Thahbib Rahman

Research Analyst

World Liberty Financial is a yet-to-be-released DeFi platform backed by President Trump (the ‘Chief Crypto Advocate’ for the project). In this report, we take a deep dive into everything World Liberty Financial – covering the Goldpaper (the President’s version of a crypto whitepaper), the tokenomics of the WLFI token, the revenue model of the business, and some of WLF’s current partnerships. Along the way, we will unravel some interesting insights behind the intention and potential end-goal of the Trump family’s crypto endeavour.

.jpg)

World Liberty Financial is a yet-to-be-released DeFi platform backed by President Trump (the ‘Chief Crypto Advocate’ for the project) and his sons (who have been given the role of ‘Web3 Ambassadors’). The goal of the World Liberty Financial Protocol is to “provide users with information and access to third-party DeFi applications”.

The first third-party application the project may provide access to is Aave v3, which will allow WLF users to borrow and lend cryptocurrencies (namely ETH, WBTC, USDT, USDC, and sUSDe) onchain, ostensibly outside the traditional rails of the banking system. The protocol’s stated unique selling point? A user-friendly interface that simplifies DeFi in order to onboard the masses of Web2 users into Web3 and “make crypto and America great” again. Another explicitly stated aim of the protocol is to advance the mass adoption of US dollar-based stablecoins, and in turn strengthen the position of the US dollar. Separately, World Liberty Financial Inc., the developer and owner of the WLF protocol, has also announced plans to launch USD1, a US dollar-based stablecoin.

The third quarter of 2025 remains the proposed start date, though this is still unconfirmed and the website currently allows users to view the team behind the project and purchase the protocol’s governance token (WLFI) only.

In this report, we take a deep dive into everything World Liberty Financial – covering the Goldpaper (the President’s version of a crypto whitepaper), the tokenomics of the WLFI token, the revenue model of the business, and some of WLF’s current partnerships. Along the way, we will unravel some interesting insights behind the intention and potential end-goal of the Trump family’s crypto endeavour.

While World Liberty Financial Protocol (WLF) is yet to launch, the protocol has submitted a proposal to Aave’s Governance Forum to be officially deployed as an instance of Aave v3 on Ethereum’s mainnet. This means WLF will utilise Aave’s v3 infrastructure and liquidity pools, but use its own user-friendly interface for consumers. At the time of writing, the only significant proposal made by WLF is to launch an Aave instance, so we will focus our attention in the subsequent section on its details. The launch of the USD1 stablecoin discussed later is separate to the WLF protocol itself but will be launched by World Liberty Financial Inc., the owner and developer of the WLF DeFi platform.

However, while the project’s October 2024 Goldpaper (World Liberty Financial Protocol’s whitepaper equivalent) mentions only the Aave proposal by name, it does state that the protocol aims to provide users access to other third-party DeFi applications in the future such as “third party digital wallet providers for acquiring, holding and transferring stablecoins”. Taken from one of the co-founders of the project, Zak Folkman, “We can’t expect the everyday person who’s just trying to go to their job, save some money, spend time with their family, to sit at home and nerd out and figure out seed phrases and wallet abstraction”.

This suggests the Trump-backed project so far aims to utilise a pre-existing DeFi model that works, while reducing its barrier to entry. By choosing the right protocols, WLF plans to achieve its goals of “advancing the adoption of USD-pegged stablecoins and strengthening the US Dollar’s position”.

Aave is a decentralised liquidity protocol that allows users to borrow and lend cryptocurrencies via liquidity pools across Ethereum and 13 other blockchains. Lenders provide liquidity to a pool by depositing a specific token into the pool’s smart contract, and in return earn a yield. Simultaneously, the pooled funds in that same contract can be drawn upon by borrowers, who access the token as long as they lock in collateral that is of greater value than their borrowed position (overcollateralised positions) and pay a fee.

When a lender deposits reserves into a pool, they receive a corresponding amount of derivative tokens, called Aave tokens (aTokens for short), which track their share of the underlying asset deposited to the pool. The number of tokens held by the depositor grows over time as the pool accrues interest from borrowers. Interest rates paid by borrowers and collected by lenders are determined automatically by an algorithm based on the supply and demand of funds in the pool. If a borrower’s collateral falls below a pre-determined threshold (while remaining over-collateralised) the borrower is liquidated.

World Liberty Financial’s proposal to deploy a whitelabelled instance of Aave v3 means that it will use the existing liquidity pools of Aave’s latest protocol implementation, Aave v3. The proposal will initially allow WLF users to deposit ETH, WBTC, USDC, and USDT into the pool, therefore also bringing new liquidity to Aave. Users can then use those deposited assets as collateral to borrow any of the other assets in the list.

For example, a user could deposit USDC, and then use that deposit as collateral to borrow a smaller amount of ETH and pay a fee to have the ability to do so. There are many reasons a user might want to pay a fee in order to do this, such as getting leveraged exposure to ETH, taking advantage of arbitrage on ETH lending rates between different platforms, or simply to just borrow funds with more flexibility than the traditional banking system. Additionally, as part of the Aave instance proposal, users are incentivised to supply assets into the WLF Aave v3 pools in exchange for earning a yield and $WLFI tokens.

Separately, there is a proposal on WLF’s Governance platform (described in more detail later), to enable Ethena’s sUSDe as an additional eligible collateral asset as part of the Aave v3 instance. Ultimately, in its current form, WLF plans to facilitate the borrowing and lending of crypto-assets.

Stani Kulechov, the founder of Aave, confirmed that WLF’s instance of Aave is not quite the same as a direct copy of Aave. According to Aave documentation, a friendly fork of the protocol would entail a project utilising Aave’s open source code, but creating its own liquidity, thus making it an independent instance of Aave. World Liberty Financial will not be a friendly fork – it is instead referred to as a Whitelabel Instance, which makes use of Aave liquidity and will collaborate directly alongside Aave.

The goal of enabling users to borrow and lend cryptocurrencies goes hand-in-hand with the choice to implement a version of Aave – Aave is after all crypto’s largest DeFi lending protocol, both by market-cap of its token and liquidity of its lending markets. But why has the Trump team chosen this goal? Why has WLF adapted Aave, and not instead forked Uniswap as its initial third-party DeFi application to become a platform for facilitating crypto-token swaps? An instance of Uniswap v4 with a more user-friendly interface would have still advanced some of the main goals of WLF: “democratizing access to DeFi and fostering mass adoption of DeFi and cryptocurrency”.

One potential answer to this relates to another long-standing goal of President Trump and a mission objective of the WLF Protocol too – “preserve the US Dollar’s status” and “dominance”, “supporting a strong US Dollar through decentralized finance,” and finally ensuring that the US Dollar “remains the global reserve currency for the next century.”

By allowing users to acquire, hold, borrow, and lend USDT, USDC, and sUSDe via liquidity pools that enable yield generation, WLF is attempting to drive more attention to US dollar-based stablecoins. President Trump has made it clear on several occasions that he does not plan to create a CBDC in order to help maintain the strength of the US dollar. His January Executive Order on Digital Assets prohibited the establishment and use of a CBDC within the US. Instead, the logic outlined in the WLF Goldpaper is that stablecoins are a potential “new strategy” to further the interest of the dollar that also promotes “financial freedom and privacy”.

Stablecoin issuers, such as Circle and Tether, are significant holders of US treasuries and debt. This is because stablecoin issuers must hold dollar-equivalent assets to back the circulating supply of their stablecoin. US treasury securities (generally T-bills – shorter dated securities) are a popular option to back most of the issued supply of the stablecoin due to their greater liquidity as a reserve asset, ensuring redemption of dollars for stablecoin is possible. This in turn allows issuers like Circle and Tether to back their reserves, and additionally earn the yield on the treasuries they purchase.

According to Tether's most recent quarterly reserve report, the company has $143B worth of total assets. The report states that 65.74% ($94.47B) of those assets are in the form of US Treasury bills. Additionally, Tether holds $17B worth of Overnight Reverse Repurchase Agreements and Term Reverse Repurchase Agreements, i.e., Treasury-backed repo transactions with the Federal Reserve.

Based on the above information and December 2024 data from the Treasury Department, if Tether was a country, it would rank as the 19th largest foreign nation holder of US debt. WLF’s Goldpaper states that the growing presence of USD-based stablecoin issuers as holders of US Treasury notes “help support liquidity and stability in the US financial system”.

This makes sense given that stablecoin issuers are picking up some of the slack from foreign holders of US treasuries, who have been offloading them at record speed. As stablecoin issuance continues to grow (stablecoin market cap increased 66% since the start of 2024 alone), the demand for US treasuries to back newly minted supply will also continue to grow – hence potentially providing President Trump’s government a relatively price-inelastic purchaser of US debt – or at least one that is driven by factors independent of other large buyers.

However, the Trump project is not just solely looking to promote the growth of existing dollar-based stablecoins. World Liberty Financial Inc., the owner of the WLF protocol, has also officially announced plans to launch USD1, “a stablecoin redeemable 1:1 for the US dollar”. The stablecoin’s smart contract was initially deployed on March 4 on both the Binance Smart Chain and the Ethereum blockchain, according to data from BSCScan and Etherscan, with a supply of 3.5M on each network and confirmed by the WLF team on March 25.

USD1 will be “100% backed by short-term US government treasuries, US dollar deposits and other cash equivalents”, meaning it will be a fiat-backed stablecoin, similar to Tether. Therefore, World Liberty Financial, through USD1, will now act as another significant purchaser of US treasuries on behalf of USD1 token holders.

To compensate for the fact that the technical aspects of the WLF Protocol will leverage Aave for its liquidity and back-end functionality, the November 2024 proposal advanced on Aave’s governance forum proposes that AaveDAO will receive 20% of the fees generated by WLF. Whilst 20% generally appears to be a relatively low fee for a white label service, relative to previous fork / white label proposals in Aave’s history, 20% is at the higher end of the range according to Aave’s own records. Additionally, providing AaveDAO 7% of the $WLFI token supply is significantly higher than all previous white labellings.

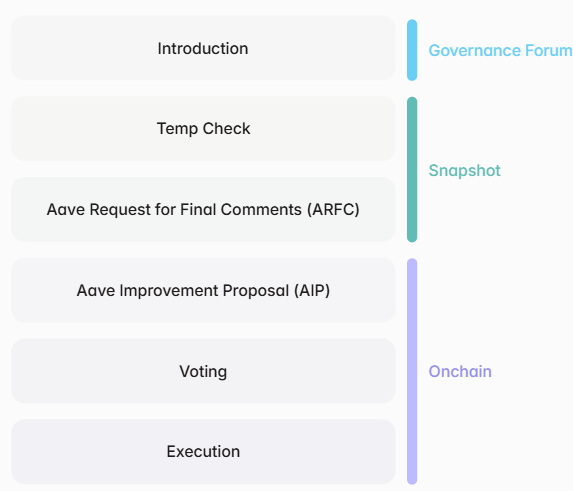

The AaveDAO represents the community of Aave token holders who can vote on different aspects of the protocol through a governance process. That process allows different proposals to be made by the community, which tokenholders can then vote on. The first stage of a proposal is the ‘Temperature Check’, which involves an informal vote to gauge community sentiment. The next is the Aave Request For Final Comments (ARFC) where the proposal is scrutinised in more detail. The WLF proposal has successfully passed the ARFC stage, with the next part of the process being the Aave Improvement Proposal (AIP) – where the proposal is formally submitted on-chain, voted on, and then executed. It is not yet clear when this stage will occur.

With a solid understanding of the WLF Protocol and its goals, we can move to the protocol’s unique governance token, WLFI, and its role in the WLF Governance Platform. The World Liberty Financial Governance Platform is a community governed through the WLFI token, similar to how Aave tokenholders govern the Aave DAO. However, the WLF Governance Platform is technically not a DAO. The Goldpaper states that both the WLF Protocol and the Governance Platform are owned and operated by World Liberty Financial Inc. (WLFI) – an “American, tax-paying” Delaware nonstock corporation.

Each WLFI token represents a vote on different matters on the WLF Protocol. For example, WLFI holders can determine the future of the protocol by approving new proposals on the protocol itself. Any WLFI holder is also able to make their own proposal. Each WLFI token is entitled to one vote on the WLF Governance Platform. However, according to the Goldpaper, no single wallet or “group of affiliated holders” can vote with more than 5% of the total token supply, meaning there is a hard-cap 5% votable limit. It is not clear from the Goldpaper how this will be enforced, though the KYC requirements in the subsequent section are a likely practical contender. WLFI tokenholders can also submit their own proposals and let other holders vote on those proposed protocol changes.

The proposal and voting mechanism involves the following stages:

WLFI tokens were available for purchase on the World Liberty Financial website through two public sales. In the first presale, the tokens were set at $0.015 by the WLF team, and in the second, the predetermined price was $0.05. The first public sale for WLFI tokens began on October 15, 2024 and the second presale ended March 17, 2025. As of now, World Liberty Financial has sold all 25B tokens that were available for public sale for a total of $550M.

However, while the goal of the protocol is to advance the adoption of DeFi in the US, most American citizens were actually unable to participate in the protocol. This is because only accredited US individuals were able to purchase the token – under US Securities Laws that meant only US investors with a minimum net worth of $1M and an individual income of $200,000 were eligible. They also needed to pass WLF’s own KYC process. However, all non-US citizens were able to purchase WFLI tokens, restricted only by the KYC process. According to WLF, more than 85,000 total participants in the token sales underwent the KYC process.

Unlike most governance tokens (like Uniswap’s UNI or Maker’s MKR), WLFI is nontransferable after purchase and cannot be sold, swapped, or traded like normal tokens. This was to prevent attracting speculative investment in the project and instead focusing purely on the governance aspect to ensure tokenholders. The idea being that, by removing the financial incentive, tokenholders (the only ones who can change the protocol) are more likely to approve proposals that are in the best interest of the protocol – though this cannot be guaranteed.

While all purchases of the governance WLFI token did require KYC, it is less clear from the Goldpaper whether any KYC will be required to access the World Liberty Financial Protocol itself – this is not clarified by the Goldpaper, though a recent partnership collaboration suggests even access to the WLF protocol itself will not be permissionless and require KYC (more on that later).

However, there are other aspects of the project which are on the murkier boundaries of decentralisation. Firstly, 30% of the 100B total supply of WLFI tokens will be distributed to “Initial Supporters” of the project – these supporters are DT Marks DEFI LLC, Axiom Management Group, LLC and WC Digital Fi LLC.

Though the Goldpaper states that “None of Donald J. Trump, any of his family members … is an officer, director, founder, or employee of, or manager, owner or operator of World Liberty Financial or its affiliates or the WLF Platform”, the reality is that “DT Marks DEFI LLC will receive 22.5 billion WLFI tokens and a right to receive 75% of the net protocol revenues” (i.e., 75% of the protocol revenue net the 20% fees to the AaveDAO and any other operating expenses). This means while the Trump family is not officially associated with the project via a director or founder relationship, DT Marks DEFI LLC, “an entity affiliated with Donald J. Trump and certain of his family members”, is the primary beneficiary of any profit the project makes and holds almost as much as the entire pre-sale amount of 25 billion WFLI tokens.

What do Trump and co need to do in exchange for such a large portion of the protocol revenue? Taken directly from the Goldpaper: “the owners and principals of DT Marks DEFI LLC, including Donald Trump” simply need to “promote the WLF and the WLF Protocol from time to time”. The remaining 25% of protocol revenue will be split amongst the other “initial supporters” of the project mentioned above.

A centralised revenue sharing model that gives 30% of the token supply to initial supporters of the protocol seems slightly counterintuitive for a project which is centred around promoting decentralisation. The Goldpaper does state that “no wallet may vote more than 5% of the total token supply” which helps minimise centralised voting power. However, it is less clear on how the protocol plans to tackle a situation where a single entity holds multiple wallets or when multiple entities collude with one another to gain a large, outsized proportion of the voting power.

Beyond the implementation of Aave, buying and lending cryptocurrencies, and links to the Presidential family, World Liberty Financial has garnered considerable attention for another reason – its aggressive accumulation of several cryptocurrency assets. The protocol recently announced a ‘Macro Strategy’: “a strategic token reserve designed to bolster leading projects”. The aim of the reserve is to diversify WLF holdings across various crypto-assets, and invest in their ecosystems to support the DeFi landscape further. Additionally, the assets will be held in “WLFI’s public wallet, providing institutions with transparent exposure” to their portfolio holdings.

World Liberty Financial’s public wallet portfolio of assets is worth $79M. Some crypto project developers have seemingly sent their token to the WLF public wallet address (and therefore the wallet appears to hold 180 different tokens) we display a breakdown of the largest holdings below – the largest current holding being ETH.

However, the above is the current value of tokens held in their public wallet. Looking at on-chain data, their total portfolio is worth over $340M. On-chain data additionally shows that WLF has, at times, sent in a single transaction over $26M worth of ETH to its Coinbase Prime wallet. The team responded to claims that the project was selling its holdings by stating the transfers are “routine movements of our crypto holdings” and “to be clear we are not selling tokens—we are simply reallocating assets for ordinary business purposes”.

The most notable tokens purchased so far have been: Aave – AAVE, Ethena – ENA, Ondo Finance – ONDO, Movement – MOVE, Ethereum – ETH, Wrapped Bitcoin – WBTC, Tron – TRX and Chainlink – LINK. Even more recently, WLF announced it had struck a “strategic reserve deal” with Sui, to add the SUI token to its crypto holdings.

Separately, in mid-February Ondo Finance announced a strategic collaboration with World Liberty Financial that will explore integrating the tokenised assets in Ondo Finance’s Global Markets as additional eligible assets in WLF’s treasury reserve. Ondo’s Global Markets is a tokenisation platform that will allow users to buy and sell thousands of tokens backed 1:1 by traditional stocks, bonds, and ETFs, such as USDY and OUSG, according to documentation from Ondo. However, their Global Markets platform is currently only restricted to users outside of the US as the platform does not yet have full US regulatory approval.

The collaboration also proposes the possibility for “qualifying” WLF users to directly borrow and lend against Ondo’s tokenised securities in the WLF platform itself – likely via new liquidity pools made possible given the Aave backend infrastructure. Those who would qualify are likely only to be non-US persons on WLF given that the Ondo tokenised assets themselves are as yet restricted to non-US users. It is this distinct qualification of non-US and US users who will and will not, respectively, have access to the tokenised assets which suggests the entire World Liberty Financial Protocol itself will not be decentralised.

The World Liberty Financial Protocol is deserving of the attention it has been receiving since its initial announcement in September 2024. So far, while the protocol is still relatively light on details, it is apparent that the World Liberty Financial Protocol is not yet reinventing the wheel in decentralised finance – aiming instead to simplify DeFi to onboard more users and amplify existing solutions to a wider audience. The instance of Aave as the first DeFi application on the platform serves to advance goals of “fostering mass adoption of DeFi and cryptocurrency” and to “help support liquidity and stability in the US financial system”. The timely launch of their own USD1 stablecoin, backed by short-term US government treasuries and dollar deposits, is another indication of World Liberty Financial’s goals.

The protocol has also announced various big-name strategic partnerships with major crypto projects as part of the strategic reserve “Macro Strategy” – the accumulation of various tokens when the project passes the majority of profits to President Trump and his family is another interesting dynamic to consider.

However, while the protocol advocates for the advance of decentralised principles and freedoms, there are many non-decentralised aspects of the World Liberty Financial project. A Trump-affiliated company owns a significant portion of the token supply and will receive 75% of the protocol's net revenue. US citizens were for the most part also excluded from token ownership despite the US first principles.