Thahbib Rahman

Research Analyst

Digital asset treasury (DAT) companies have dominated crypto-asset narratives throughout 2025. In this report we aim to highlight a far less discussed implication of DATs – the structural selling of optionality (and volatility) by DAT’s and the potential impact this may be having on both realized and implied BTC volatility at a time where BTC is already in a regime of historically low volatility.

Digital asset treasury (DAT) companies — firms that issue corporate debt to load crypto-asset purchases onto their balance sheets – have dominated crypto-asset narratives throughout 2025. DATs stockpiling Ether now hold more than $22B worth of the asset (4.5% of ETH supply), while public companies collectively hold 4.6% of BTC’s total 21M supply. However, far less has been discussed about the structural selling of optionality (and volatility) by DAT’s and the potential impact this may be having on both realized and implied BTC volatility – at a time where BTC is already in a regime of historically low volatility.

In this report we aim to highlight how DAT’s are likely contributing to the low volatility environment, and use the case study of one digital asset treasury that has already begun this process to examine the likely size of their activity in options markets.

Over the past year, Bitcoin’s delivered volatility has been close to the lower end of its historic range. Prior to 2025, delivered volatility rarely fell below 30% across any length of lookback window. In 2025, this has become a far more regular occurrence, with 7-day delivered vol even dropping to an extreme low of 20% following the September FOMC meeting.

This low volatility environment is not uniform across crypto-assets. As seen in the figure below, BTC’s delivered volatility has fallen relative to other major altcoins (such as ETH and SOL) over the course of the year (largely a result of low BTC vol, and higher/ increasing altcoin vol). That picked up significantly in early May, during a period of spot price outperformance by altcoins.

The low levels of BTC delivered volatility have also caused the volatility implied by at-the-money BTC options to drop significantly too. In fact, as seen by the linear regression below, options markets have recently been implying an even lower level of IV than we would expect given the current level of delivered vol.

While at least part of the impact can be explained by stickier, institutional buyers now driving more of Bitcoin’s price action (especially since the launch of easy-to-access ETFs in Jan 2024), the “extra-curricular” activities of DATs in derivatives markets is likely exacerbating the effect on BTC’s volatility – both implied and delivered.

According to a filing dated Oct 3, 2024, the (now) fourth largest BTC DAT by bitcoin stockpile, Metaplanet, sold 223 ATM BTC put options, expiring three months later on 27DEC24. That earned the hotel-operator turned Bitcoin accumulator a premium of 23.972 BTC.

The logic behind the transaction was simple: by selling cash-secured put options, Metaplanet could potentially cheapen its entry to buying Bitcoin. If BTC’s spot price expired below the strike price at expiration, Metaplanet would buy BTC at the strike and accumulate more BTC as intended at a price discounted from the strike price by the collection of option premia. If the puts expired OTM, the premium earned from selling those puts would also be put towards BTC purchases.

A separate filing showed that a week later on Oct 16, 2024, Metaplanet rolled over those 223 put options to a higher strike price ($66K) – assuming that they were held to expiration, these options expired OTM to Metaplanet’s benefit.

The disclosed details of the put contracts that were sold in the Oct 3, 2024 filing (shown above), includes

We used this information to calculate the fair (market implied-mid) premium of that transaction using our own calibrated volatility surfaces. This yielded a fair premium of the transaction of closer to $1.5M, compared to the ~$1.47M implied by the filing. We therefore estimate that Metaplanet took an approximate 3% haircut on the fair mid premium on the put options sold in Q4 2024.

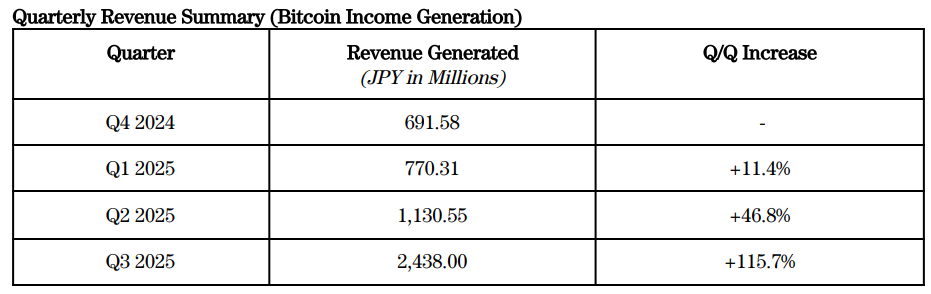

While the initial notional position started off small, Metaplanet quickly scaled up their activity. A later filing of the company’s revenue for their so-called “Bitcoin Income Generation” business stated that it earned 770,351,229 yen from put selling in Q1 2025, disclosing their notional as 645.74 BTC of put contracts (which expired ITM and resulted in the exercise of the options against Metaplanet), while removing information on the strike, and expiration of the contracts.

In their Q2 2025 filing, however, Metaplanet chose to omit further details of their options activity, stating:

“All transactions executed under this program are fully collateralized with cash and structured to protect capital while enabling opportunistic acquisition of Bitcoin. Execution details, including pricing and contract structure, are intentionally not disclosed to preserve the proprietary nature of the strategy.”

Instead, the filing discloses only the total revenue earned from this activity during the quarter. To estimate the notional of the remaining filings, we make the following assumptions (consistent with the full disclosure in the Q4 2024 filing) to calculate the premium per contract and divide the total revenue to estimate the number of put options sold.

Using those assumptions and the details listed in Metaplanet’s Q2 2025 filing, we estimate that Metaplanet sold (roughly) 1,021 BTC put options in Q2 (note Metaplanet later announced a small adjustment to their Q2 revenue, which we exclude from our calculations).

The same assumptions applied to Metaplanet’s Q3 2025 disclosure of 2,438M JPY revenue generated implies a put notional of (around) 2,228 BTC. Therefore, we estimate that between Oct 2024 and Q3 2025, Metaplanet sold around close to 4,100 BTC put options between Oct 3, 2024 and Oct 1, 2025.

Given that the total open interest of BTC options on Deribit and the open interest of IBIT BTC options are both $40B each, the selling of volatility from Metaplanet alone is likely not enough to explain the structurally lower volatility regime we see in BTC. Daily volumes in month-end expiration BTC options on Deribit alone is routinely above 10,000 BTC in notional, dwarfing the ~4,100 BTC notional traded by Metaplanet over the last year.

However, despite their relatively small notional size (relative to daily volumes), Metaplanet are unlikely to be the only DAT already active in the derivatives market. Metaplanet’s publicly disclosed derivatives market activity is a proof of concept to the idea that DATs can acquire BTC at a rate lower than spot by selling vol and cheapening their entry. It’s also likely that other DATs are not restricting their options selling to puts (to acquire BTC at a discount to prevailing market prices). Unlike ETH and other PoS cryptocurrencies, BTC does not generate any yield, and so day-to-day DAT business operations must be funded somehow.

For that reason, we extrapolate Metaplanet’s actions to the rest of the DAT market and in this section we aim to discuss what could happen if the 20 largest DATs and corporate holders of Bitcoin have already (or may soon) adopt similar strategies.

Firstly, we calculate the ratio of the notional size of put options sold by Metaplanet relative to their total BTC holdings (13.72%). We then consider three cases of the impact on the market if the top 20 corporate holders begin to sell put options at the same ratio as Metaplanet, a lower estimate where that ratio is a smaller 5%, and a larger estimate where the ratio is 20%. Note that a more accurate estimate of the likely incoming activity of DATs in options markets would repeat this analysis using the proportion of $ capital raised to be allocated towards derivatives acquisitions (for Metaplanet this value is 20.412B JPY, 10% of the 204.123B JPY raised).

Given the vast disparity of the BTC held by Strategy relative to all other holders (Strategy holds 12x more Bitcoin than the next largest holder, Marathon), we include a binary variable of whether Michael Saylor’s Strategy also deploys its 640,000 chest of bitcoins to such an activity (with no such activity found by us among MSTR filings).

The result is that, depending on the pickup in activity of corporations replicating such a strategy, there could be an annual supply of notional BTC options between 15.6K –190K BTC, which then could contribute to a far larger dent in the market.

According to Metaplanet’s October filings, the sale of the put options was facilitated by QCP Capital — a crypto-native market maker. Market makers have two choices with the options that they purchase from DATs selling volatility, both of which are made more attractive due to the fact they purchased these puts at an (estimated) 3% discount to mid-price:

If hedging the delta dynamically until expiration, market makers will take the bet that realized volatility will be higher than the volatility implied by the bid that they show to the DAT at entry. Assuming that Metaplanet’s October 3rd, 2024 filings are representative of the spread shown for block trades of this size, this is one potential option given that they are paying a slightly lower price relative to the fair market price.

Doing so has the effect of (likely in the margin, depending on the total notional size being hedged) suppressing delivered volatility. This is because the long-gamma position of the market maker requires them to sell in a rally and buy in a sell-off. Further, if delivered volatility is falling below implied volatility, market makers may over-hedge their positions (i.e. more frequently and in larger size), amplifying the impact of market makers' flow on spot markets. This effect is particularly strong at times where spot liquidity may already be drawing thin.

The other option for market makers is to pass the risk of the long options off by dumping the puts directly onto the market. In the ideal case, where the market maker is able to offload the entirety of the notional immediately without dropping the bid price for the options, they should be able to lock-in the 3% difference in premium. This has the effect of suppressing implied volatility as they increase the liquidity of volatility on the market and push prices downward. This effect is probably less marginal than the effect on delivered volatility due to the much smaller size of the options market relative to the spot market.

Metaplanet’s most recent Q3 filing disclosed their total revenue over the Q3 period from their ‘Bitcoin Income Generation’ strategy as 2,438M JPY, or close to $17M (assuming a JPYUSD rate of around 143.4 on Jul 1, 2025).

Using the same assumptions as we have in previous sections, we mark this option to the market and calculate its greeks in order to estimate the size of the spot trades required by a market maker in order to rebalance their delta and remain delta-hedged. Assuming a rebalancing every 3 hours, we approximate an average (absolute value) delta rebalance order size of close to $2.6M of BTC each 3 hour adjustment period.

If we conservatively assume 5% of the BTC held by the top 20 digital asset treasuries (excluding Strategy) are utilised in a similar put selling strategy as is being carried out by Metaplanet, we can scale our estimates of Metaplanet’s activity to calculate the capital deployed by market makers to the spot market if other major DATs followed suit. In our bear case in the previous section, the annual notional size of puts sold amounted to 15,670. Scaling this gives us a factor of 6.87 (15,670 / Metaplanet’s approximate 2,228 notional of puts sold). That results in an order size of $17.86M BTC every 3 hours in order to hedge the long gamma position. Equivalently, that approximates to $71.44M per day, or 0.1% of BTC’s total spot trading volume ($66B).

Focusing on Metaplanet’s market maker in particular, we estimate that they would have likely have lost out by rebalancing their delta dynamically, even given the assumed 3% discount they paid for buying the put options. The market maker paid approximately $17M in premia relative to a $19M fair price, but would have collected just $13.78M from the gamma scalping process during the hedging process (estimated from our own options pricer greeks over the lifetime of the option, assuming no frictional costs). That was largely a result of the fact that the implied volatility on the options paid, even that implied by the discounted premium, was higher than the delivered volatility over the period.

BTC has been in a low environment of realized volatility throughout the last 18 months. That volatility is not just low relative to BTC’s own distribution, but also when measured against the volatility delivered in large-cap altcoins. That has clearly had some impact on the levels of implied volatility (as markets will price for a lower level of realized volatility in the future), but we also note that the 30-day option-implied volatility trades below what we would expect from a regression against realized volatility.

The structural selling of volatility by digital asset treasuries is one factor contributing to this oversupply of volatility. While Metaplanet’s notional position sizes are not yet large enough to cause the low vol environment alone, they are a clear proof of concept that DATs can (and likely do already) sell vol. While we are yet to find evidence in public filings from other DATs doing this currently, Metaplanet have quickly scaled their operations to a larger notional BTC size and it is likely that disclosures from other DATs will soon follow (either through disclosures of previous similar transactions, or announcements of new options market activities).

Market makers on the other side of the trade are also contributing in one of two ways: if delta-hedging, their long gamma position has a marginal effect on delivered vol, and/ or if selling puts directly back to the market, they are likely to be affecting implied volatility. What we are interested in going forward is exactly how many other BTC DATs are likely to follow suit, and what the impact will be on ETH’s spot and options markets should ETH DATs begin to partake in a similar activity.