Thahbib Rahman

Research Analyst

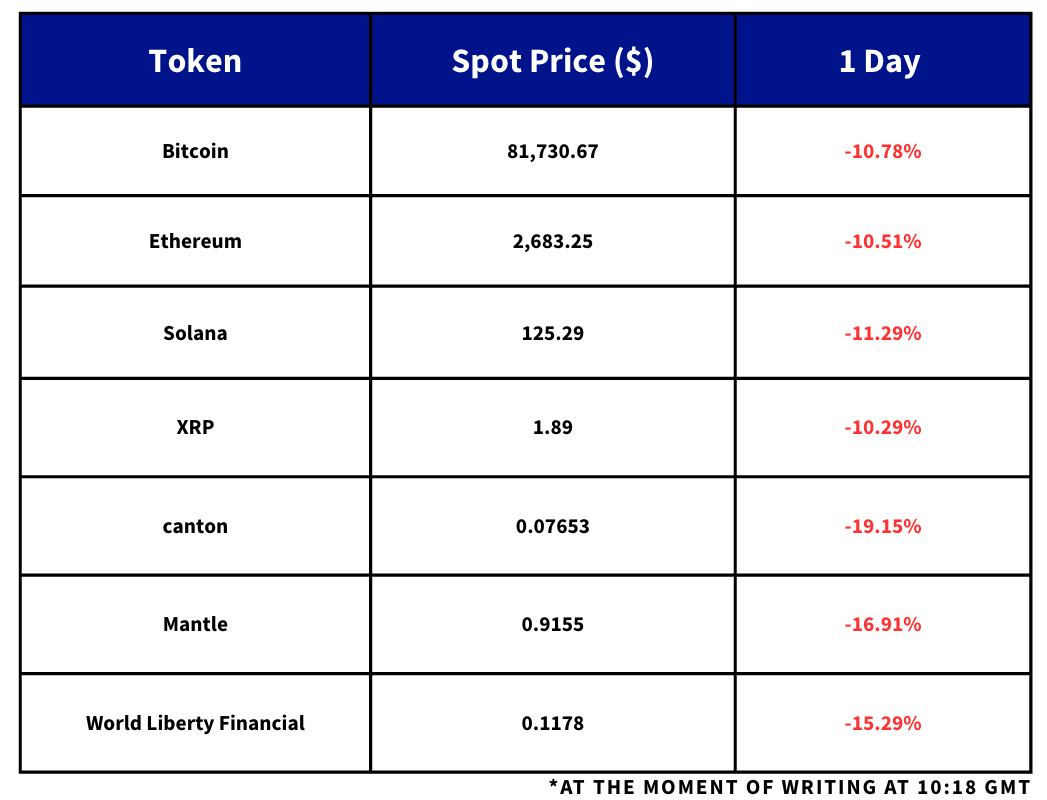

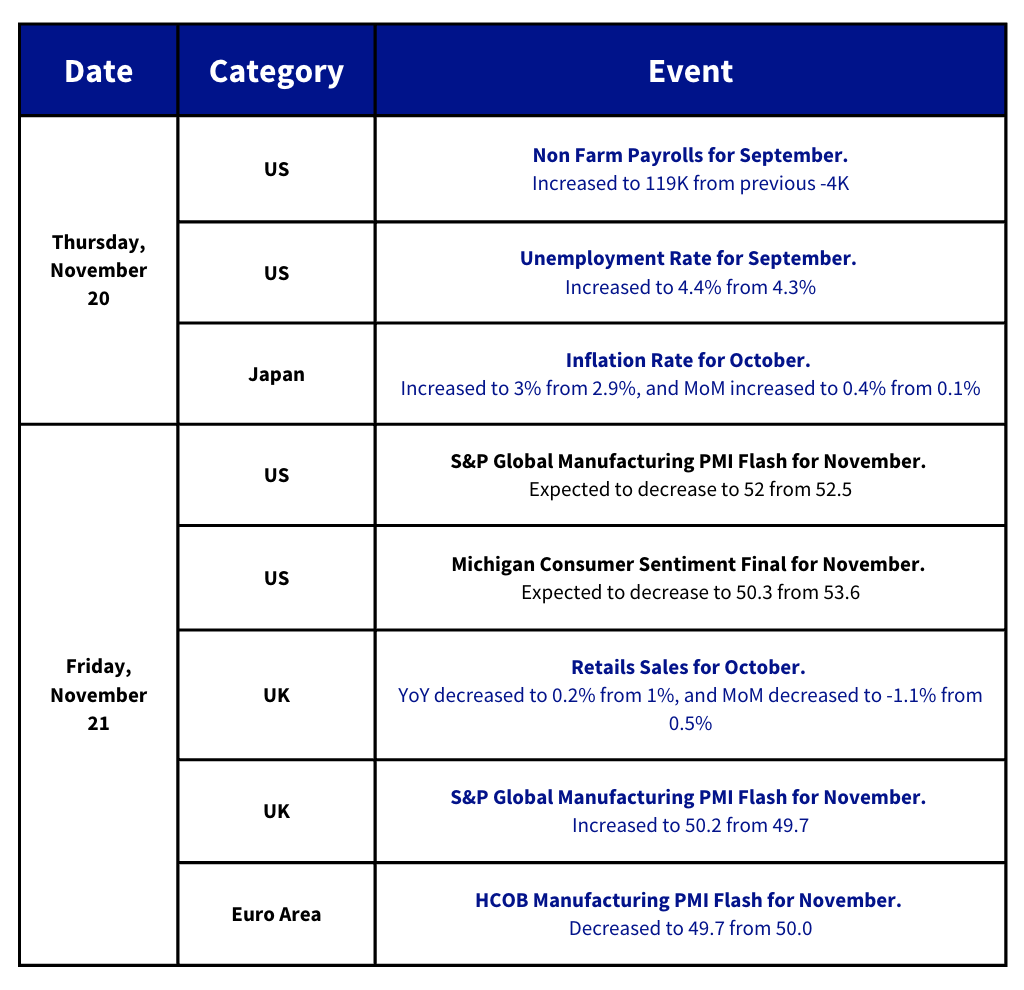

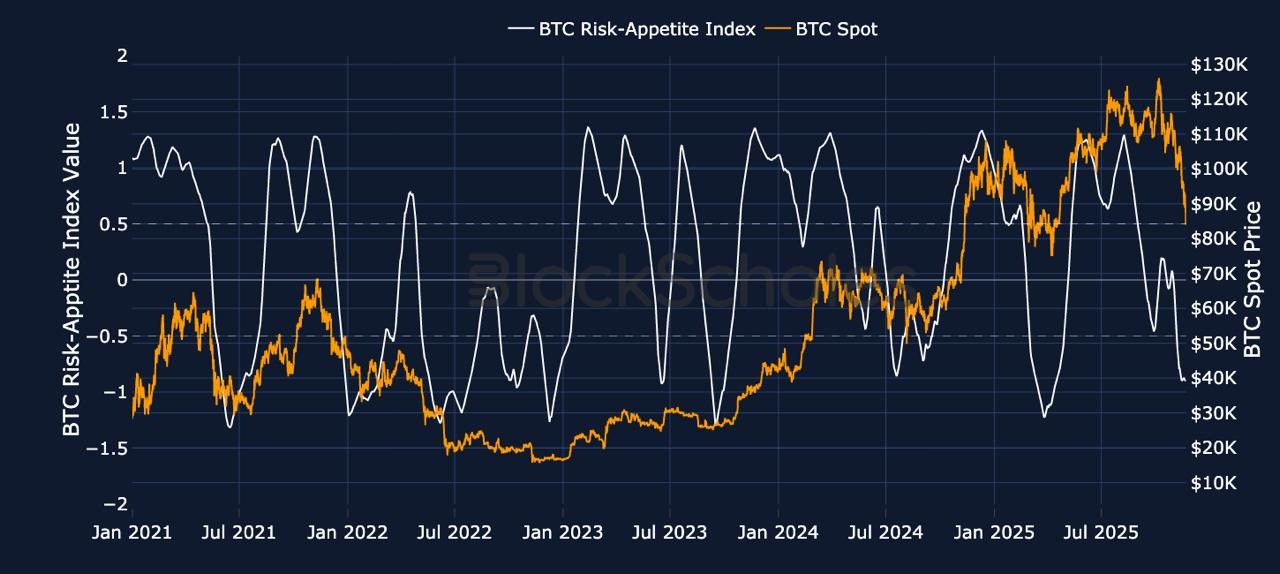

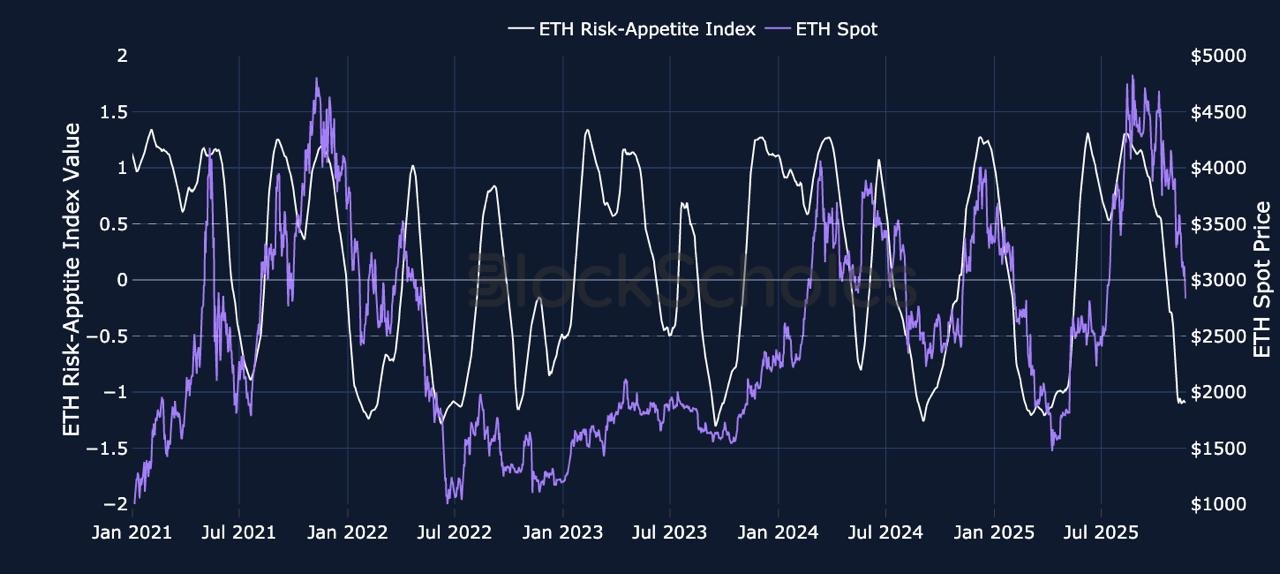

BTC’s selloff deepened with spot hitting $82k (-33% from the October ATH), as spot ETFs have dumped over $5bn of BTC since 10 October, including $903m yesterday (2nd-largest daily outflow on record). 7d realised vol has jumped to ~60%, front-end ATM IV is >60%, and skew is heavily put-rich as the market hedges a potential retest of the $75k April low. Risk-off spilled into US equities, with the S&P 500 down 1.56%, Nasdaq-100 down 2.38%, NVDA down >3%, and the VIX back above 27. A mixed US labour print (119k vs 50k expected, UR up to 4.4%) briefly shifted December Fed pricing, but odds have reverted to ~33% for a cut and ~67% for a pause, while Japan’s ¥17.7tn stimulus has pushed 10y JGBs to 1.84% and weighed on JPY amid intervention warnings and rising idiosyncratic crypto-equity risk around MSTR index inclusion and Metaplanet’s BTC-funded capital raise.