Thahbib Rahman

Research Analyst

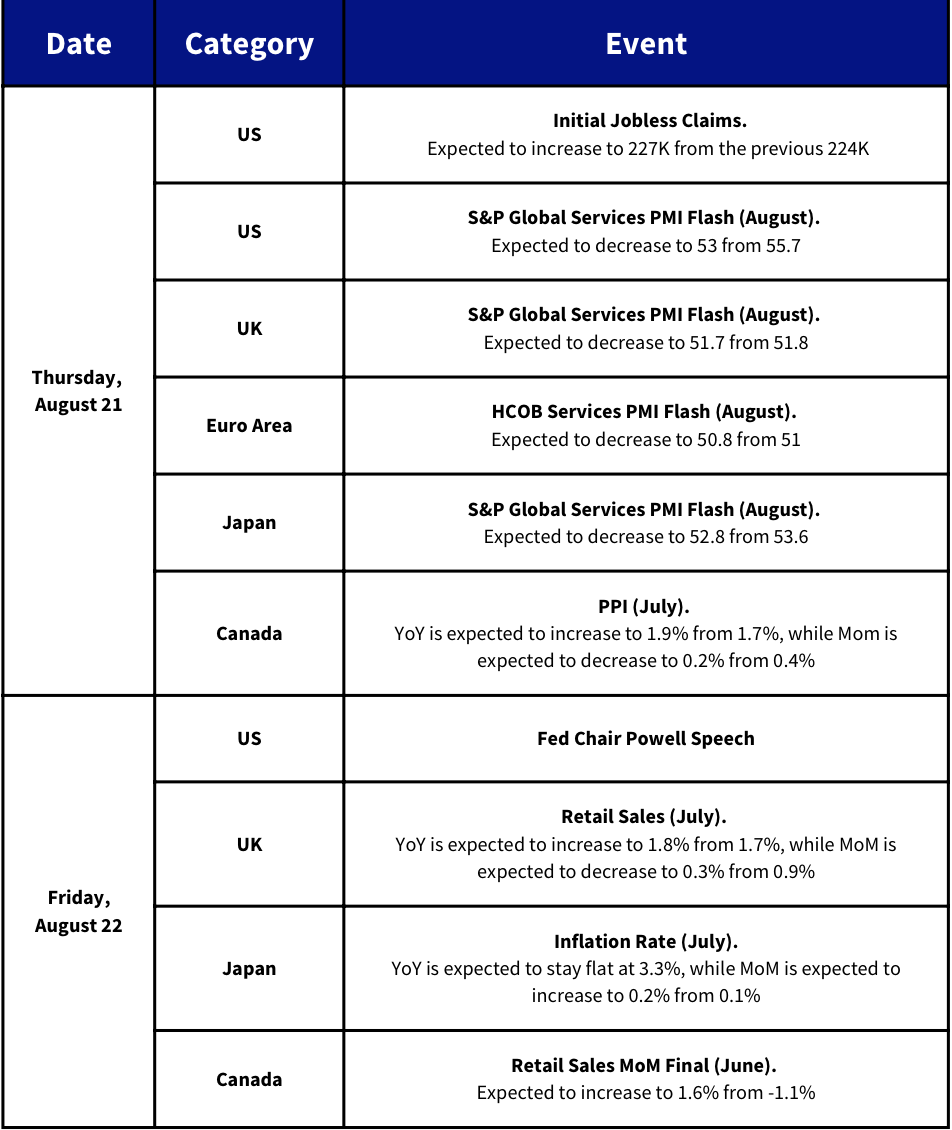

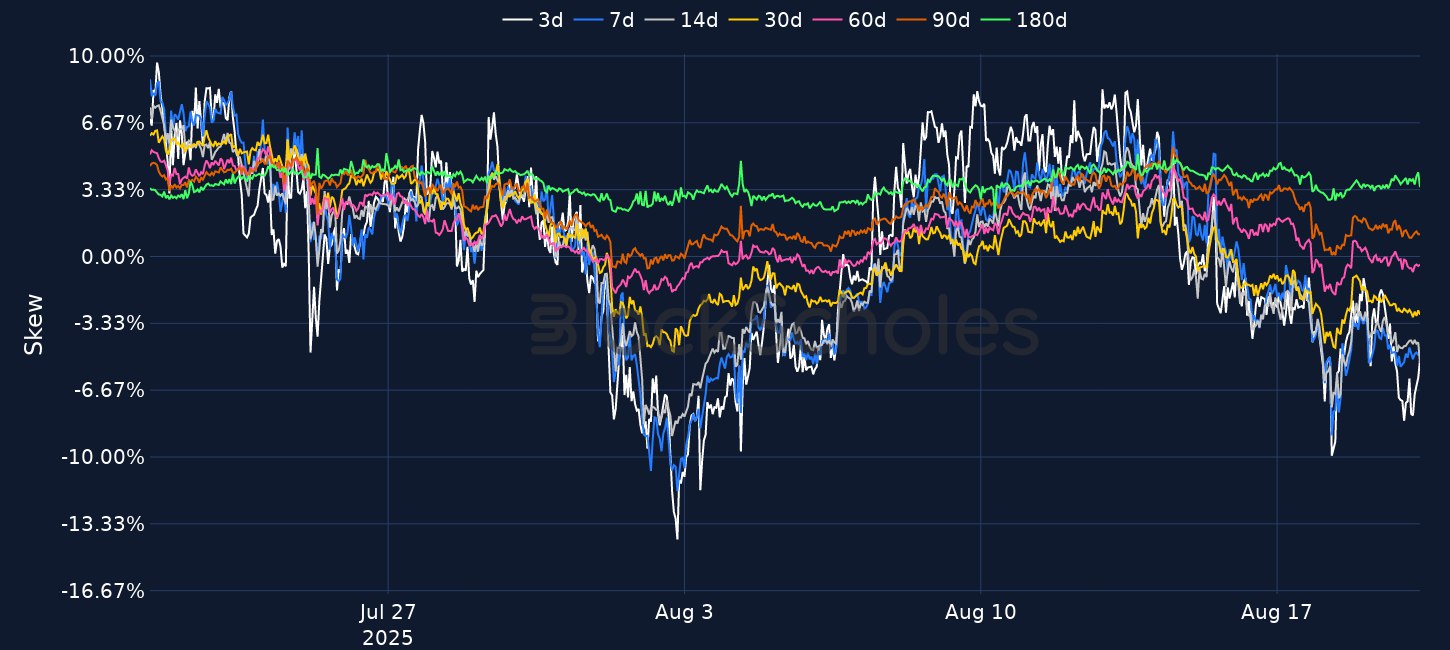

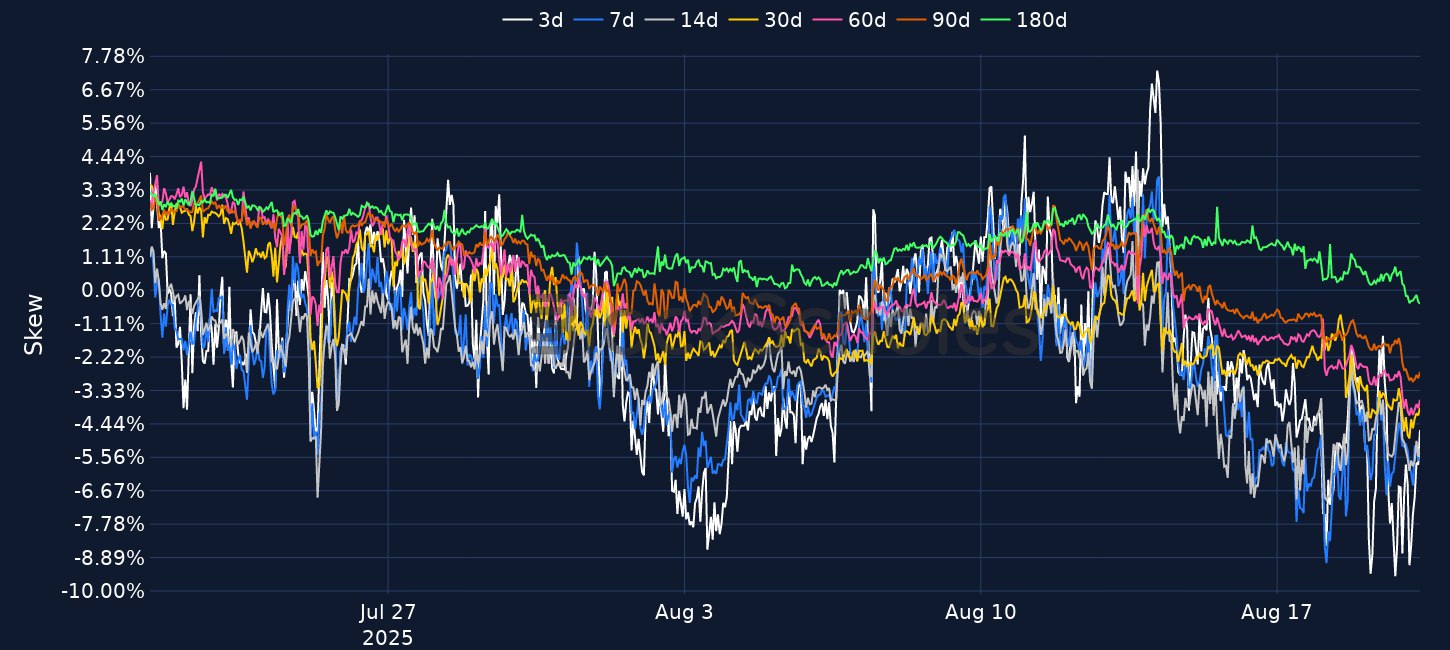

Cryptocurrencies continued their downward trend, with Bitcoin dipping to $112.6K and Ethereum falling 1% over 24 hours and 9% over the past week, reaching a local low of $4,060. The broader risk-off sentiment mirrored US equities, as the Nasdaq 100 fell 1.39% and the S&P 500 dropped 0.59%, ahead of Fed Chair Powell’s speech at Jackson Hole. Market expectations for a September rate cut have been revised sharply lower after a strong PPI report, with 30-day federal funds futures now pricing in an 82.9% probability of a 25bps cut, down from 98% last week. Spot ETF flows showed continued outflows, with BTC ETFs losing $523.3M and ETH ETFs $422.2M, highlighting investor caution. SEC Chair Paul Atkins signaled a potential regulatory shift, suggesting few crypto tokens should be treated as securities and emphasizing context over token type. Meanwhile, global inflation trends remained mixed, with UK inflation rising to 3.8% in July and Eurozone core inflation steady at 2.3%.