Andrew Melville

Research Analyst

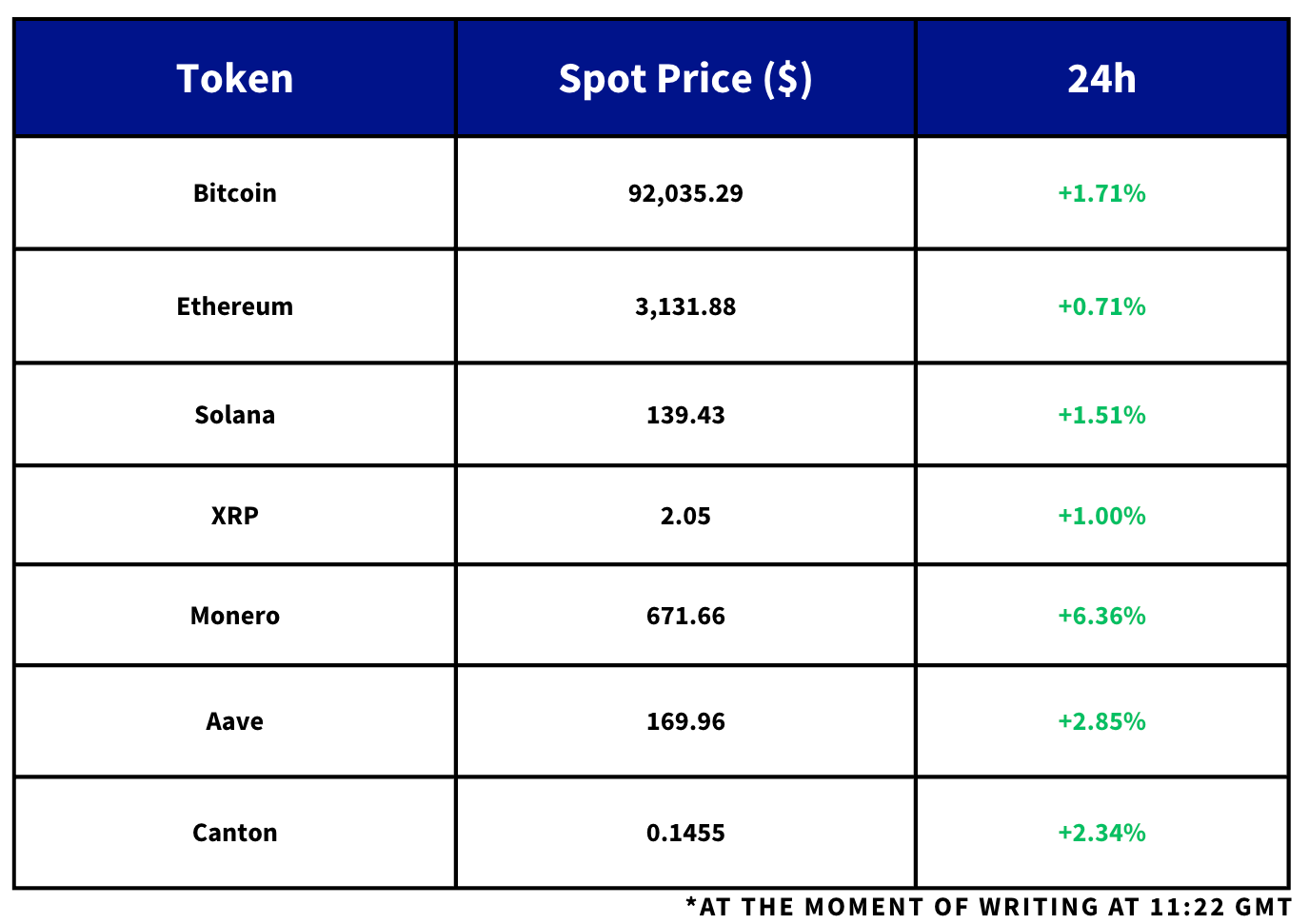

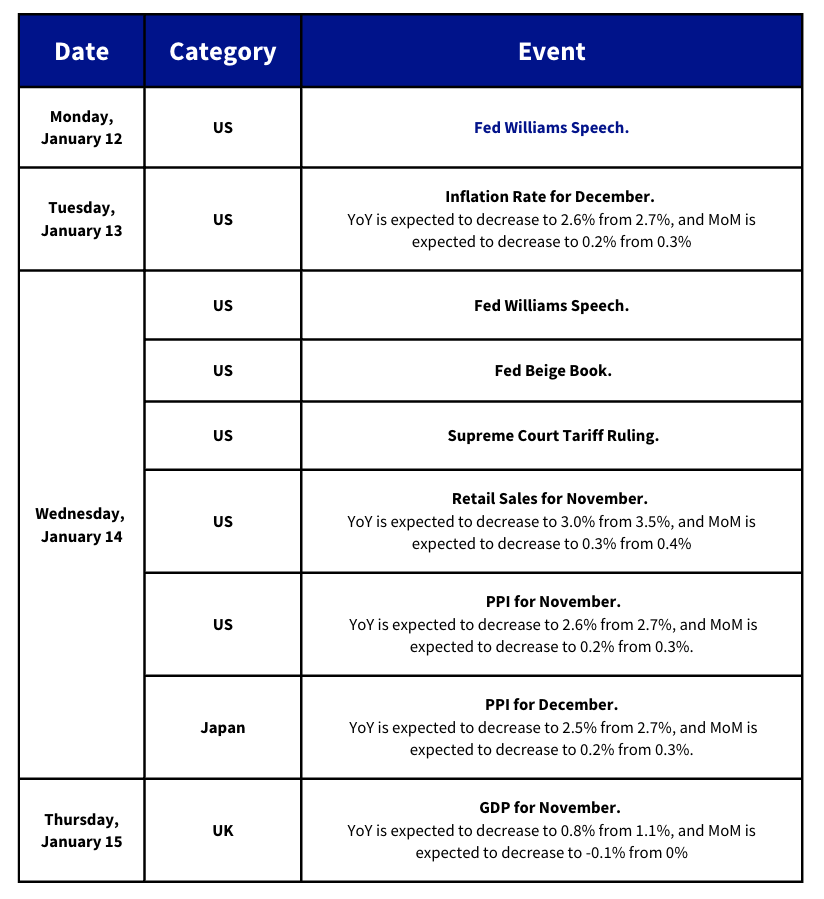

BTC is still rangebound near $90K, briefly touching $92K in Asia before slipping back to about $90.7K, as markets weigh tariff uncertainty, a mixed December jobs report and tomorrow’s CPI. Despite the macro noise, US equities ended last week at record highs and Fed speakers signalled only incremental policy adjustments, with traders leaning toward no change at the end-of-January meeting. Crypto ETF flows were mixed with heavy BTC and ETH outflows, while XRP stayed net positive and set a weekly volume record, as SOL and DOGE cooled and LTC returned to inflows. Policy risk rose again with DOJ subpoenas targeting the Fed, Dubai tightening DIFC crypto rules including a privacy-token ban, and South Korea moving toward reopening corporate crypto trading under a 5% cap.