Andrew Melville

Research Analyst

After initially holding firm following US president Donald Trump’s “Liberation Day” tariffs, crypto joined the global market sell-off as BTC dropped from $87K on Apr 2, 2025, down to a local bottom of $74K. Its term structure once again inverted before slightly abating, as we’ve often seen it do, and ETH’s term structure has remained at an already inverted state. Short-tenor BTC volatility smile skews reached a bias toward OTM puts, reflecting even more bearish sentiment than during the turmoil of the US banking crisis in Q1 2023. These levels of volatility have since dropped off, as Trump announced yet another pause on his tariff plan. This time, the reciprocal tariffs have been temporarily paused for 90 days (except for those on China), which has resulted in a dramatic spot price rally.

After initially holding firm following US president Donald Trump’s “Liberation Day” tariffs, crypto joined the global market sell-off as BTC dropped from $87K on Apr 2, 2025, down to a local bottom of $74K. Its term structure once again inverted before slightly abating, as we’ve often seen it do, and ETH’s term structure has remained at an already inverted state. Short-tenor BTC volatility smile skews reached a bias toward OTM puts, reflecting even more bearish sentiment than during the turmoil of the US banking crisis in Q1 2023. These levels of volatility have since dropped off, as Trump announced yet another pause on his tariff plan. This time, the reciprocal tariffs have been temporarily paused for 90 days (except for those on China), which has resulted in a dramatic spot price rally.

Perpetuals: Funding rates for BTC briefly turned negative at the start of the spot sell-off, before returning to a more neutral level, and have since remained close to 0%, with ETH funding rates showing a similar story.

Options: Implied volatility levels have once again exploded to the upside for BTC and ETH as Trump announced his “reciprocal tariffs” program, but have since relented slightly.

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

US Treasuries yield curve — Over the past week, long-end maturities across US Treasuries have jumped by over 20 bps amid strong sell pressure. In comparison, shorter maturities have risen by a smaller amount, resulting in a steeper yield curve.

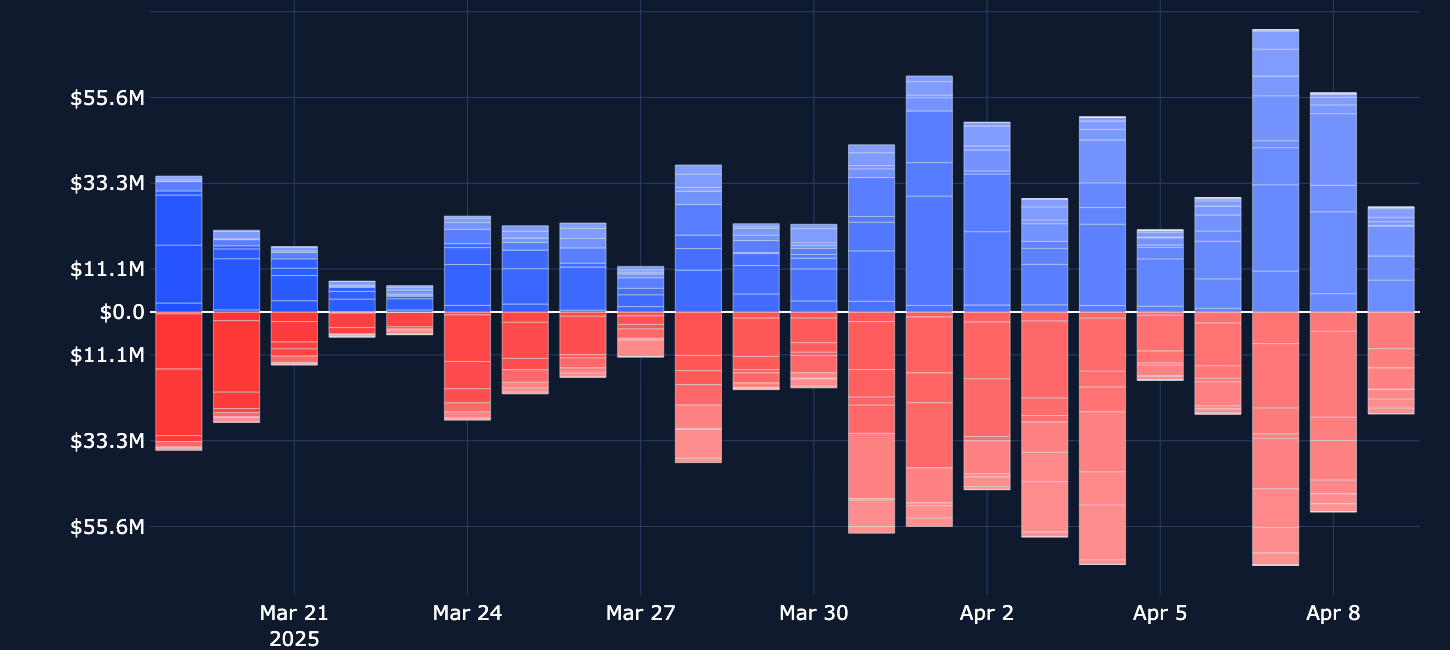

Activity in Bybit’s largest perpetual swap markets had previously remained firm throughout the broader market sell-off and reaction to tariffs, first holding and then building upon the level that it had dropped to after the Bybit hack in late February 2025. However, Trump’s most recent announcement, escalation and pausing of near-unilateral import tariffs has weighed strongly on markets, including perpetual swap trading. BTC and ETH lead the largest losses in open interest and are several steps down from their late March highs.

After a brief run of positive funding rates, BTC’s perpetual swap market was once again fluctuating between positive and negative sentiment. This suggests that, just like last week, traders were seemingly unwilling to price in a directional move with strong conviction, reflecting what we’ve observed in options markets positioning. That trend may have been reversed as President Trump announced a 90-day tariff relief, and funding rates have moved to print positive jumps. Across altcoins, we see much the same story as with BTC: funding rates varying from positive to negative through the week before posting an upward jump on new tariff news.

The sell-off from Apr 6–7, 2025 saw traders rush to protect themselves against further downside moves as BTC’s spot price dropped to $75K, following a delayed market response to President Trump’s latest tariff announcement. The volume in put options relative to calls supports the picture of demand for downside protection. Meanwhile, the US’s reciprocal tariffs have led to a significant inversion in BTC’s term structure of at-the-money volatility, which (while it has since abated) remains inverted. That inversion was also met with an even stronger skew toward OTM puts at short tenors than during the US banking crisis in March 2023. Finally, put open interest has increased significantly over the week in an extreme expression of bearish sentiment for both the near- and long-term.

Options volume and open interest have both shown near equal activity in calls and puts, as realized volatility and implied volatility have both jumped over the past week, while traders have reacted to the realization that Trump’s reciprocal tariffs were more than a move to extract concessions from the US’s trade partners. Short-tenor volatility imploded as ETH’s spot price crashed: the token is trading 20% down this week alone, with the ETH/BTC pair reaching its lowest level in over five years. After realized volatility cratered in late March to trade below implied levels, it’s now once again trading above the levels implied by 30-day tenor options.

Trade volumes in Solana call options jumped significantly on Apr 7, 2025, as the token traded below $100 for the first time since February 2024. After SOL’s price dropped, open interest in both calls and puts first spiked before falling off slightly. That increased trade volume was otherwise an anomaly, as options volume subsequently reverted back to similar levels not seen since mid-March. Call options for Solana are still dominating both volume and open interest, with the gap between call open interest and put open interest over $1M in favor of open interest.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)