After sideways price action since Thursday afternoon, a late weekend rally in spot prices has pushed BTC close to $112K and ETH back above the $4,000 mark. Both majors Spot ETF products saw net outflows over the past week, while the share prices of DAT companies has slumped lower amidst the slowdown in spot prices. Implied vol levels have traded sideways through the weekend, despite the small rally, and vol smiles continue to remain towards OTM puts. For BTC, that skew progressively became more severe through the month post-FOMC as spot price continued to leak lower, however is beginning to show some signs of recovery. Resilient US economic data and an as-expected PCE inflation print helped US equities bounce back after a three-day slide.

After falling below $112K on Thursday afternoon last week, BTC traded sideways on Friday and the early half of the weekend. Since yesterday evening however, spot price has recovered slightly, now once more trading just below $112K.

ETH had seen a similar sideways movement after dipping below $4,000 on Thursday, before equally rallying yesterday to reclaim $4,100.

Last week, Spot BTC ETFs sold $897.6M bitcoins, ending a four-week inflow streak, with Fidelity’s FBTC fund leading the outflows on Friday. Spot Ethereum ETFs also had an entire week of negative flows, selling $795.8M worth of the token over the past five days.

The stock prices of Ethereum treasury companies have also plummeted recently in line with the decline in Ether. The largest holder of ETH, Bitmine Immersion Technologies, is down 13% in the last 5 days while Sharplink Gaming is down more than 10% over the past month.

The rally that began yesterday has pushed SOL back above $200, however the token has still pared back most of its gains following announcements of major purchases from digital asset treasury companies last month. Galaxy Digital, Multicoin Capital and Jump Crypto in late August announced plans to raise $1B to accumulate SOL tokens via Forward Industries, a Nasdaq-listed company, while in mid-September, Pantera Capital announced a $500M funding for Helius, another Solana backed treasury company. Together, these DATs now hold 3.64% of the token’s supply.

Similar to spot price, the implied volatility of BTC and ETH options traded sideways on Friday and the early weekend. However, unlike the late weekend bounce in spot price, implied vol has remained rangebound. For BTC, that means IV’s are trading between 31% and 41%, outperformed by the flatter term structure of ETH where vols are between 58% and 63%.

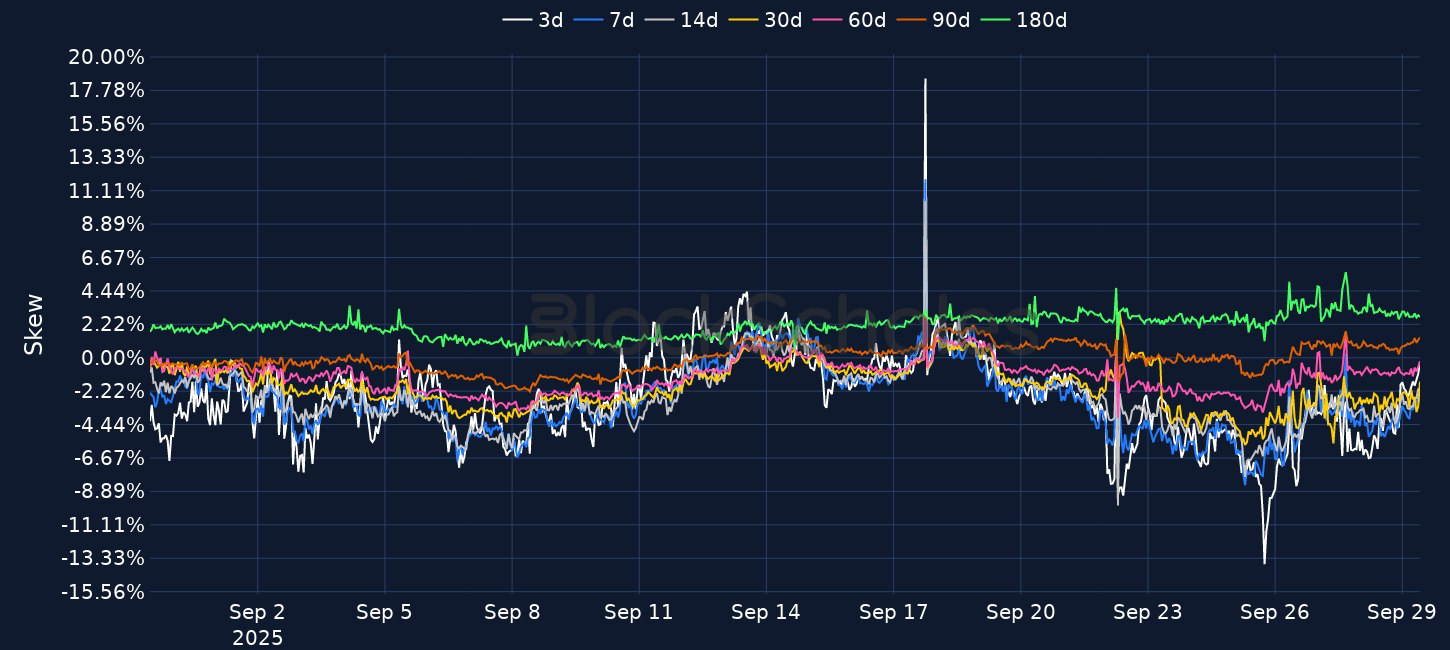

As has been the case for almost the entirety of the month, vol smiles remain skewed towards OTM puts for both majors. For BTC, that skew progressively became more severe through the month post-FOMC as spot price continued to leak lower, however it has shown signs of recovery late last week, though remains put-skewed.

US equities bounced in Friday’s trading session, with the S&P 500 finishing 0.6% higher, after a three-day slide. Despite the Friday recovery, all of the major US stock indexes ended the week lower. The move on Friday came following a PCE inflation report which matched expectations exactly — providing markets with a sigh of relief that the price stability side of the Fed’s dual mandate is still not spiraling higher.

The core personal consumption expenditures price index, PCE, rose 0.2% in August from a month ago, slightly lower than the 0.3% rise in July. That meant core PCE stayed flat at 2.9% on an annual basis, in line with expectations. Headline PCE year-over-year rose to 2.7%, following a rise to 2.6% in July.

The data also showed a resilient US consumer. Inflation adjusted personal consumer spending rose 0.4% for a second consecutive month. That follows data earlier in the week, including a revised Q2 GDP estimate of 3.8% (driven in part by strong consumer spending) and initial unemployment claims data that suggest the US labour market is still holding up.

After dipping to a five-month low on the date of the September FOMC meeting, following the strong GDP data, 10-year treasury yields rose towards 4.2% last week, marginally steepening the yield curve.

Interestingly, despite the resilient consumer spending, the University of Michigan’s Friday report showed consumer sentiment fell to a four-month low in September. According to the director of the survey, Joanne Hsu “Consumers continue to express frustration over the persistence of high prices, with 44% spontaneously mentioning that high prices are eroding their personal finances, the highest reading in a year”.

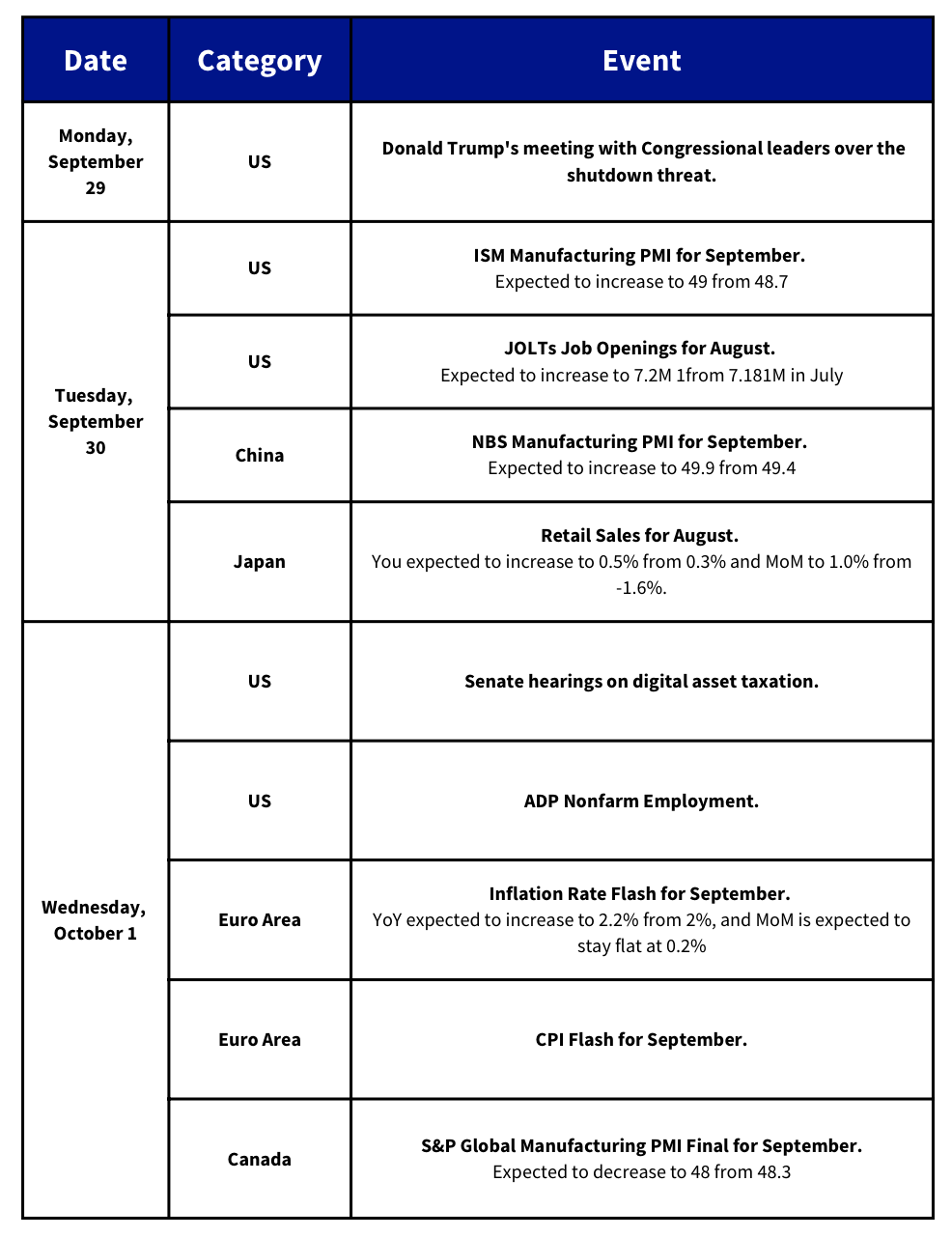

While the stronger than expected data meant traders slightly pared back some of their bets on an October rate cut at least temporarily (now implied-odds are back to 89%), looking ahead into the week, markets are awaiting a nonfarm payrolls report on Friday for further clues on the direction of monetary policy.

The US economy is expected to have added 50,000 jobs in September, above the revised three-month average of 30,000, while the unemployment rate is expected to have held at 4.3%. However, one potential complication is a federal government shutdown by Oct 1, 2025. The shutdown could delay the release of key government data, including the NFP report as well as a JOLTs report expected mid-week.

SWIFT plans to build a blockchain-based ledger that will allow financial institutions to settle tokenized assets and digital money more efficiently, according to Bloomberg.

The system is intended to connect fragmented blockchain networks with traditional payment rails, giving banks a common infrastructure for digital transactions.

Live trials are scheduled for 2025, covering areas such as cross-border payments, securities, and foreign exchange.

The initiative will initially focus on 24/7 cross-border payments. The design is based on a conceptual prototype developed with ConsenSys, with reports indicating experiments using ConsenSys’ Ethereum Layer 2 solution, Linea.

The company announced that it’s collaborating with more than 30 financial institutions to gather feedback on its upcoming blockchain-based ledger.

Participants include major global banks such as Banco Santander, Bank of America, BNP Paribas, and HSBC.

Decentralized perpetuals exchange Aster has surged to the top of DefiLlama’s data of Perp Volumes, generating over $25M in daily fees and recording $42B in 24-hour trading volume. The platform outpaced rivals including Hyperliquid, which earned $3.17M in fees and ranked fifth by comparison.

Aster has been gaining momentum since its token launch and receiving public backing from Binance co-founder Changpeng Zhao. Backed by YZi Labs (formerly Binance Labs).

The platform, formerly known as APX Finance, rebranded earlier this year after merging with Astherus and continues to lean on support from YZi Labs.

Crypto exchange Kraken is in talks to raise $200–300M from a strategic investor, according to Bloomberg. The funding, which is not yet finalized, could lift the company’s valuation to $20B and comes as Kraken prepares for an initial public offering planned for early 2026.

The report follows news from Fortune that Kraken recently completed a $500M round at a $15B valuation.

Crypto’s Wildcard:

We’ve consistently emphasised the point that BTC and crypto-assets have become intertwined with the macro space for some time. One interesting playful memecoin that sits at that exact intersection is SPX6900. For those in our readership who are unaware of this memecoin — it is an Ethereum-based token that critiques traditional finance through satire.

Launched in August 2023, SPX6900 is a parody of the S&P 500 index that we cover in our daily comment almost every day! The token’s catchphrase is that “6900 is a bigger number than 500”. Unlike some utility-driven memecoin projects, SPX6900’s value is derived from its meme virality. The token exploded from $0.001 in February 2024 to a high of $2.25 in July 2025, however it currently trades at $1.

After falling below $112K on Thursday afternoon last week, BTC traded sideways on Friday and the early half of the weekend. Since yesterday evening however, spot price has recovered slightly, now once more trading just below $112K.

ETH had seen a similar sideways movement after dipping below $4,000 on Thursday, before equally rallying yesterday to reclaim $4,100.

Last week, Spot BTC ETFs sold $897.6M bitcoins, ending a four-week inflow streak, with Fidelity’s FBTC fund leading the outflows on Friday. Spot Ethereum ETFs also had an entire week of negative flows, selling $795.8M worth of the token over the past five days.

The stock prices of Ethereum treasury companies have also plummeted recently in line with the decline in Ether. The largest holder of ETH, Bitmine Immersion Technologies, is down 13% in the last 5 days while Sharplink Gaming is down more than 10% over the past month.

The rally that began yesterday has pushed SOL back above $200, however the token has still pared back most of its gains following announcements of major purchases from digital asset treasury companies last month. Galaxy Digital, Multicoin Capital and Jump Crypto in late August announced plans to raise $1B to accumulate SOL tokens via Forward Industries, a Nasdaq-listed company, while in mid-September, Pantera Capital announced a $500M funding for Helius, another Solana backed treasury company. Together, these DATs now hold 3.64% of the token’s supply.

Don't miss what's next

Upgrade your Block Scholes account to unlock this article and other exclusive insights

After falling below $112K on Thursday afternoon last week, BTC traded sideways on Friday and the early half of the weekend. Since yesterday evening however, spot price has recovered slightly, now once more trading just below $112K.

ETH had seen a similar sideways movement after dipping below $4,000 on Thursday, before equally rallying yesterday to reclaim $4,100.

Last week, Spot BTC ETFs sold $897.6M bitcoins, ending a four-week inflow streak, with Fidelity’s FBTC fund leading the outflows on Friday. Spot Ethereum ETFs also had an entire week of negative flows, selling $795.8M worth of the token over the past five days.

The stock prices of Ethereum treasury companies have also plummeted recently in line with the decline in Ether. The largest holder of ETH, Bitmine Immersion Technologies, is down 13% in the last 5 days while Sharplink Gaming is down more than 10% over the past month.

The rally that began yesterday has pushed SOL back above $200, however the token has still pared back most of its gains following announcements of major purchases from digital asset treasury companies last month. Galaxy Digital, Multicoin Capital and Jump Crypto in late August announced plans to raise $1B to accumulate SOL tokens via Forward Industries, a Nasdaq-listed company, while in mid-September, Pantera Capital announced a $500M funding for Helius, another Solana backed treasury company. Together, these DATs now hold 3.64% of the token’s supply.

Don't miss what's next

Upgrade your Block Scholes account to unlock this article and other exclusive insights

Premium

$30/mo

Access previous and future reports, market insights & deep dives.

Bitcoin has rebounded from a sideways range around $89K to $92K, while Ether has moved from $3K to just under $3.2K, despite weekly outflows of $87.7M from spot BTC ETFs and $65.4M from spot ETH ETFs. Implied volatility term structures are modestly inverted, with 7D BTC IV at 50% versus 47% for 180D, and 7D ETH IV at 73% versus 70% for longer tenors, while 30D skew sits at -6% for BTC and -4% for ETH, indicating a smaller downside premium for Ether. In traditional markets, the S&P 500 is up over 17% year to date and sits just below its October all-time high, while BTC is now -2% year to date after the October liquidation. Into Wednesday’s final FOMC meeting of the year, markets are pricing an 87% probability of a 25bp cut, with core PCE at 0.2% MoM and 2.8% YoY, and University of Michigan consumer sentiment ticking up to 53.3 in December from 51 in November.

BTC stalled after an intraday spike to $94k and now trades just above $91k, with ETH slipping from $3,200 to $3,100 as short-dated OTM put premia compressed from 11 to 5 vols over calls in BTC and to ~2.5 vols in ETH, even as ETH is only +4% over five days despite BitMine nearing 5% of supply and the Fusaka upgrade going live. Spot flows remain a headwind: spot ETH ETFs have taken in just $9.8m net so far this week, while spot BTC ETFs have seen $142.5m of outflows including a $194.6m single-day bleed, the largest since 20 November. Structurally, 21Shares secured approval to list the first US Sui-linked leveraged product, the 2x SUI ETF (TXXS), taking the crypto ETF tally to 74 for 2025 and 128 overall, while Base launched a Chainlink-CCIP bridge to Solana to move SOL/SPL and Base-native assets cross-chain.