Andrew Melville

Research Analyst

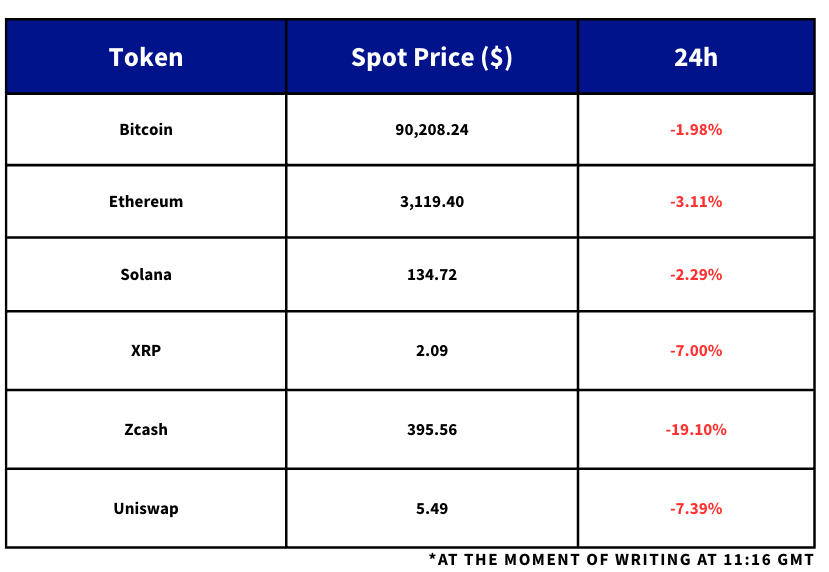

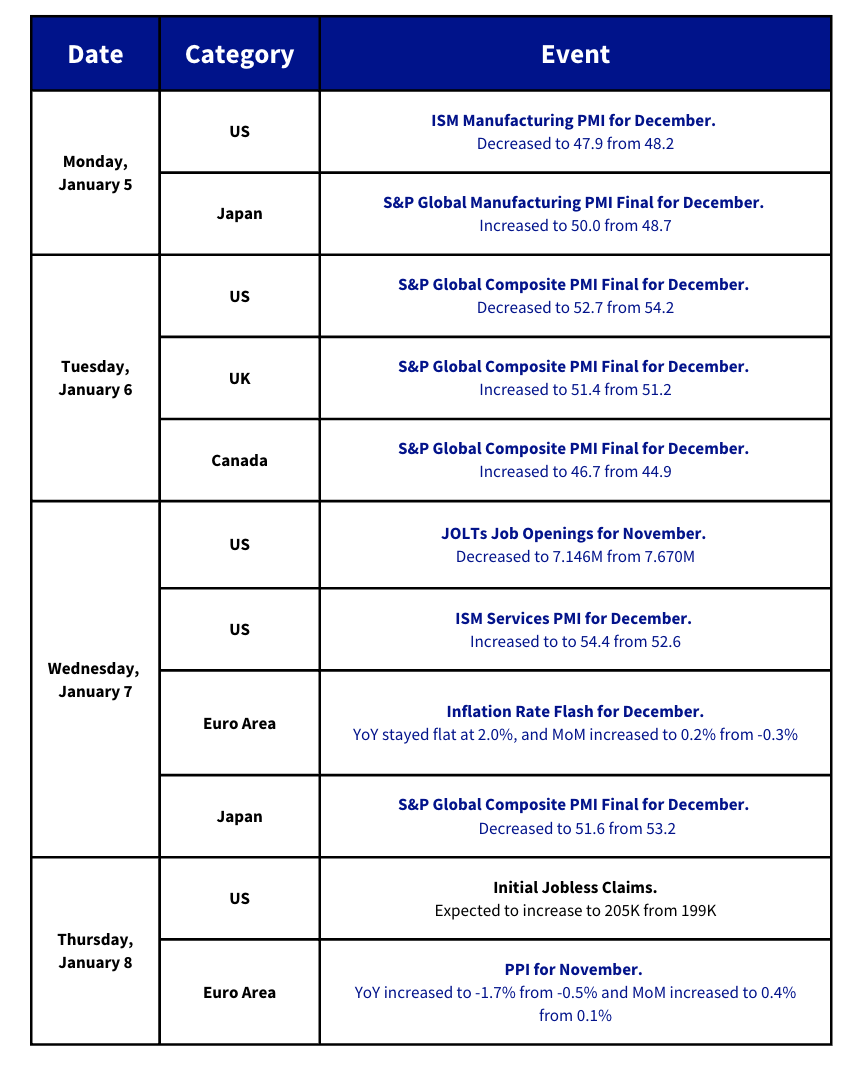

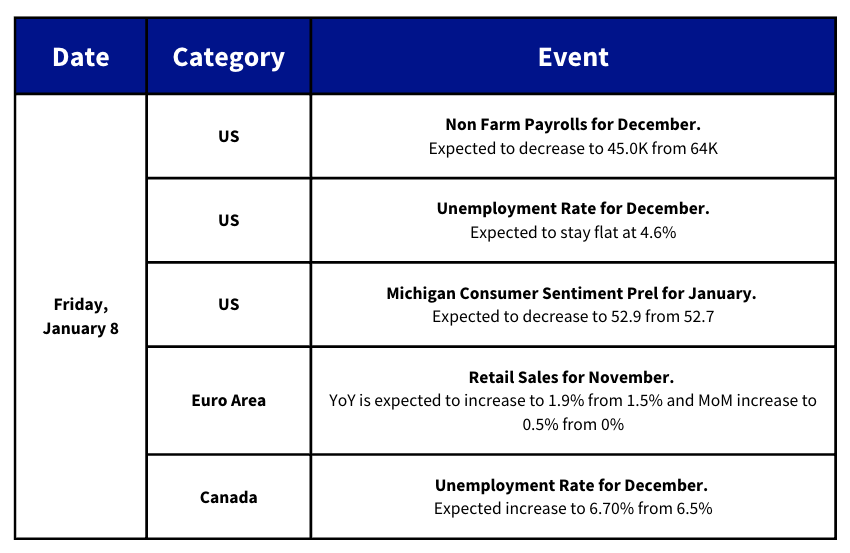

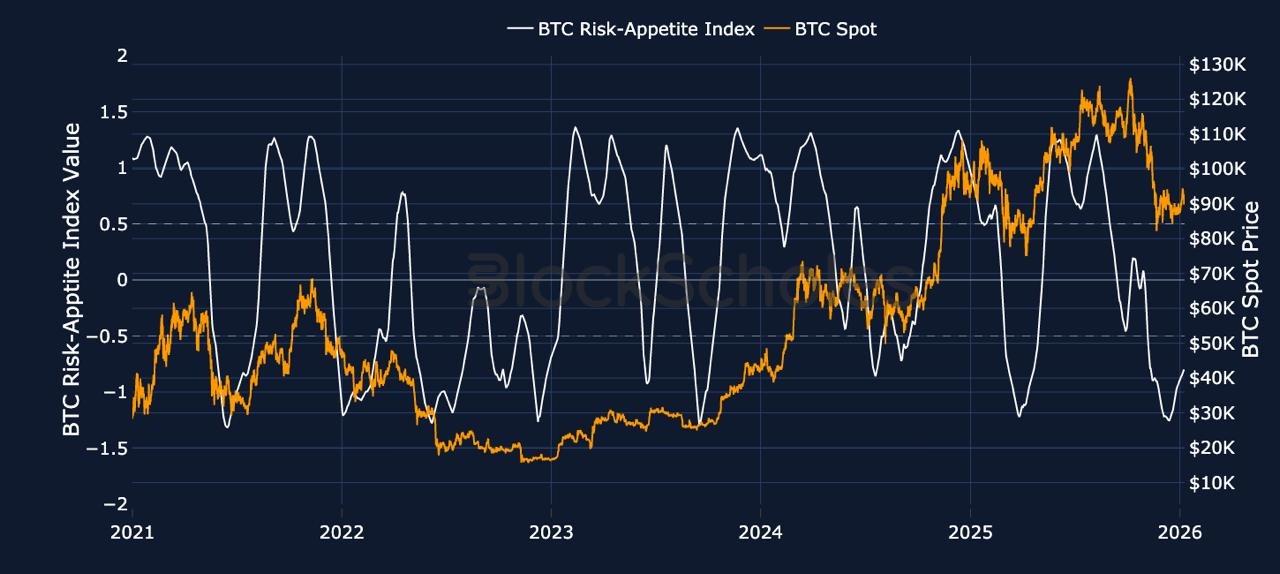

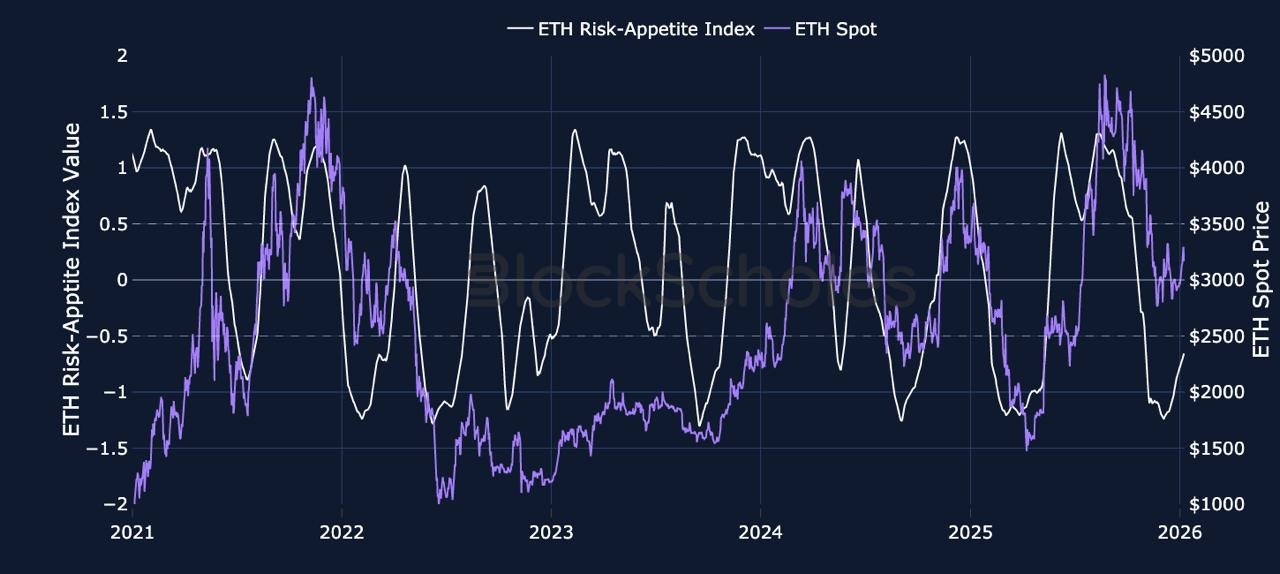

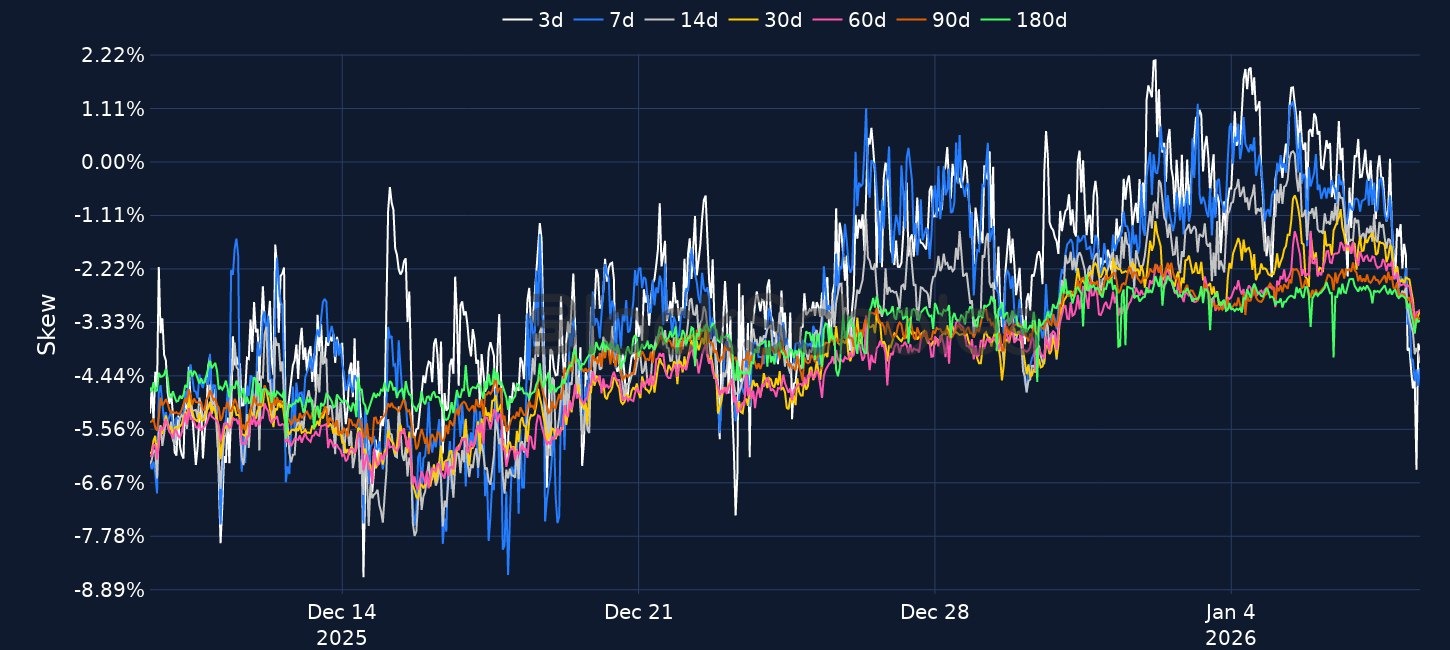

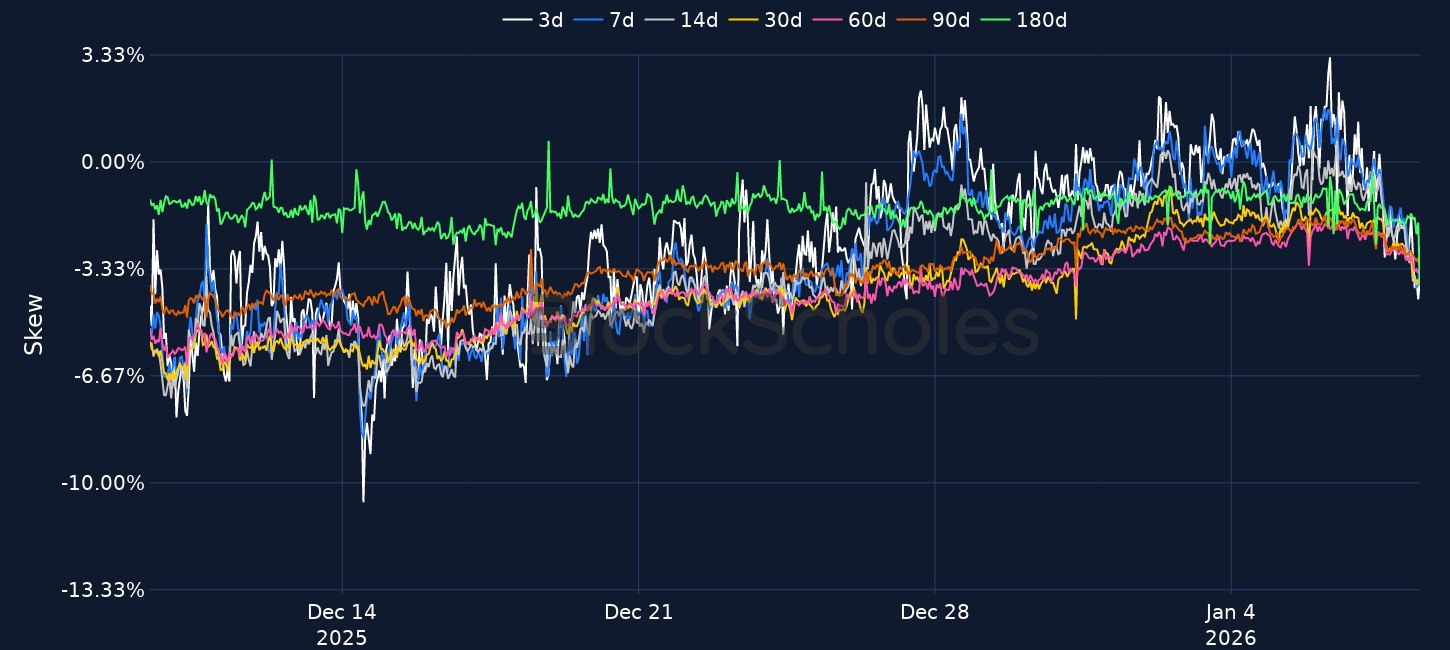

US equities logged their first decline of 2026 as investors digested a hawkish-leaning split in US data: ISM Services surprised to the upside, while JOLTS openings fell to a 14-month low, reinforcing a “low hiring, low firing” labour market. Crypto weakened alongside broader risk, with BTC sliding from ~$93K to below $90K and short-dated BTC and ETH skews flipping decisively toward puts as downside hedging demand repriced. Attention now turns to Friday’s nonfarm payrolls and the Supreme Court’s ruling on the legality of President Trump’s tariffs as the next key macro catalysts. In crypto/TradFi plumbing, World Liberty Financial moved toward formal oversight via a national trust bank charter application for USD1 issuance/custody, while Digital Asset and J.P. Morgan’s Kinexys announced plans to bring JPM Coin to Canton and Polymarket partnered with Dow Jones as Babylon secured $15M from a16z.