Thahbib Rahman

Research Analyst

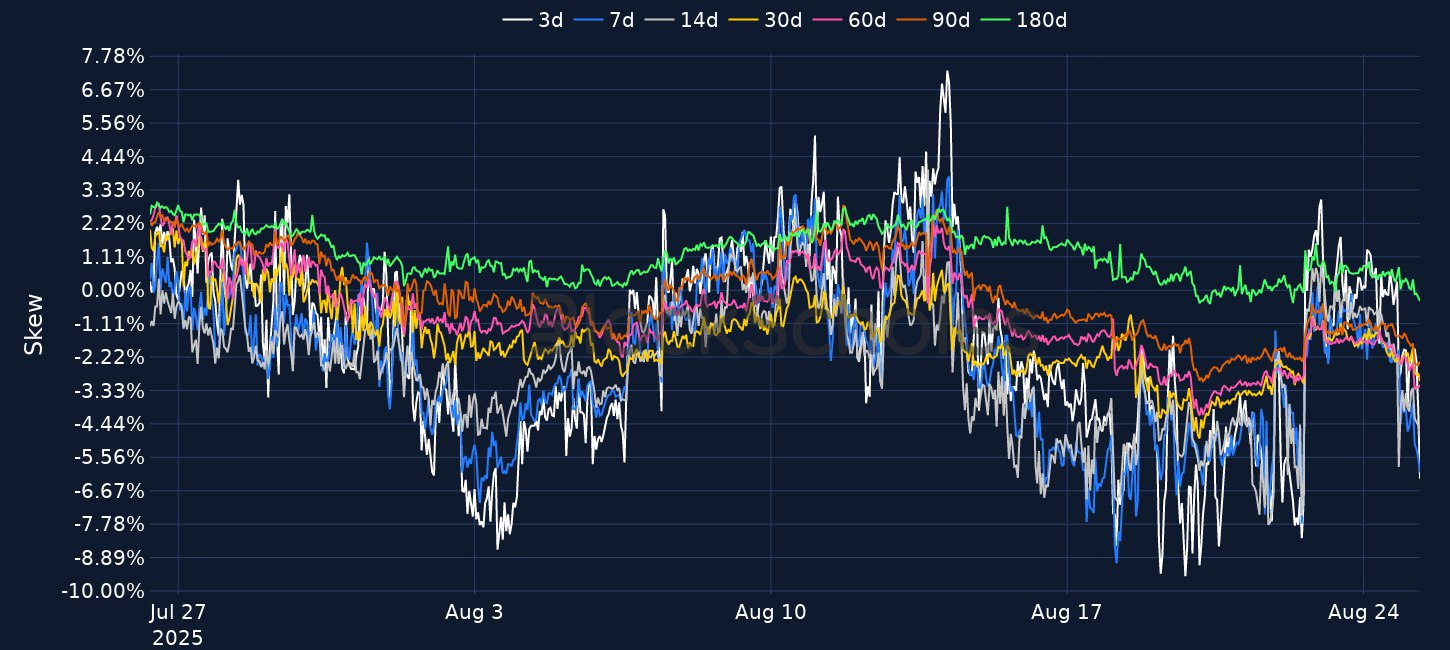

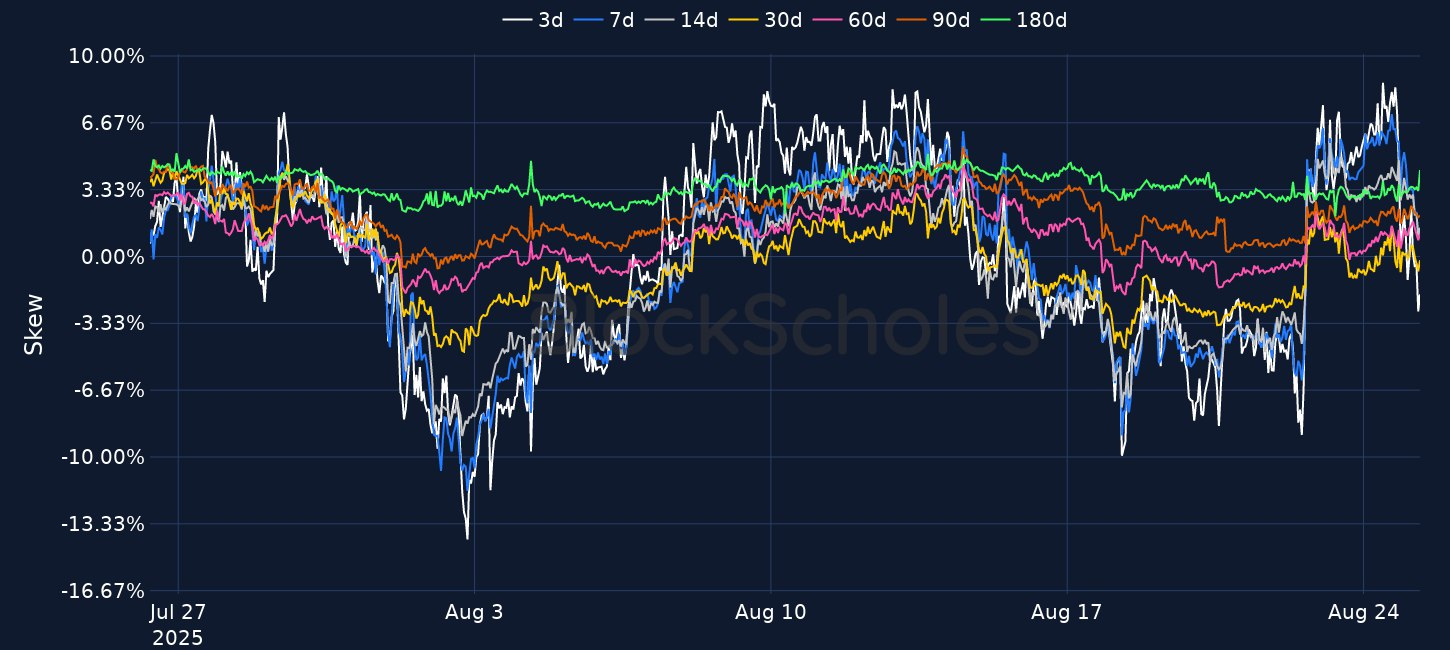

In the immediate aftermath of Jerome Powell's speech at the Jackson Hole Symposium, markets priced in a near certainty for a September rate cut. That came as Powell gave a surprisingly more dovish-than-expected hint that the time for an adjustment to the Fed's policy stance could be appropriate. In options markets, BTC volatility levels diverged from ETH as the former declined to below 30%, while ETH volatility held up at its higher 70% level. That divergence is apparent in put-call skew too. While skew is tilted towards OTM put options across the term structure for BTC, ETH skew remains positive at most tenors.