Andrew Melville

Research Analyst

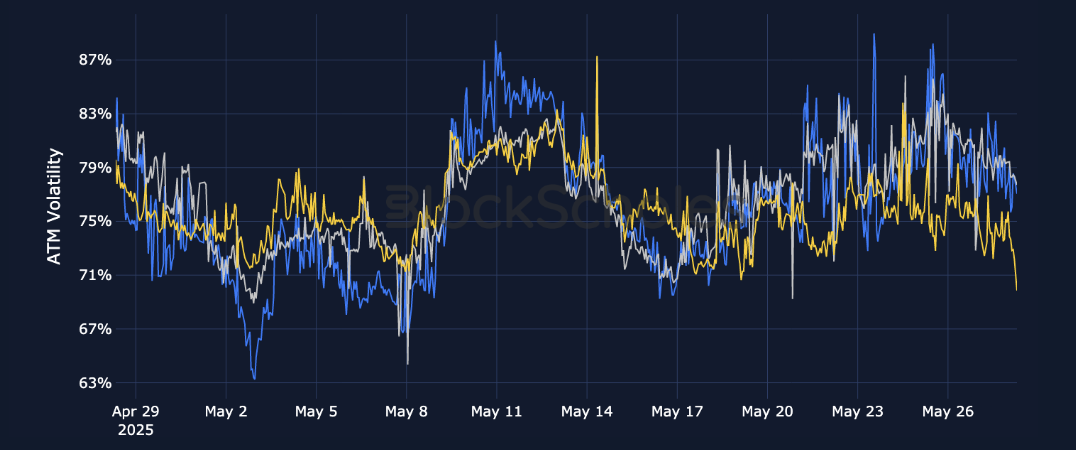

BTC’s march to a new all-time high on May 22, 2025 has been followed by a period notable largely for its lack of volatility. Realized volatility has fallen across cryptocurrencies, causing a corresponding drop in short-dated implied volatility. For ETH, that’s resulted in a flat term structure, while for BTC it’s caused a reasonably strong steepening as the 7-day tenor has fallen back below 40%. Options and futures markets have expressed bullish sentiment throughout the past week, with positive futures yields and funding rates and a skew toward OTM calls. However, a downturn in BTC’s spot price on May 28, 2025 has clouded the picture somewhat in funding rates.

BTC’s march to a new all-time high on May 22, 2025 has been followed by a period notable largely for its lack of volatility. Realized volatility has fallen across cryptocurrencies, causing a corresponding drop in short-dated implied volatility. For ETH, that’s resulted in a flat term structure, while for BTC it’s caused a reasonably strong steepening as the 7-day tenor has fallen back below 40%. Options and futures markets have expressed bullish sentiment throughout the past week, with positive futures yields and funding rates and a skew toward OTM calls. However, a downturn in BTC’s spot price on May 28, 2025 has clouded the picture somewhat in funding rates.

Perpetuals: Open interest remains at a strong high across tokens, despite the pullback from Bitcoin’s all-time high notched on May 22, 2025.

Options: A fall in realized volatility has caused a flattening in ETH’s term structure and a steepening in BTC’s as short-dated volatility expectations react. Volatility smiles for both tokens are bullishly skewed toward calls.

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

BTC’s May 22, 2025 all-time high of $111.97K led the entire crypto market higher. That was reflected in corresponding growth in the open interest of perpetual swaps, which saw growth supported by a wide base of tokens. This suggests that, as we’re used in crypto markets, much of the open interest in perpetuals has been opened by those seeking long exposure to the rally, a fact echoed by the persistently positive funding rates recorded for each of these tokens over the same period. BTC contracts continue to dominate the market, accounting for more than $6B of open interest alone. However, sideways spot price action since notching that most recent all-time high has left its mark on daily trade volumes, which have been more than half of the $26B high recorded on May 21, 2025, the day before the all-time high.

Since May 19, 2025 (the beginning of the rally toward BTC’s most recent all-time high), funding rates across all coins were positive, indicating a strong willingness to pay for leveraged long exposure to the rally. This wasn’t just seen in BTC’s perpetual swap markets, but across all tokens, as the entire market was lifted during the rally. That regime of nearly nonstop positive rates persisted until May 28, 2025, when BTC slid from $109K to $107K, and BTC funding rates turned negative for the first time since May 15, 2025. While the funding rates of other coins have moderated, they haven’t yet reflected the same flip to negative as BTC’s.

BTC’s most recent charge to an all-time high has been marked by a surprisingly low level of volatility, both realized in spot returns and implied by options prices. Short-dated volatility expectations have collapsed once more, strongly steepening a term structure that had already refused to invert to the same degree as ETH’s, despite BTC spot pushing to new highs while ETH remains close to 40% below its $4.6K all-time high. Also in contrast with ETH’s markets, BTC put options have recorded higher daily trade volume (peaking at $250M on May 21, 2025) and higher open interest when measured relative to call options. However, while lower than that assigned to ETH’s upside, BTC’s options markets continue to price OTM call options at a premium across the term structure.

BYBIT BTC OPTIONS OPEN INTEREST

After a catch-up rally of over 40% at the beginning of May, ETH has traded sideways in tandem with the rest of the crypto market. With that drop in realized volatility, the strong premium that options markets had previously assigned to short-dated optionality has dissipated, and the term structure of at-the-money implied volatility has returned to a far flatter shape, with implied volatility at all tenors trading lower within a tight 64–67% range.

Reflecting a similar phenomenon in perpetual swaps markets, daily trade volumes have been remarkably lower toward the end of the month in both bullish call options and bearish put options, with little change in the open interest of either contract.

SOL retreated quickly from the local high that it recorded on May 22, 2025 (at the time of BTC’s most recent all-time high), falling 10% to $169. Its options markets have priced in a lower level of volatility across the term structure in response to a fall in realized volatility, which had previously remained elevated since early May. However, the term structure of at-the-money implied volatility remains inverted, with short-dated options trading at an implied volatility premium to longer-dated options. This creates an unusually shaped implied volatility term structure curve, as it’s rare for short-term volatility expectations to remain elevated at the same time as a drop in volatility.

After a brief fall in short-tenor expectations toward bearish put/skewed volatility smiles for both BTC and ETH, outlooks have since recovered as BTC spot has traded mostly sideways just below its all-time-high. Each tenor’s BTC smile is skewed between 2–3% in favor of calls, with a stronger tilt at the 7-day tenor. Meanwhile, ETH options have shown a more decisive recovery in expectations following the initial rally, with volatility smiles at all tenors shorter than 90 days now reporting a 4% premium of 25-delta out-the-money calls relative to 25-delta out-the-money puts. Both markets reflect similar bullish sentiment in perpetual swap funding rates as well as futures-implied yields, indicating that traders are willing to pay a premium to bet on continued bullish momentum

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)