Thahbib Rahman

Research Analyst

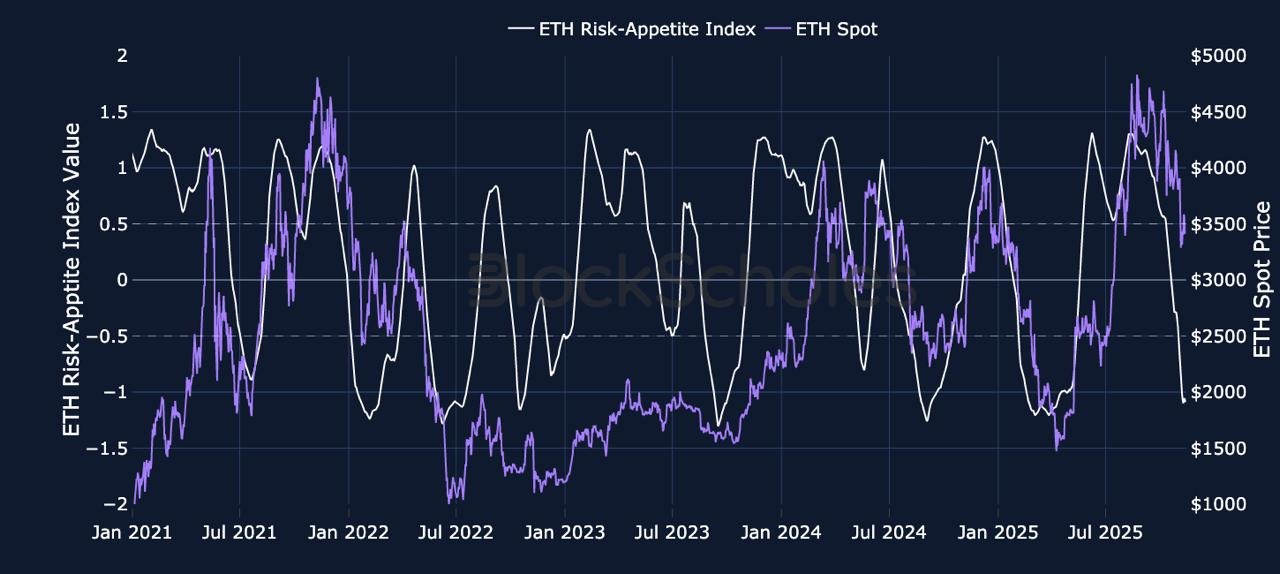

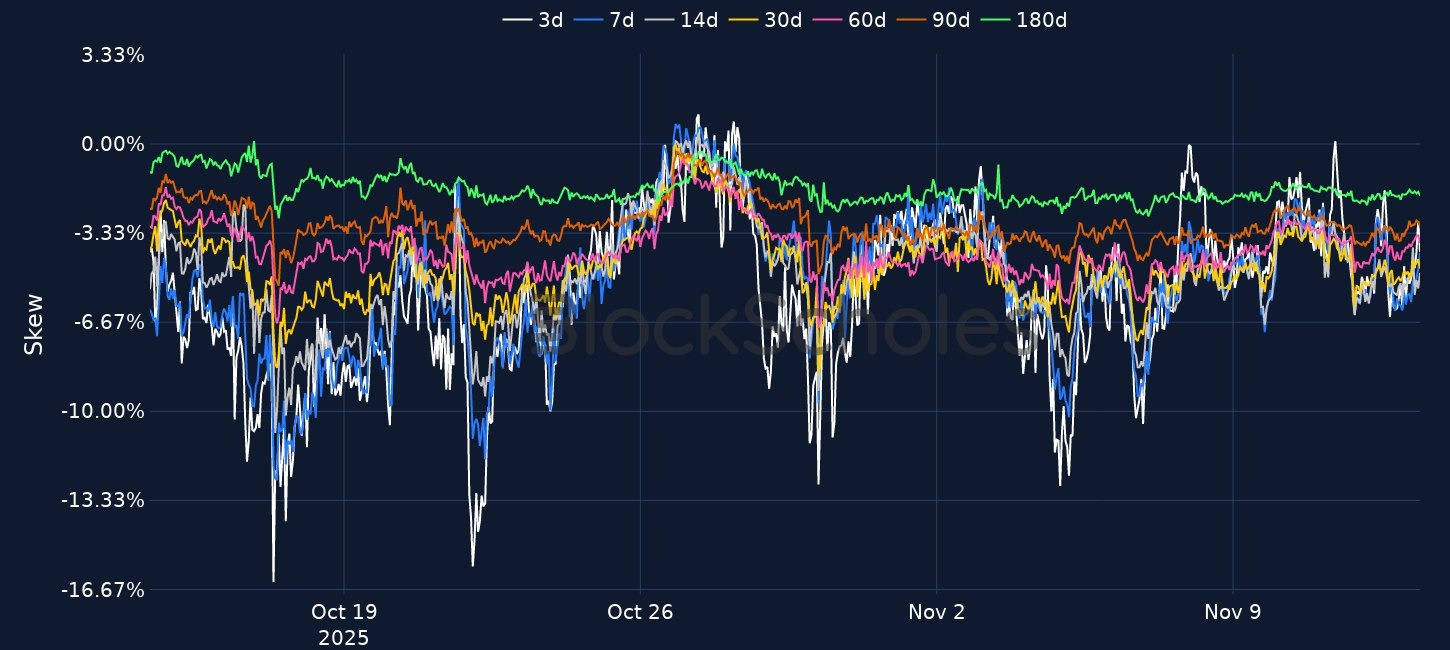

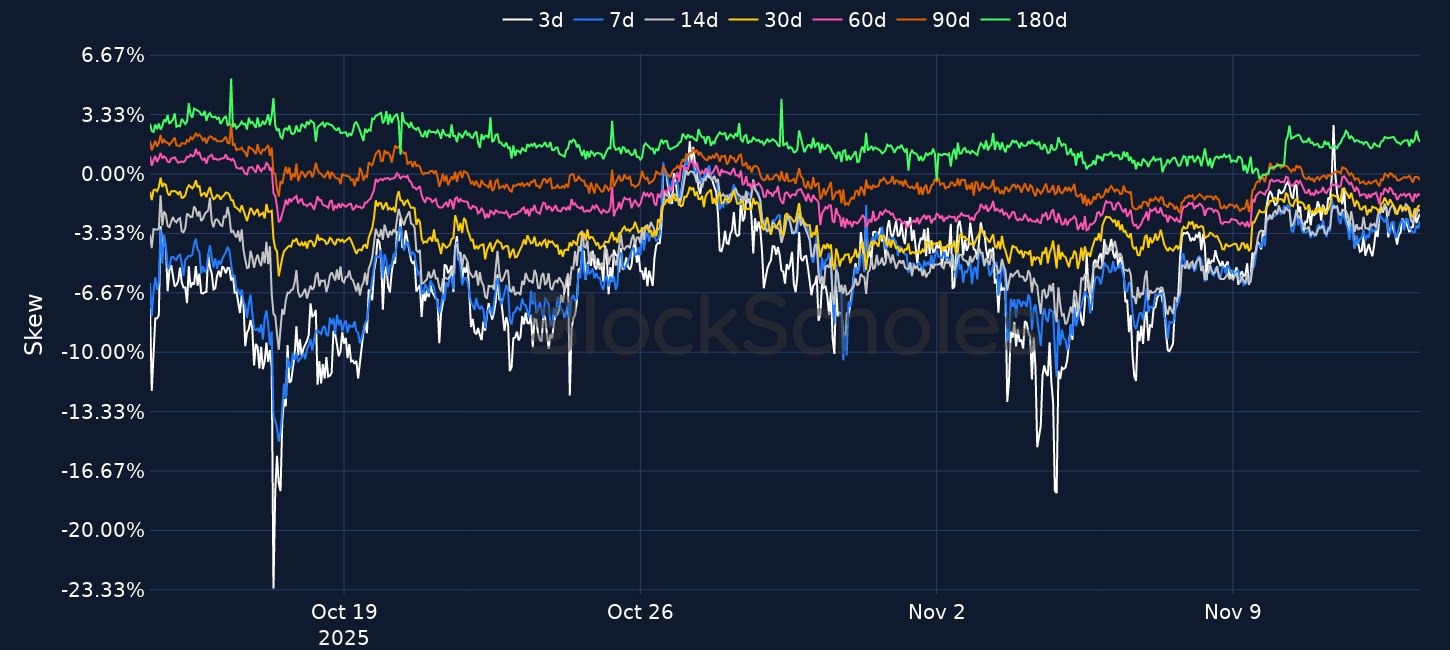

BTC has retraced to ~$102k from >$107k, with derivatives and ETF flows signalling weak dip-buying: short-tenor futures are below spot, option skews are put-heavy, and spot ETFs have offloaded ~$71m of BTC since 29 Oct. US risk assets diverged, with the S&P 500 up 0.93% and UST yields lower after an interim funding bill ended the 43-day government shutdown but left October NFP and CPI data likely permanently missing. Fed communication remains hawkish-leaning despite the data vacuum, with key officials stressing inflation risks, limited room for further cuts and a high bar for additional easing absent a clear labour-market deterioration. Structurally, tokenisation and digital-asset rails continue to advance via the SEC’s proposed “token taxonomy”, MAS’s tokenised bill pilot, Franklin Templeton’s Benji expansion, CME/FanDuel’s prediction app and Sui’s new USDsui stablecoin.