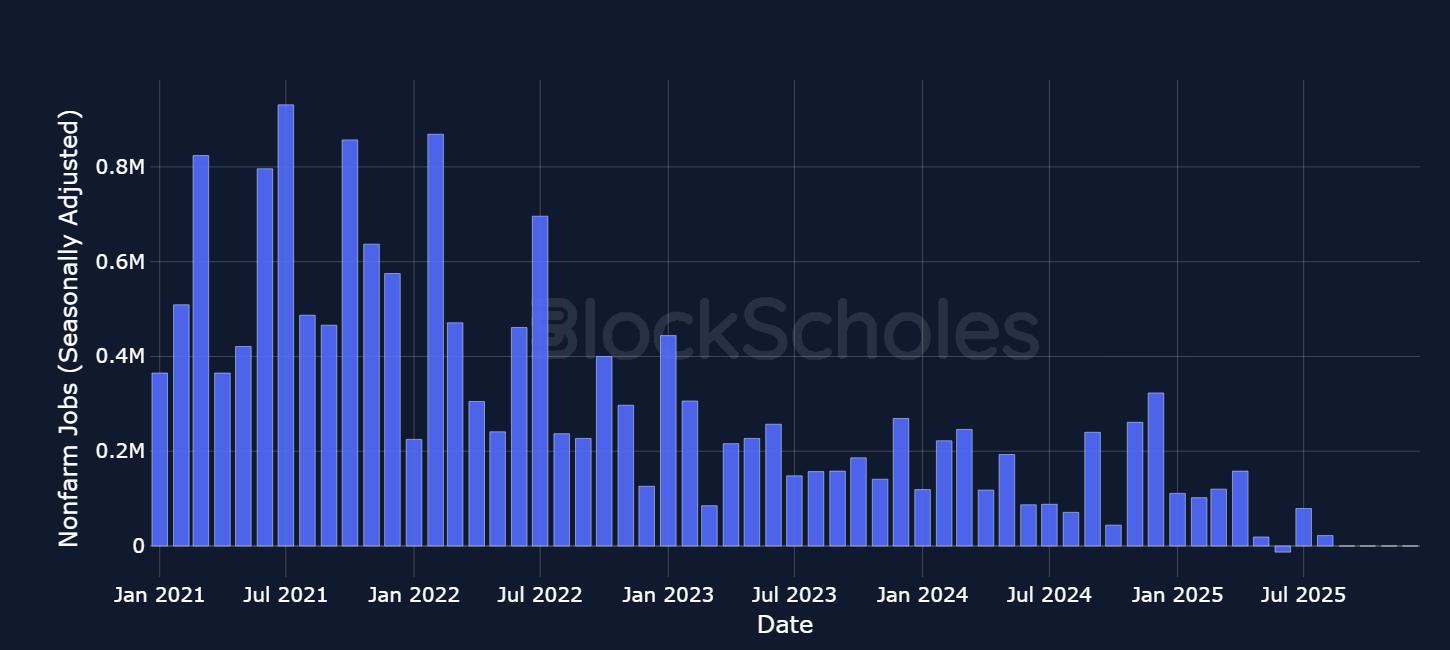

Macro narratives have been the main driver for spot prices since the start of September, as reflected in derivatives market positioning with daily trade volumes reaching their highest levels so far this month on Friday, Aug 5, 2025. That day, the latest nonfarm payrolls report in the US showed that payrolls had increased by only 22,000 in August, far below expectations of 75,000. Meanwhile, June saw negative job growth, the first time this has occurred since December 2020. BTC initially rallied before falling from $112K to $110K.

BTC funding rates continue to maintain a mostly neutral stance, with a slightly bullish tilt and an appetite for higher prices. This is reflected in the fact that funding rates have been positive all week, though they’ve failed to break out past 0.01%, a sign of a more exuberant view for a rally in spot prices. After some early shakiness from traders in the ETH leveraged instrument during the tail end of August and initial part of September, ETH funding rates have also stabilized at neutral-to-positive levels.

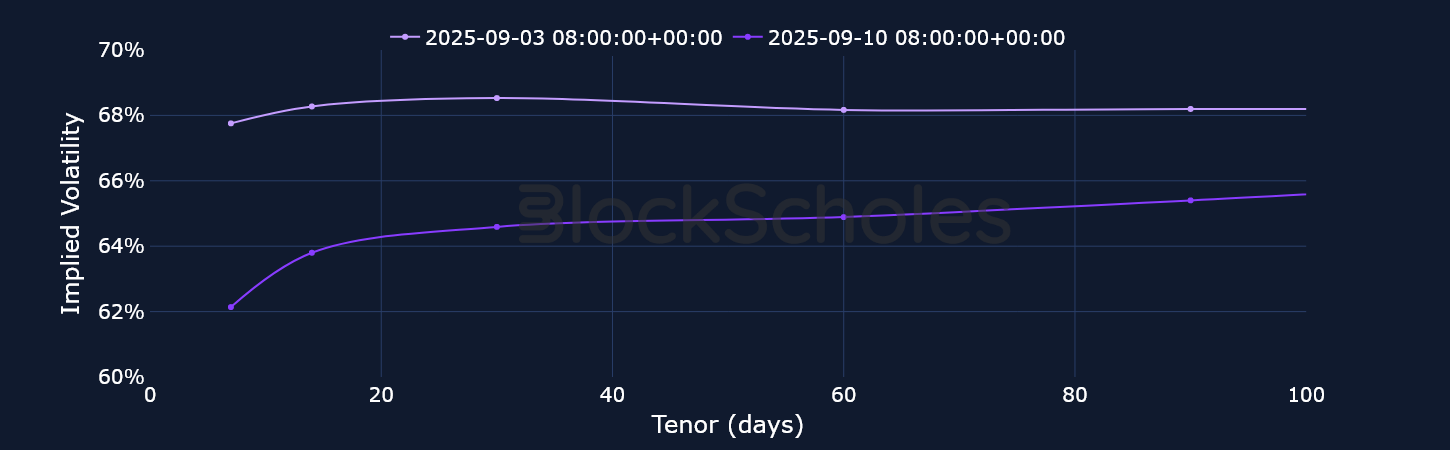

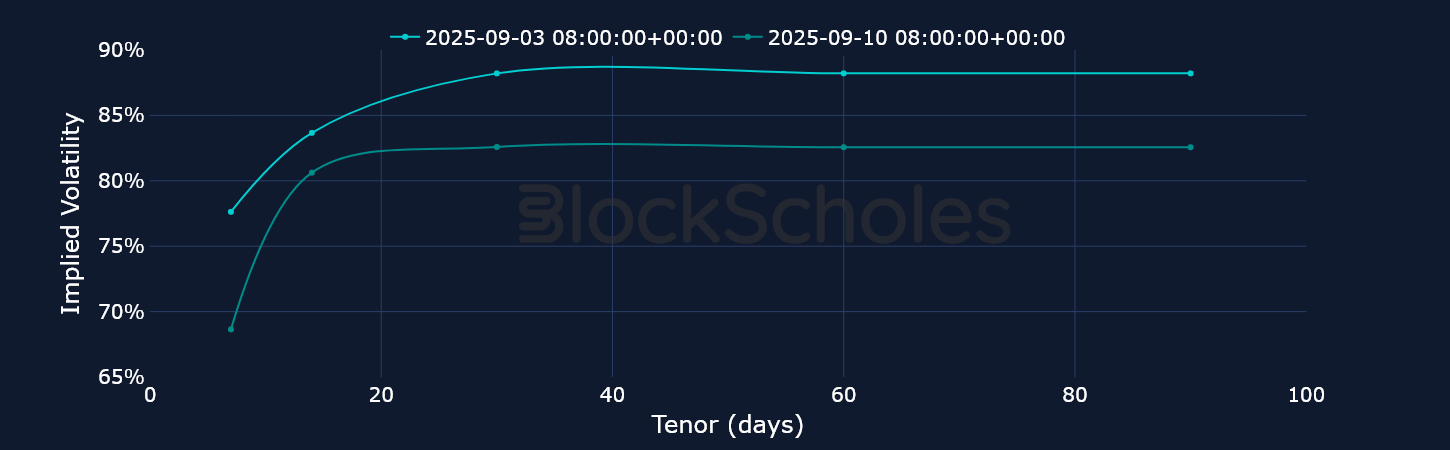

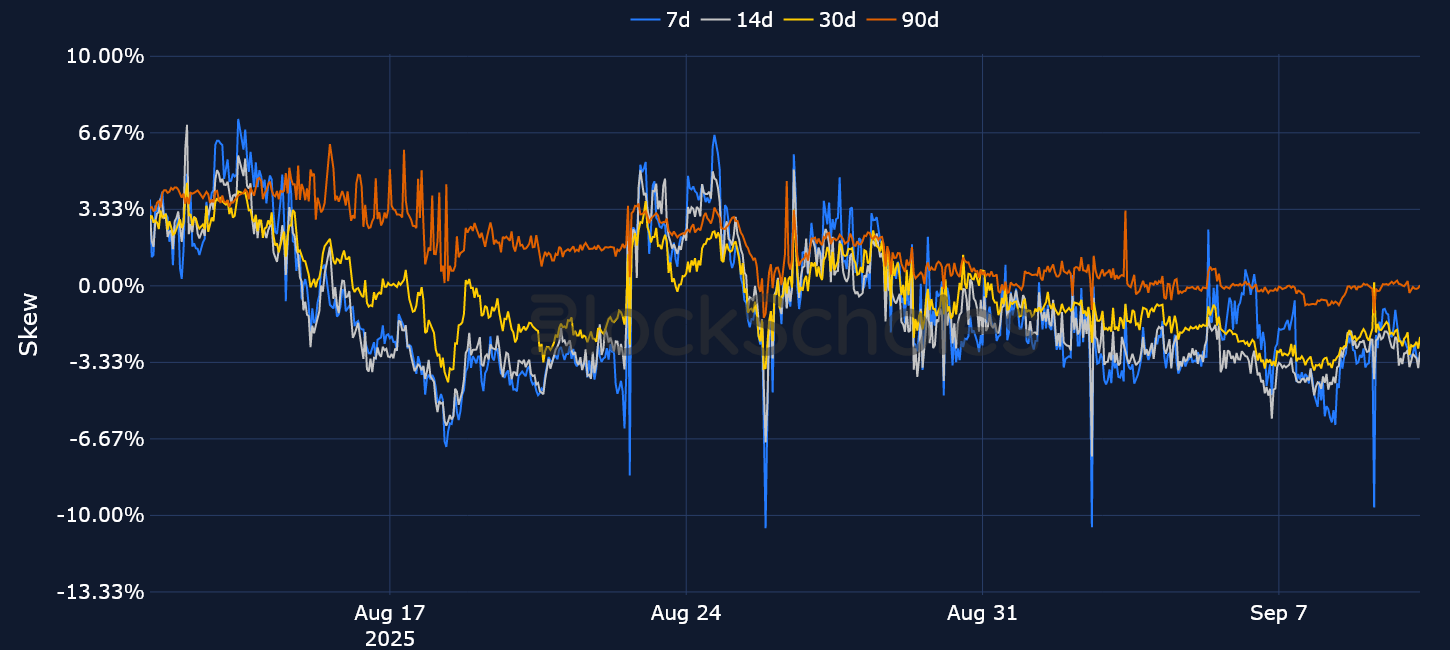

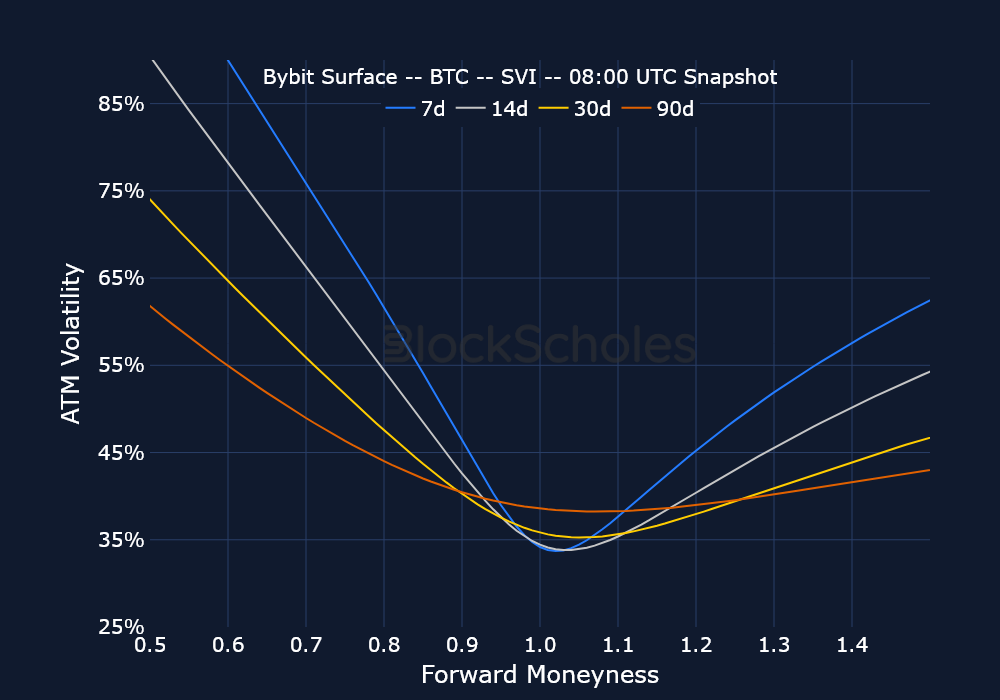

Perhaps the more interesting divergence is between options markets and perp markets. The sideways movement in spot prices for BTC and ETH has culminated in declining levels of ATM implied volatility, while volatility smiles still suggest traders are bracing for more downside price action. Since the start of September, short-tenor BTC and ETH skews have failed to increase above 0% (i.e., OTM calls trading more attractive to puts) for any sustained period of time. That contrasts with the positioning in perpetual swaps, as a sideways spot price hasn’t turned traders bearish just yet.

Bearish positioning continues to dominate BTC options, despite a run of softer-than-expected macro data releases that have pushed the market to price in nearly three rate cuts before year’s end by the Federal Reserve — which typically provide a favorable backdrop for risk-on sentiment. JOLTS data showed job openings fell to 7.18M in July, the lowest level in ten months, while last Friday’s nonfarm payrolls report informed us that June was the first negative month for jobs growth since December 2020.

For most of the week, BTC’s failure to break out of its $109–113K range hints at the tug-of-war that traders are currently facing. A US economy that’s too weak bodes ill for US equities as consumer spending and the labor market slow down, while a more controlled slowdown may boost risk-taking via increased liquidity from interest rate cuts. There is also another tug of war between inflation and employment. On Sep 11, 2025, core CPI came in as expected, though the headline number exceeded expectations on the month. That occurred while an initial jobless claims report showed unemployment filings close to a four-year high (more weakness in the labor market). Volatility smiles for BTC have remained tilted toward OTM puts for most of September — and not just for short-dated options either. The bearish sentiment is across the term structure, and began in mid-August.

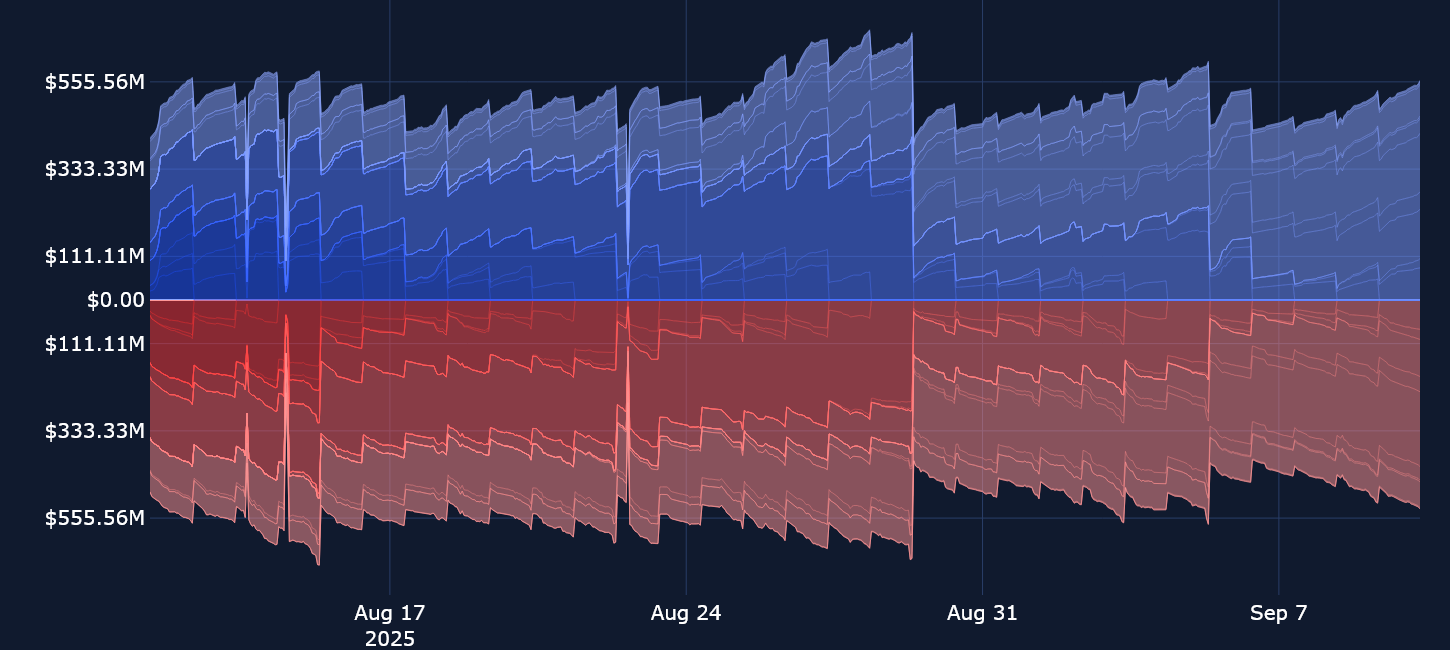

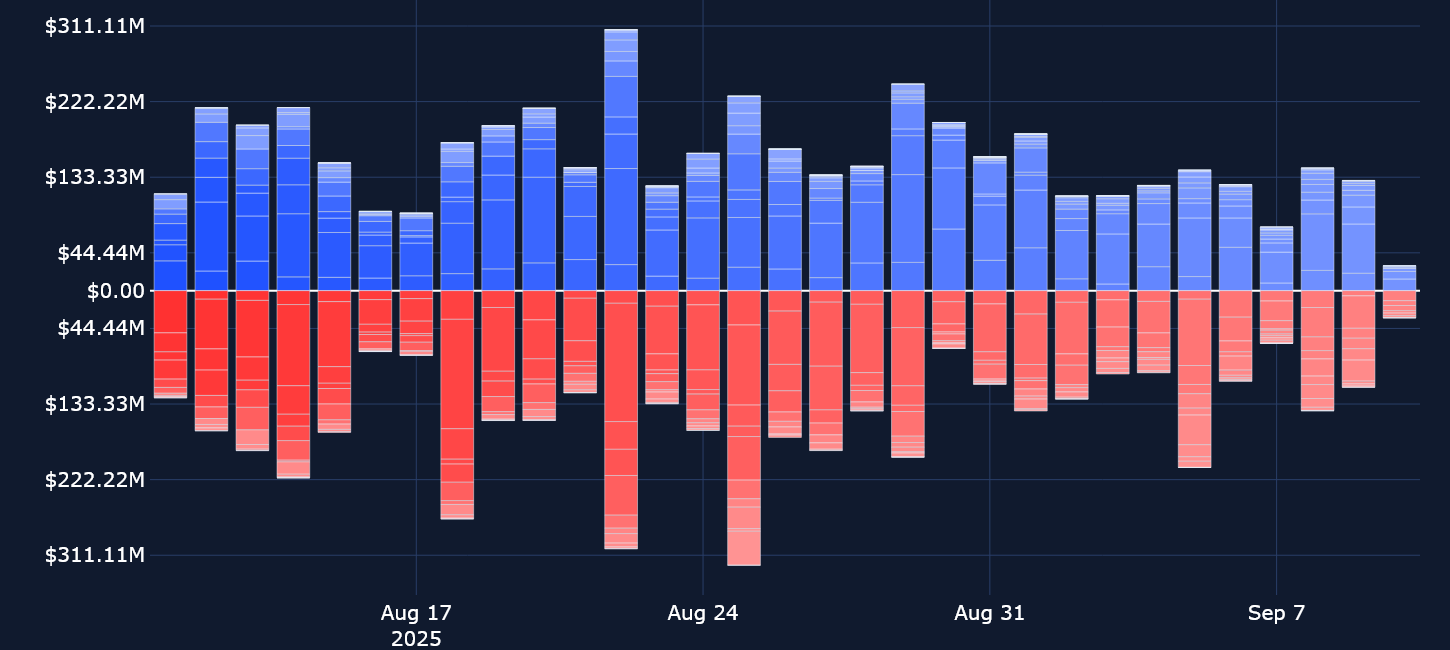

BYBIT BTC OPTIONS OPEN INTEREST

We mentioned that BTC and ETH spot prices have mainly been in a sideways sloth over the past week. Nonetheless, ETH has underperformed relative to BTC. While the latter is up a slight 0.8%, ETH is down 1.0%. The two assets’ spot ETF markets have also diverged in their net flows. As a matter of fact, only yesterday were Spot Ethereum ETFs able to break a six-day outflow streak, driven partly by sizable outflows from BlackRock’s Shares Ethereum Trust ETF.

On Tuesday, Sep 9, 2025, Spot ETH ETFs purchased $44.2M worth of Ether. Bitcoin Spot ETFs, on the other hand, have had a slightly less bearish run. Of the six consecutive ETH outflow days, Bitcoin products net bought BTC on three days, and yesterday the funds purchased $23M of bitcoins, primarily due to a $169.3M inflow from BlackRock.

Unlike BTC options volumes, which saw a jump higher last Friday following the NFP report in the US, ETH options volumes have stayed steady around the $133M mark, while open interest has also remained flat.

The decline in ATM implied volatility across SOL’s term structure mirrors both a major decline in realized volatility for SOL and the wider drift lower in implied volatility across the three major crypto assets. Solana’s native SOL token has, however, held up far better than BTC and ETH: on the week, it’s rallied more than 11% from a low of $199 to now trading shy of $220, and in the past 30 days, SOL is up 27%.

Part of SOL’s outperformance may be attributed to Monday’s announcement that Nasdaq-listed Forward Industries (FORD), a design and manufacturing company, has raised $1.65B in cash and stablecoin commitments — led by Galaxy Digital, Jump Crypto and Multicoin Capital — to form the largest SOL-focused digital asset treasury company. The company also aims to generate on-chain returns and increase long-term shareholder value through active participation in Solana’s DeFi markets, which could provide a boost to the entire Solana ecosystem.

As has been the case since mid-August, we continue to see bearish expectations in BTC and ETH options markets. That skew turned slightly more negative following the CPI print in the US. Volatility smiles for both assets are reflecting a far higher demand for short- and long-term downside protection than for bets on a spot price rally. The notable contrast is in longer-dated optionality: the 90-day put-call skew for ETH is flirting with the 0% mark, without showing a strong willingness to firmly price puts richer than calls. That contrasts with the positioning in BTC longer-maturity options, where (for example) 90-day skew is firmly tilted bearish at −2%.

Nonetheless, for BTC we do see a recovery in skew over a longer time horizon. Back on Aug 25, 2025, 7-day skew was as low as −10%, with BTC’s spot price later falling to $107K.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)