Thahbib Rahman

Research Analyst

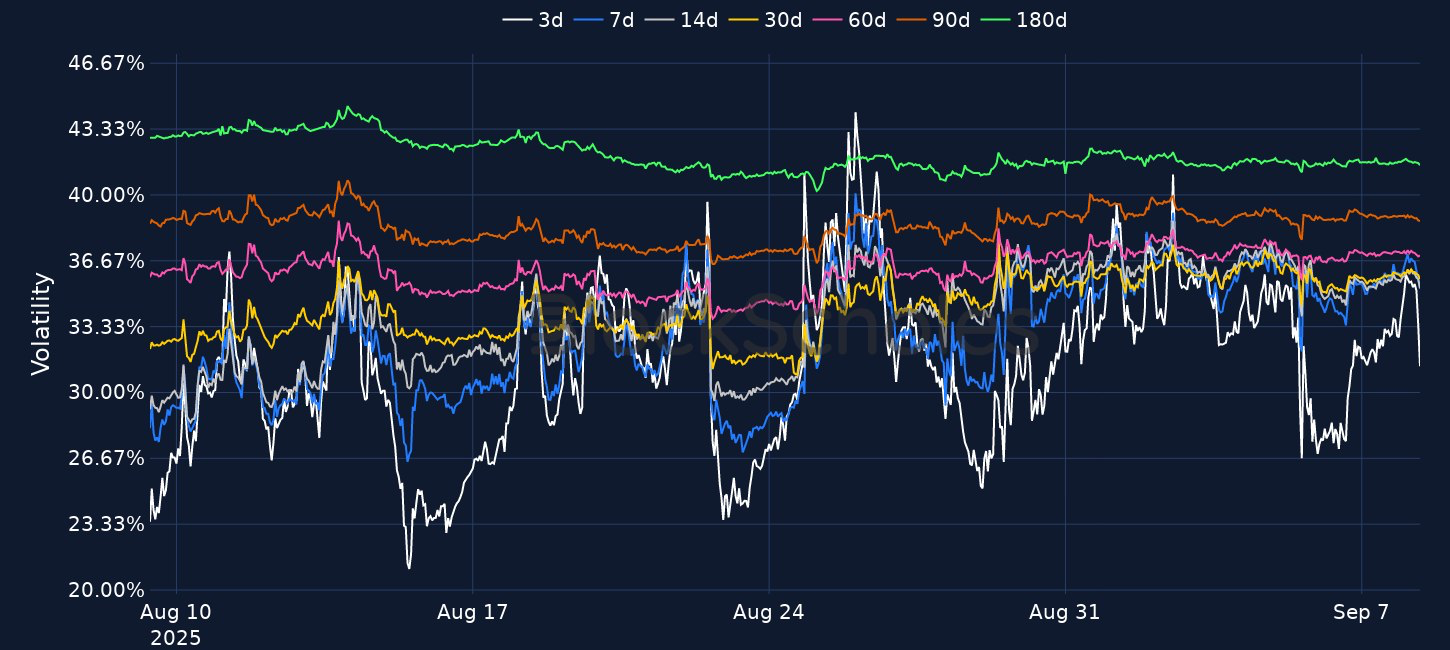

US job growth slowed sharply in August, with only 22,000 jobs added and June’s payrolls revised to a net loss of 13,000, the first month of negative jobs growth since Dec 2020. Prior to the release, markets had locked in the probability of a 25bps rate cut for the September FOMC meeting, however that distribution has now changed, with a 90.1% probability of a 25bps reduction to the FFR, and a 9.9% chance of an outsized 50bps cut. BTC has mostly continued to trade within $109K and $113K over the past week. That sideways spot price action has seen a similar sideways trading in ATM implied volatility levels. 7-day BTC options trade with an IV of 35.8%, largely unchanged over the past 24 hours.