Thahbib Rahman

Research Analyst

A record-breaking liquidation event in crypto’s history has certainly taken its toll on perpetual swap contract markets, with Bybit traders showing almost no willingness to re-enter lost leveraged positions. More than $6B in notional positions were wiped out on Oct 10, 2025, ignited by a re-escalation of trade tensions between the US and China. Those tensions eased earlier this week as US and Chinese negotiators agreed on a “very positive framework” for discussions between President Xi and President Trump — that then set the table for a much anticipated trade deal between the two nations that was signed on Oct 30, 2025.

A record-breaking liquidation event in crypto’s history has certainly taken its toll on perpetual swap contract markets, with Bybit traders showing almost no willingness to re-enter lost leveraged positions. More than $6B in notional positions were wiped out on Oct 10, 2025, ignited by a re-escalation of trade tensions between the US and China. Those tensions eased earlier this week as US and Chinese negotiators agreed on a “very positive framework” for discussions between President Xi and President Trump — that then set the table for a much anticipated trade deal between the two nations that was signed on Oct 30, 2025.

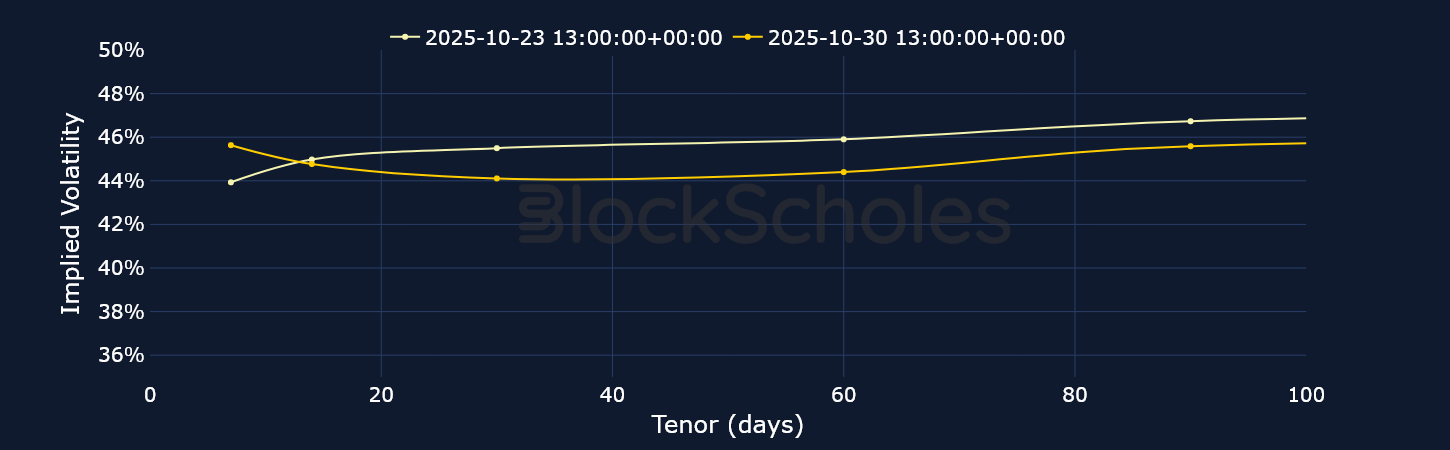

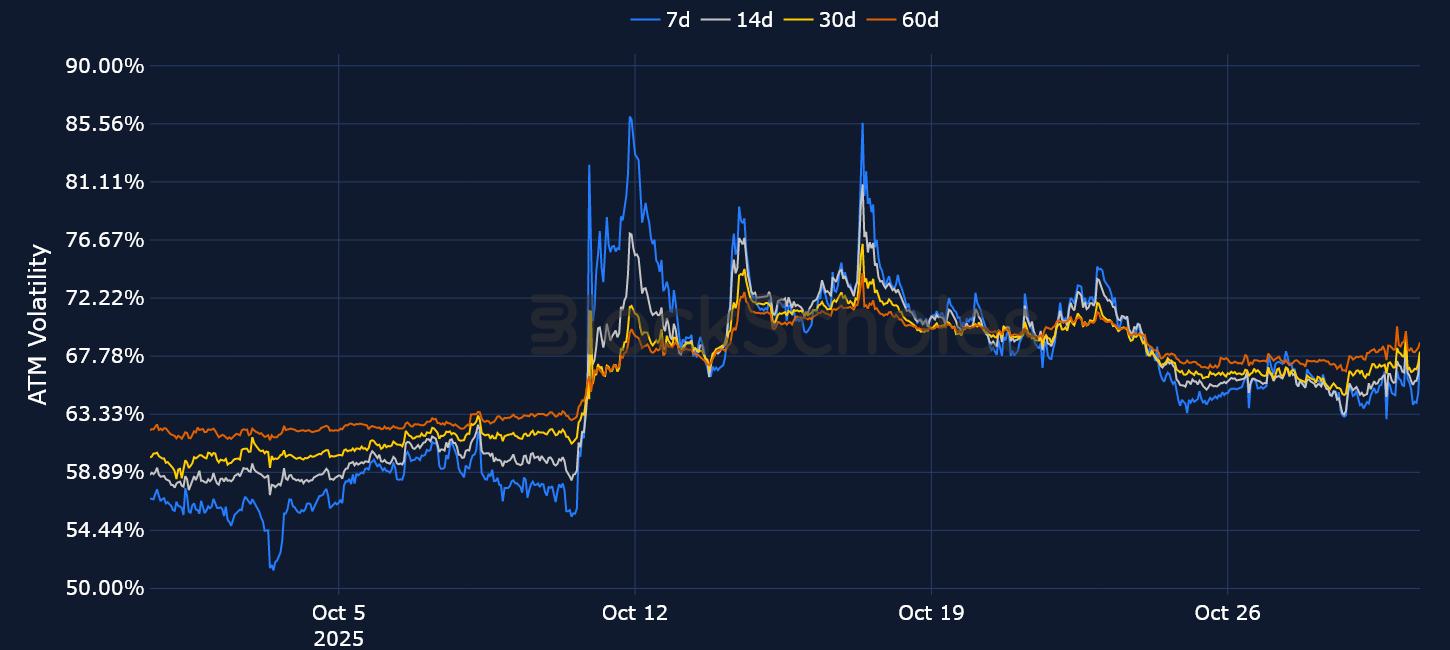

Nonetheless, sentiment appears to have been overpowered by Federal Reserve Chair Jerome Powell’s more hawkish stance in the mid-week FOMC press conference. While delivering a 25 bps rate cut, Powell said that the decision for December “is not a foregone conclusion — far from it.” Markets have not taken kindly to those comments, as BTC fell to $107K and the short-tenor put-call skew ratio is skewed toward puts by as much as 6.5%. That’s a major reversal from sentiment only a few days ago, when 7-day smiles temporarily switched from bearish to bullish.

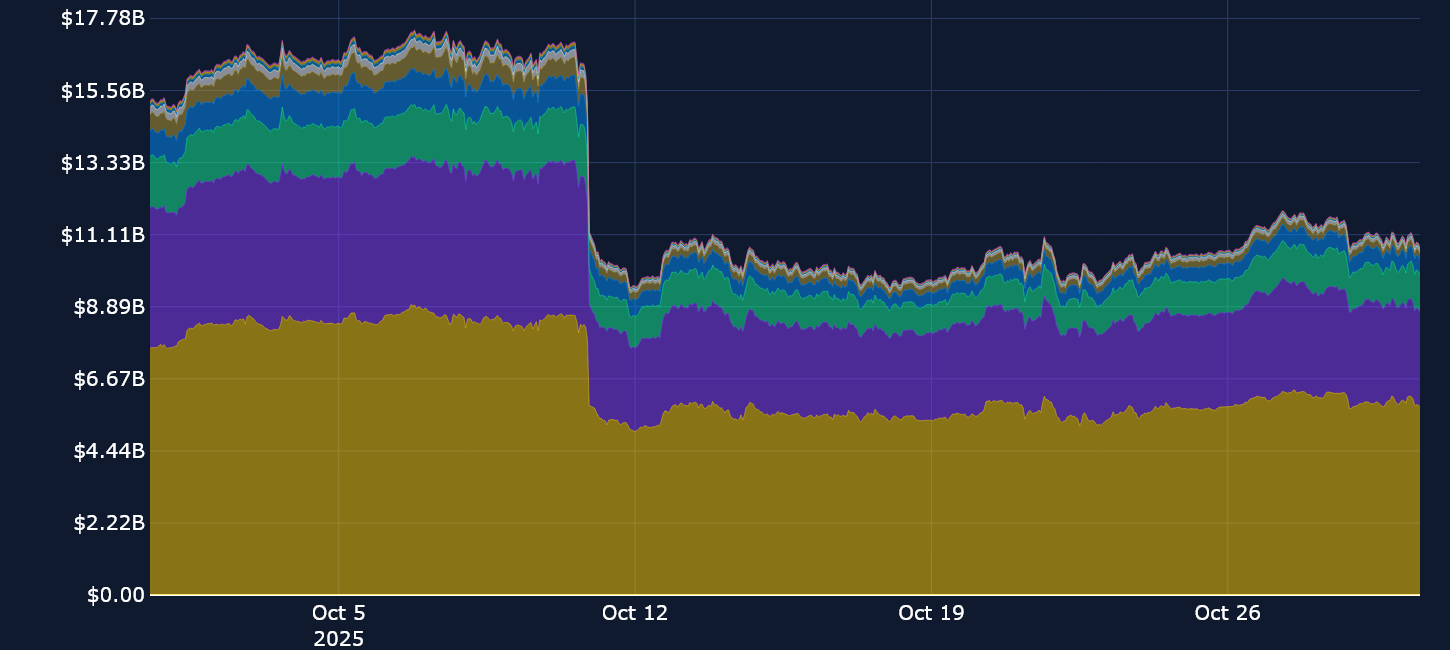

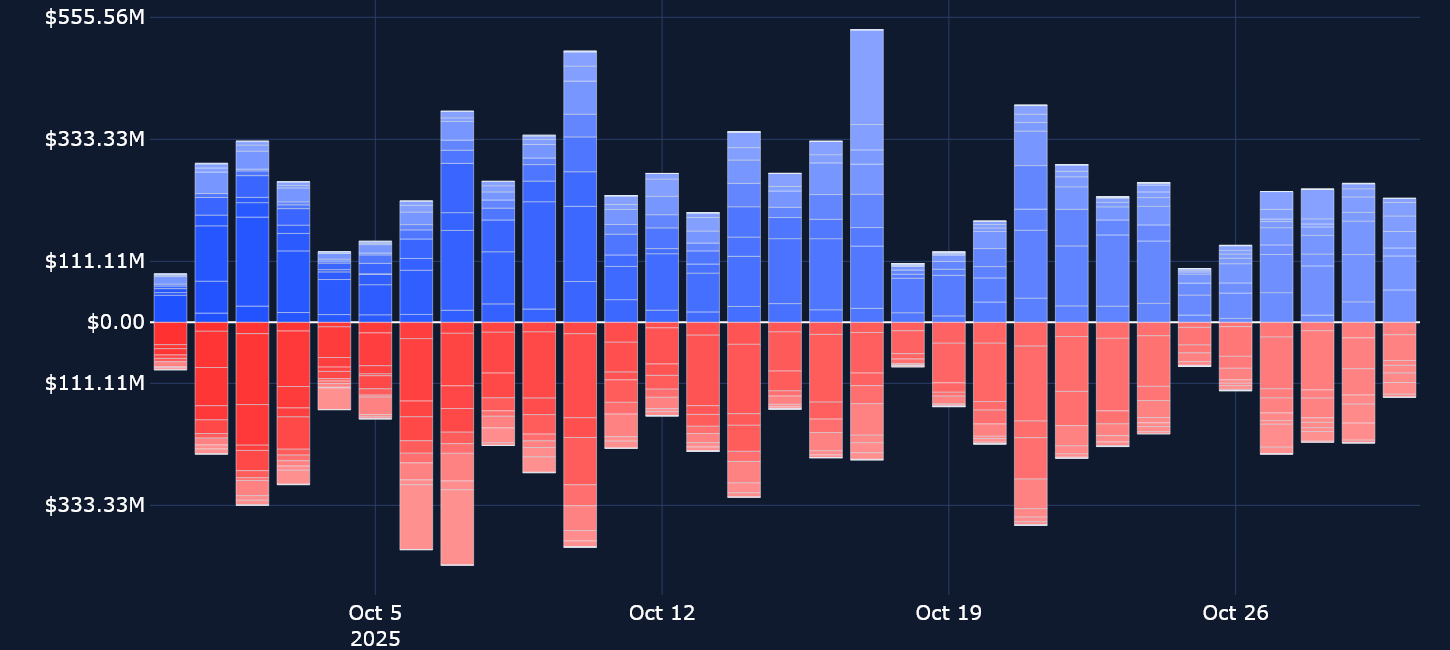

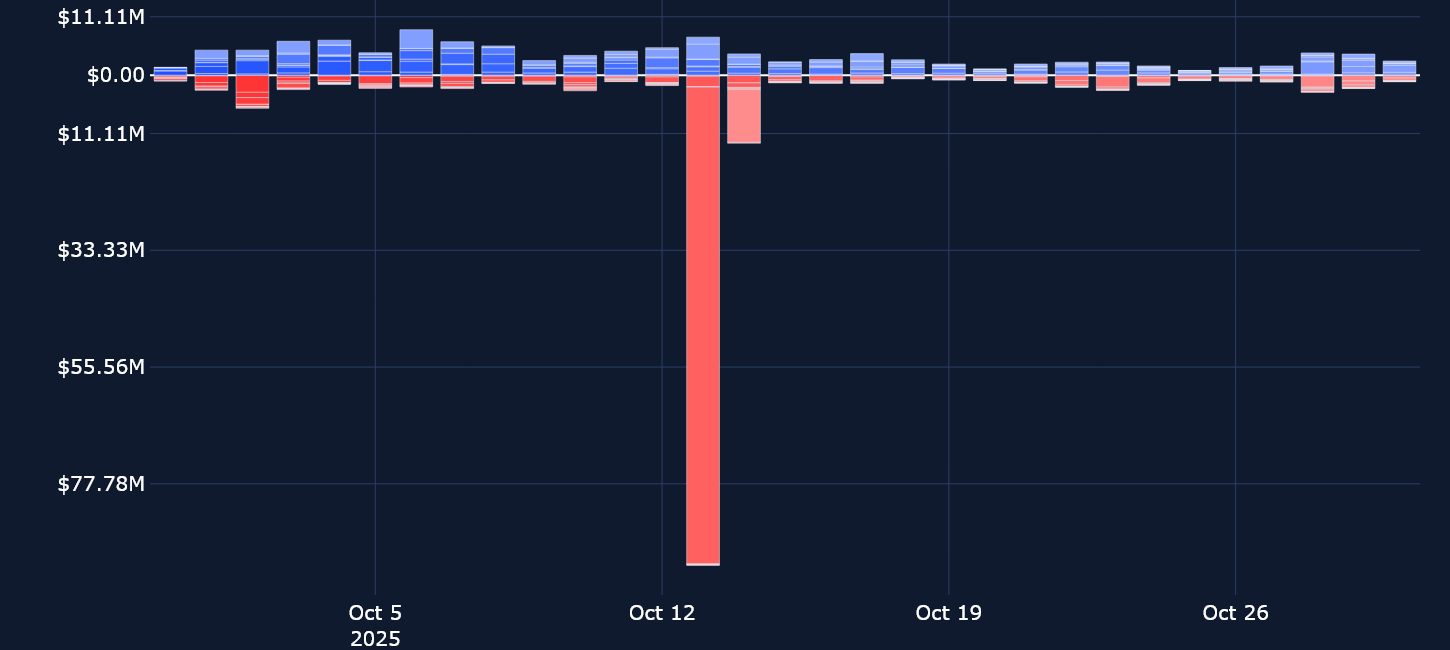

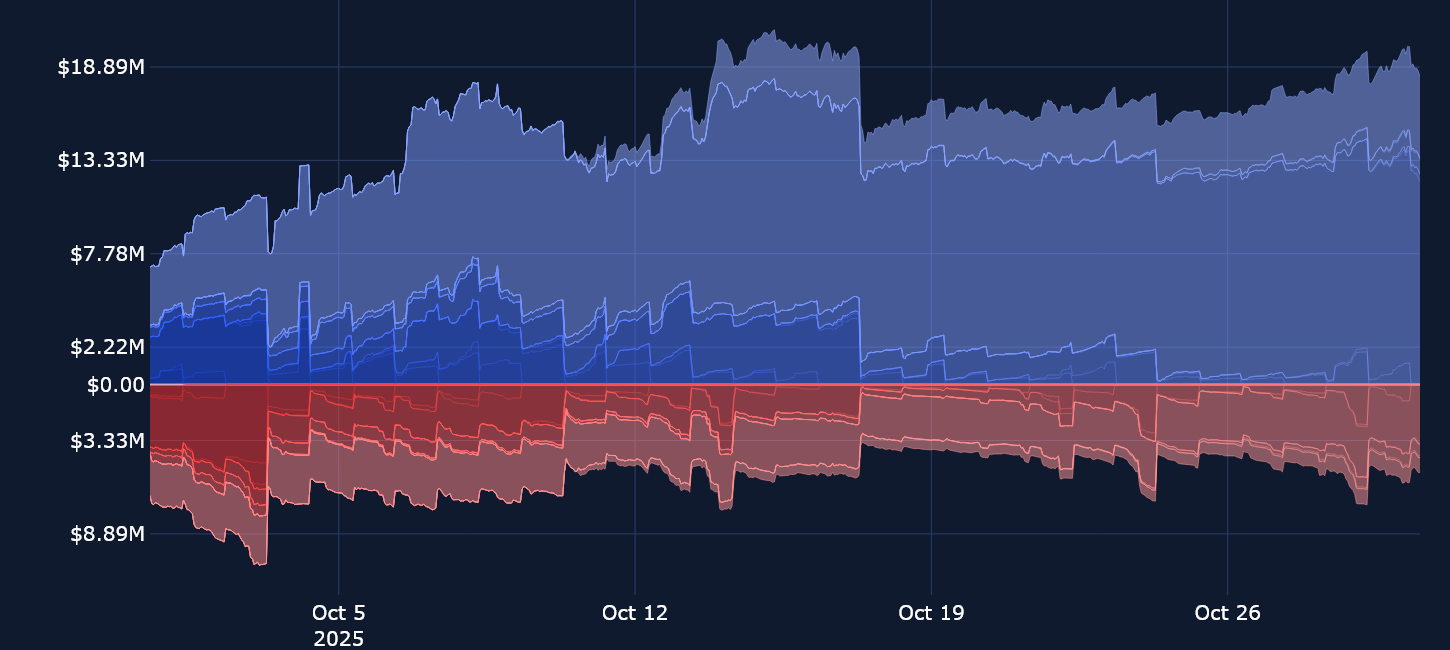

Perpetuals: Open interest fell by more than $6B following the largest crypto deleveraging event in history, and has since flatlined around $10B.

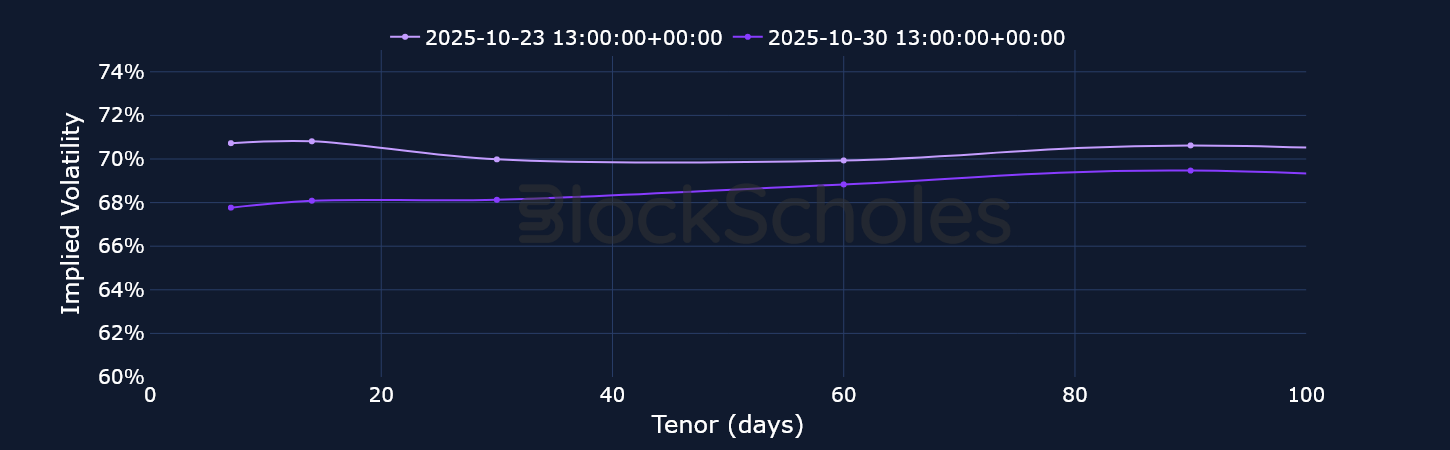

Options: BTC and ETH volatility smile skews priced out much of their bearish sentiment over the past week, even tilting temporarily toward calls. That skew toward OTM calls was short-lived, however, and traders continue to expect more downside. ATM implied volatility also remains elevated for both BTC and ETH (relative to the start of the month), though neither asset’s term structure of volatility remains inverted.

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

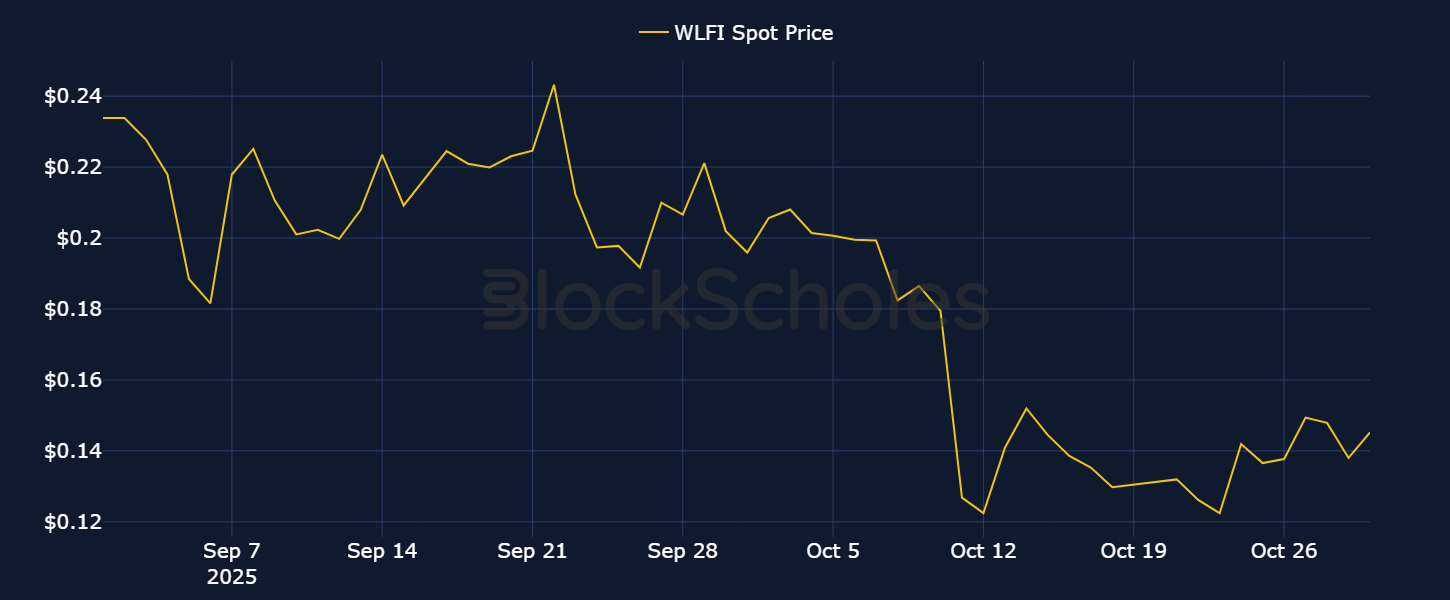

The World Liberty Financial protocol is a DeFi platform backed by the Trump family. WLFI, the governance token backing the platform, is down nearly 30% since its launch, but has recently outperformed the market. Since reaching a local bottom of $0.12 on Oct 23, 2025, WLFI gained 25%, jumping up to $0.15 earlier this week.

On Oct 30, 2025, World Liberty Financial announced that it would distribute 8.4M WLFI tokens as an airdrop to early participants in its USD1 points program, which rewarded users who traded with or held USD1, a stablecoin backed by the owners of the WLF protocol. Additionally, in mid-September, the protocol’s governance community approved a buyback and burn proposal that directs 100% of the fees earned from liquidity pools owned by the protocol on Ethereum, with Solana and BNB Chain to be used for purchasing WLFI tokens and burning them. The burn program will permanently reduce the amount of tokens in circulation, and is part of a wider trend of buybacks from many DeFi protocols to increase the value of their tokens.

Despite the recent spot price outperformance, funding rates on perpetual contracts linked to the WLFI token have fluctuated between a bearish and bullish regime — indicating a lack of clear conviction among traders as to whether the token can sustain its rally.

The record-breaking $19B crypto liquidation event on Oct 10, 2025 (initially triggered by President Trump’s announcement of an additional 100% tariff rate on China) has had a long-lasting impact on the perpetual swap market. More than two weeks after $6B in notional positions were wiped out on Oct 10, 2025, there are few signs that traders have any appetite to reopen positions.

Much of the range-bound notional open interest below $10B has coincided with sideways trading in BTC and ETH. Since Oct 10, 2025, BTC has mostly traded between $105K and $115K, and has struggled to break past that upper resistance level — despite US equities (to which crypto has been strongly correlated) closing at record highs for two consecutive trading sessions this week. Both are now bleeding lower following the Fed’s most recent FOMC meeting, which was far more hawkish than most market participants had expected. This has pushed the prices of BTC and ETH as low as $107,000 and $3,800 (respectively).

It’s interesting that the proportion of open interest dominated by BTC hasn’t changed following the liquidation event. Open interest was split almost evenly between BTC and the eight tracked altcoins prior to President Trump’s re-escalation of trade tensions, and remains roughly the same as we approach the end of the month.

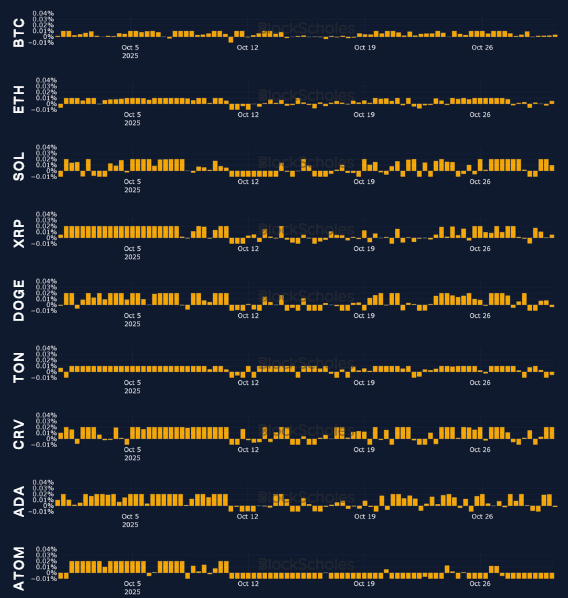

In line with the historic flush-out of leveraged perpetual futures positions, funding rates turned negative in the weekend of President Trump’s re-escalation of trade tensions. That marked a reversal in sentiment for many tokens that hadn’t seen negative funding rates up to that point in the month — a show of renewed bearish sentiment as perpetual swap traders were willing to pay a premium in order to stay short. Recent developments in trade tensions, however, including a “very positive framework” being agreed to between Chinese and US negotiators (and later a trade deal between President Trump and Xi) have received a mixed response.

For BTC, funding rates have returned to positive, though not to euphorically bullish levels. Other major altcoins, such as ETH and SOL, have fluctuated around neutral levels. This matches a similar sentiment in options markets, where volatility smile skews reversed much of the bearish positioning over the past week — though failing to turn distinctively bullish for a sustained period of time. The lack of major recent moves in funding rates in either direction may also be a reflection of the general decline in participation rates — an observation that has evidence in the failure of open interest to pick up.

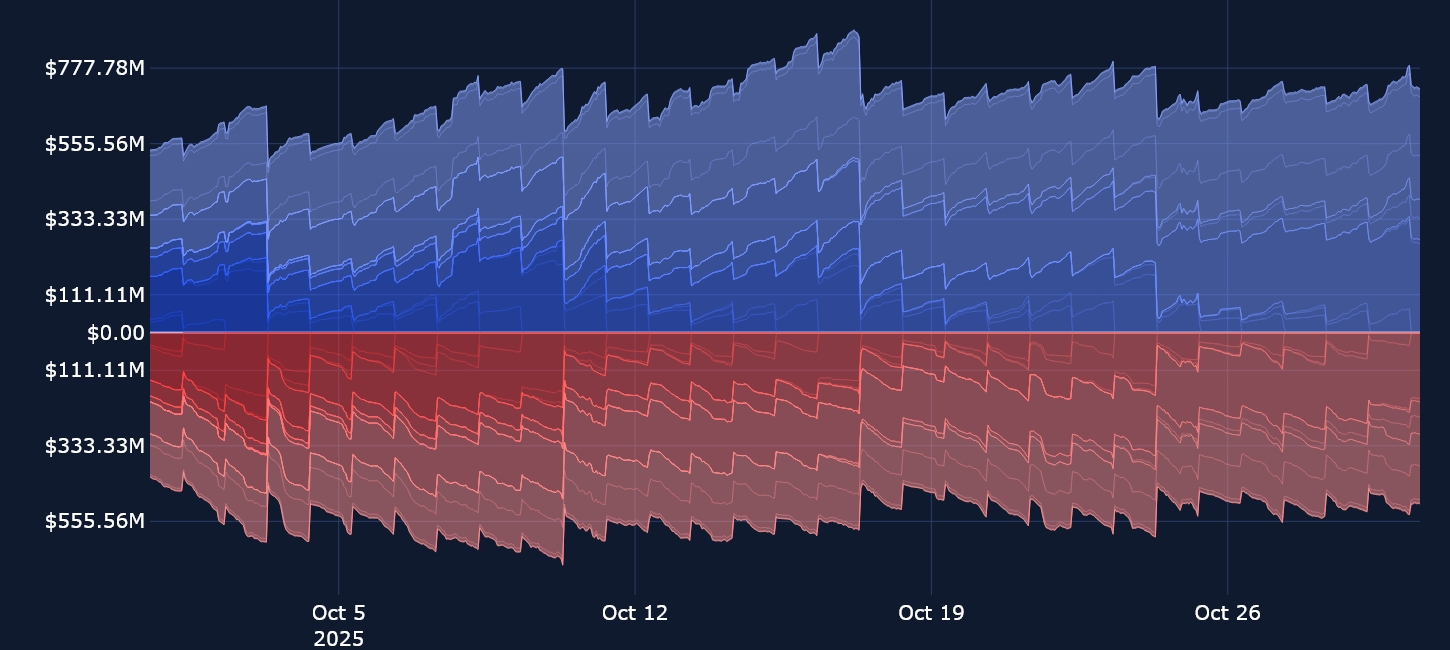

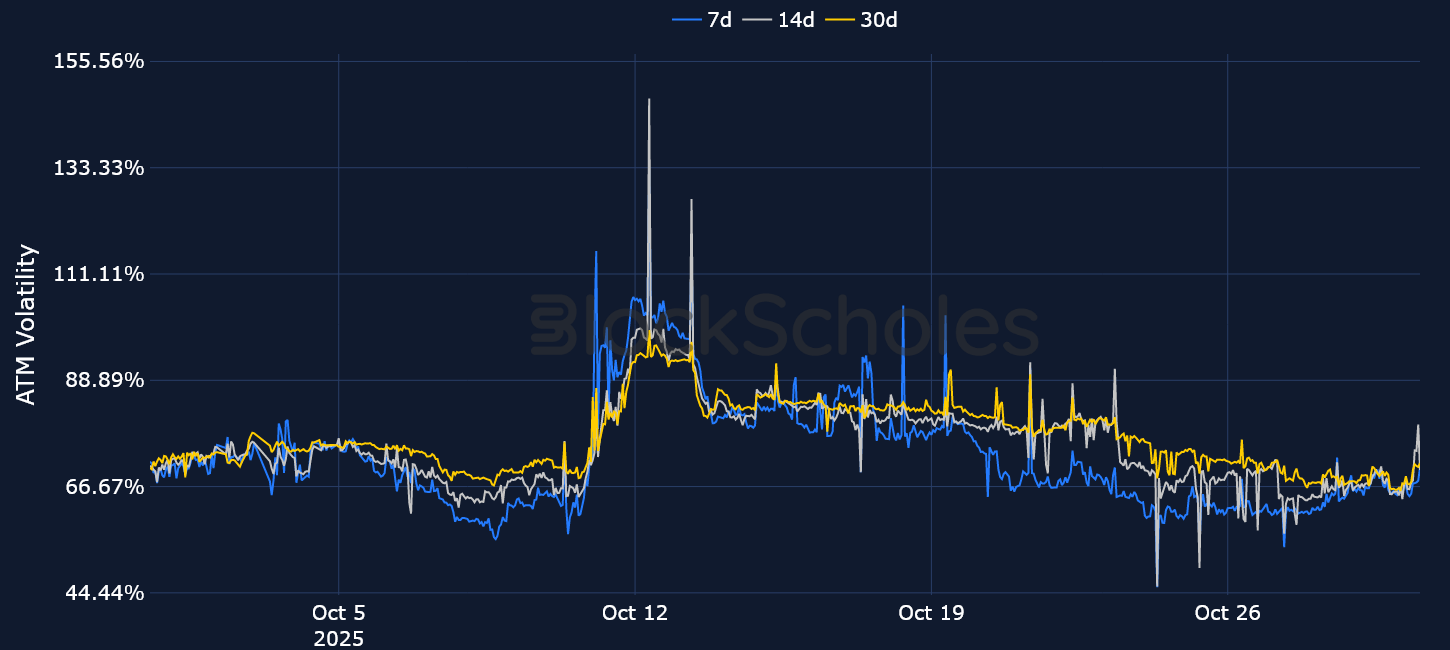

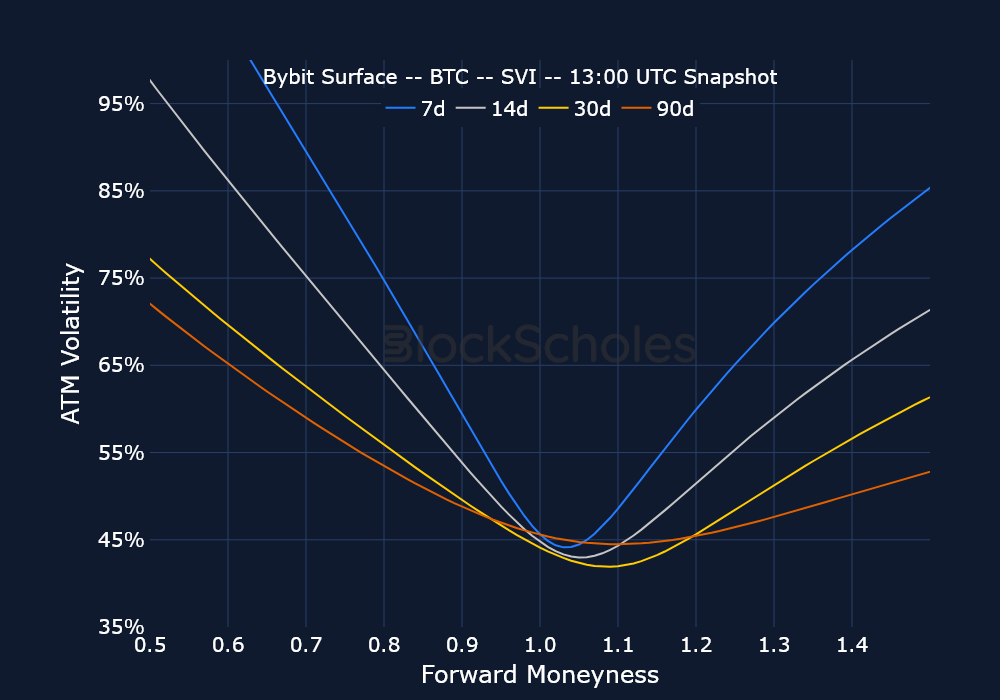

Open interest in BTC options isn’t showing the same deep deleveraging of positions that we’re observing in perpetual markets. In fact, open interest has actually steadily increased over the past month, albeit at a relatively slow pace. This suggests strong use of options contracts from Bybit traders in order to hedge their positions or speculate on future market moves. Indeed, at-the-money implied volatility for BTC options across the term structure remains elevated, relative to levels at the start of the month. This elevated volatility is noteworthy, given that two major macro events have passed without triggering a drop in forward-looking expectations: President Trump and President Xi signing a long awaited trade deal, and the FOMC meeting concluding with a 25 bps rate cut (though the likelihood of another cut this year is less certain). This indicates consistently higher demand for optionality following Oct 10, 2025, despite the low-volatility environment that BTC options have traded with over the past year.

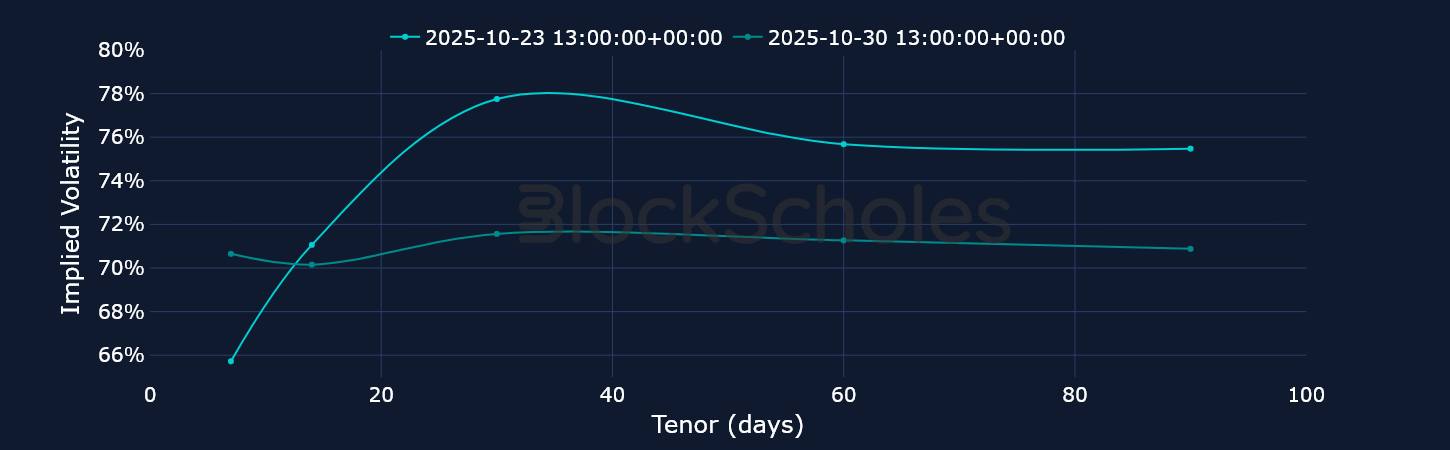

Meanwhile, BTC options traders still have the appetite to drive up the front end of the term structure and invert it in times of market stress. While the inversion hasn’t lasted long, it leaves in its wake a higher baseline level of volatility pricing that’s concentrated on put options.

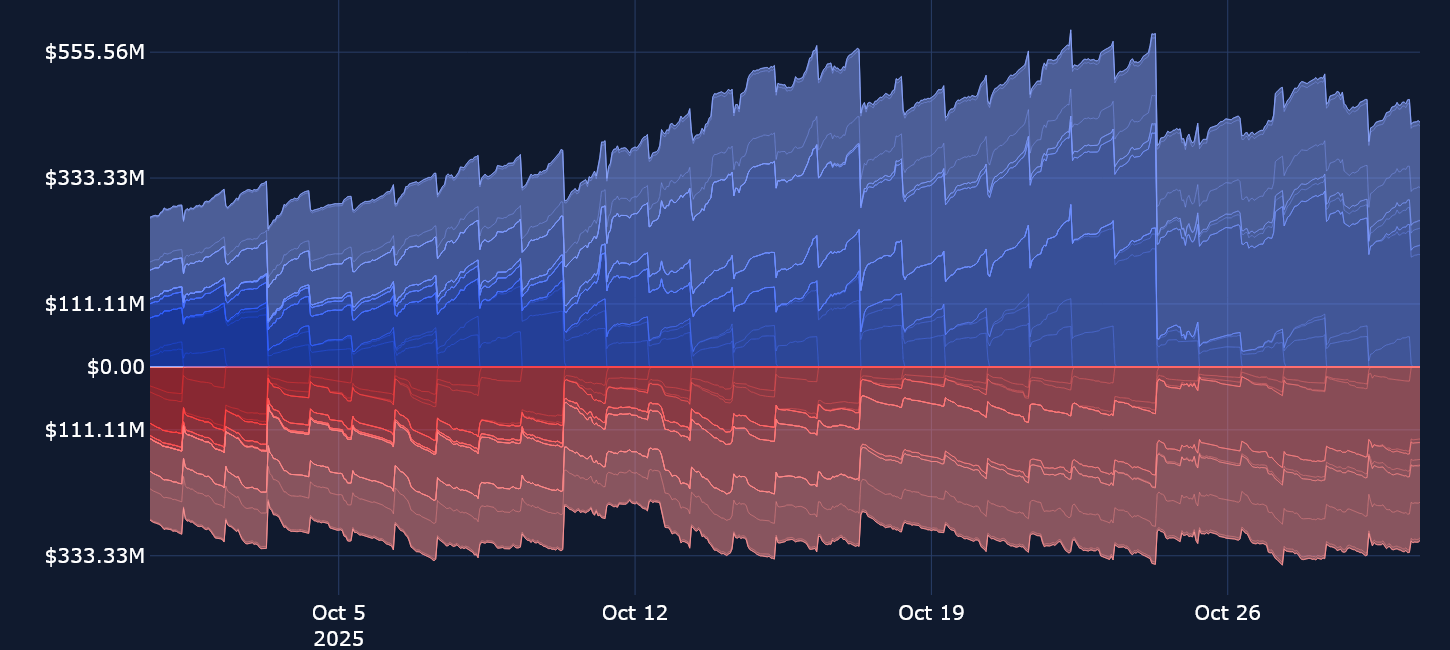

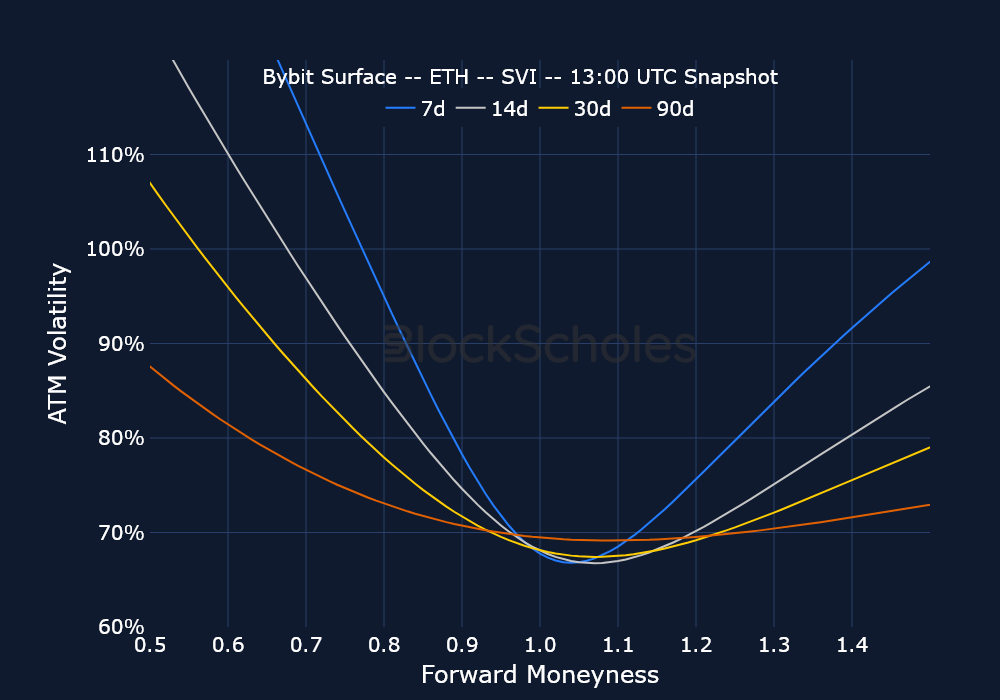

After two major inversions earlier in the month, short-tenor volatility has now dropped below that implied by longer-dated options contracts. Nonetheless, ATM implied volatility is still elevated, relative to the levels ETH options contracts traded at during the beginning of the month (similar to BTC). Interestingly, while realized volatility has fallen almost 50 volatility points over the past week, implied volatility hasn’t yet followed the same path. This suggests that options traders haven’t yet forgotten about the market moves on Oct 10, 2025 and are still willing to pay significant premiums for options contracts across all maturities of the curve.

As has been the case, ETH options continue to command a significant premium over BTC options at all points on the volatility surface. While the structural selling of volatility by BTC digital asset treasury companies is likely one cause of the months-long trend of declining volatility in BTC markets; this is still something we have yet to see from digital asset treasury companies (DATs) that hold Ether.

SOL’s realized and implied volatility are once more diverging after a temporary period of convergence. However, unlike earlier in the month, when realized volatility traded far higher than implied volatility, volatility implied by 30-day options is now trading at a 10 point premium to what’s been realized over the past week.

Additionally, among the three majors, SOL’s options market is the only one in which ATM implied volatility no longer remains elevated, relative to pre–Oct 10, 2025 levels. Prior to the liquidation cascade, options traders assigned a 67% premium to one-week SOL contracts — the same premium we see today. Meanwhile, SOL has yet to recover from the levels it fell from during the Oct 10, 2025 crash, and is down 3% over the past seven days.

With the ongoing US government shutdown, crypto assets have had few macroeconomic data releases to react to. So far, markets have only received a CPI report showing inflation in September a tenth of a percentage point lower than expected (for both headline and core inflation). This slight drop in inflation alongside a willingness to cool trade tensions between the US and China has helped drive some sentiment recovery in options markets.

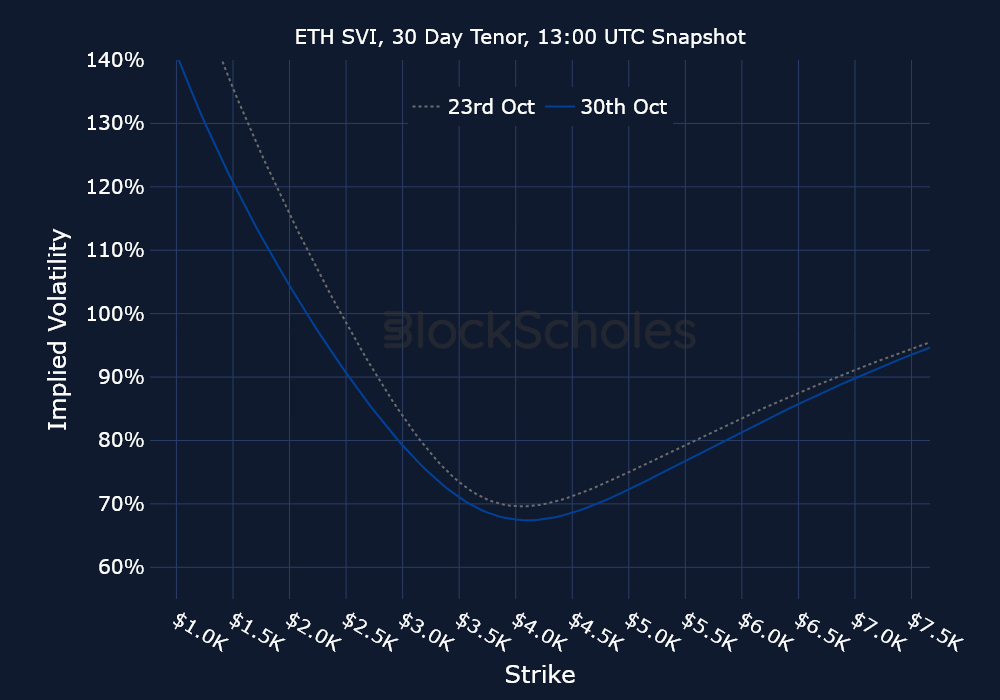

Unfortunately, that recovery has now flipped just as fast — despite delivering a rate cut at Wednesday’s Oct 29, 2025 FOMC meeting, Chair Powell said that a December rate cut (which markets had priced in with a 91% probability) was “not a forgone conclusion — far from it.” This has resulted in a major sentiment shift back to risk-off. Both BTC and ETH volatility smiles are now firmly skewed toward a bearish bias for puts, a significant reversal from the temporary skew toward calls that we saw earlier this week. An even more bearish picture is apparent when looking at ETH volatility smiles, indicating negative sentiment despite a trade deal signed on Oct 30, 2025 between Trump and Xi.

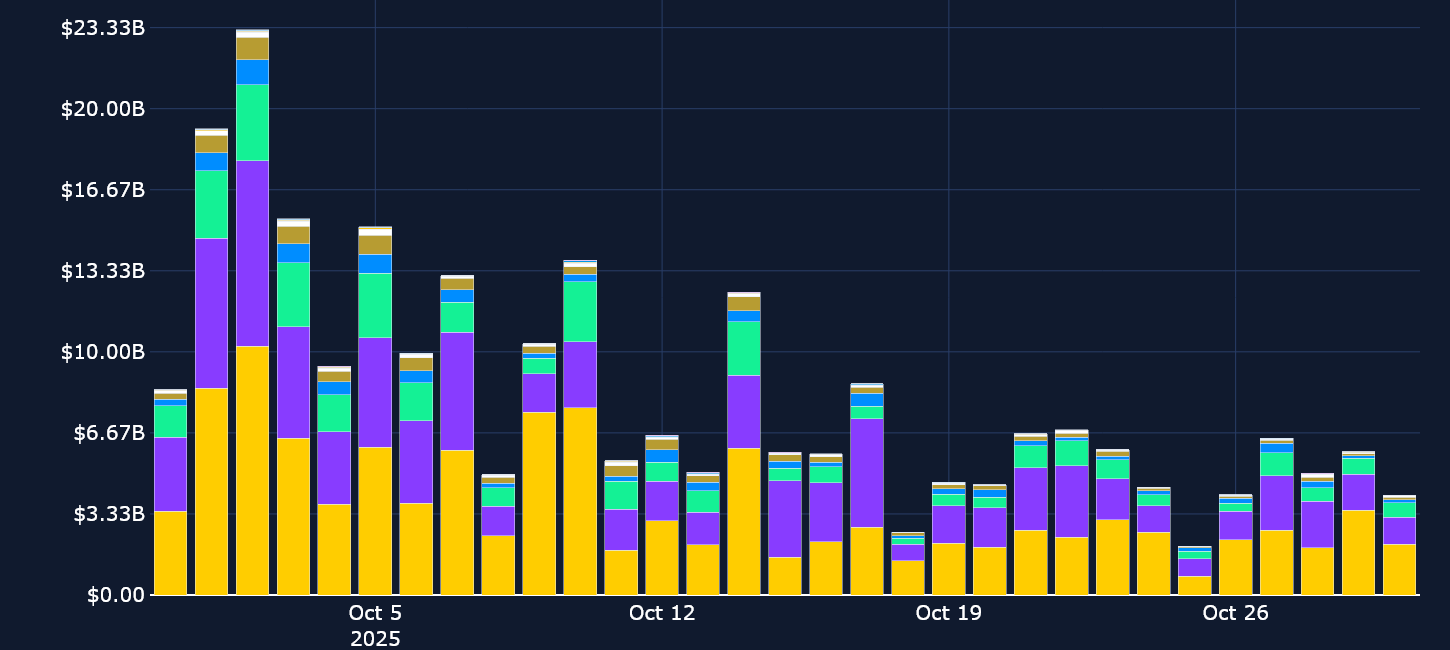

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)