Tazmina Rashid

Research Analyst

Crypto-exposed equities are emerging as a new sector in the traditional finance markets, with headlines of crypto native companies going public on the market and existing public companies exploring the addition of crypto and blockchain technologies into their operations. For an investor, decentralised finance exposure can be gained on the equities market through a variety of different business models, such as crypto treasury strategies, exchanges, mining companies and more.

Crypto-exposed equities are emerging as a new sector in the traditional finance markets, with headlines of crypto native companies going public on the market and existing public companies exploring the addition of crypto and blockchain technologies into their operations. For an investor, decentralised finance exposure can be gained on the equities market through a variety of different business models, such as crypto treasury strategies, exchanges, mining companies and more.

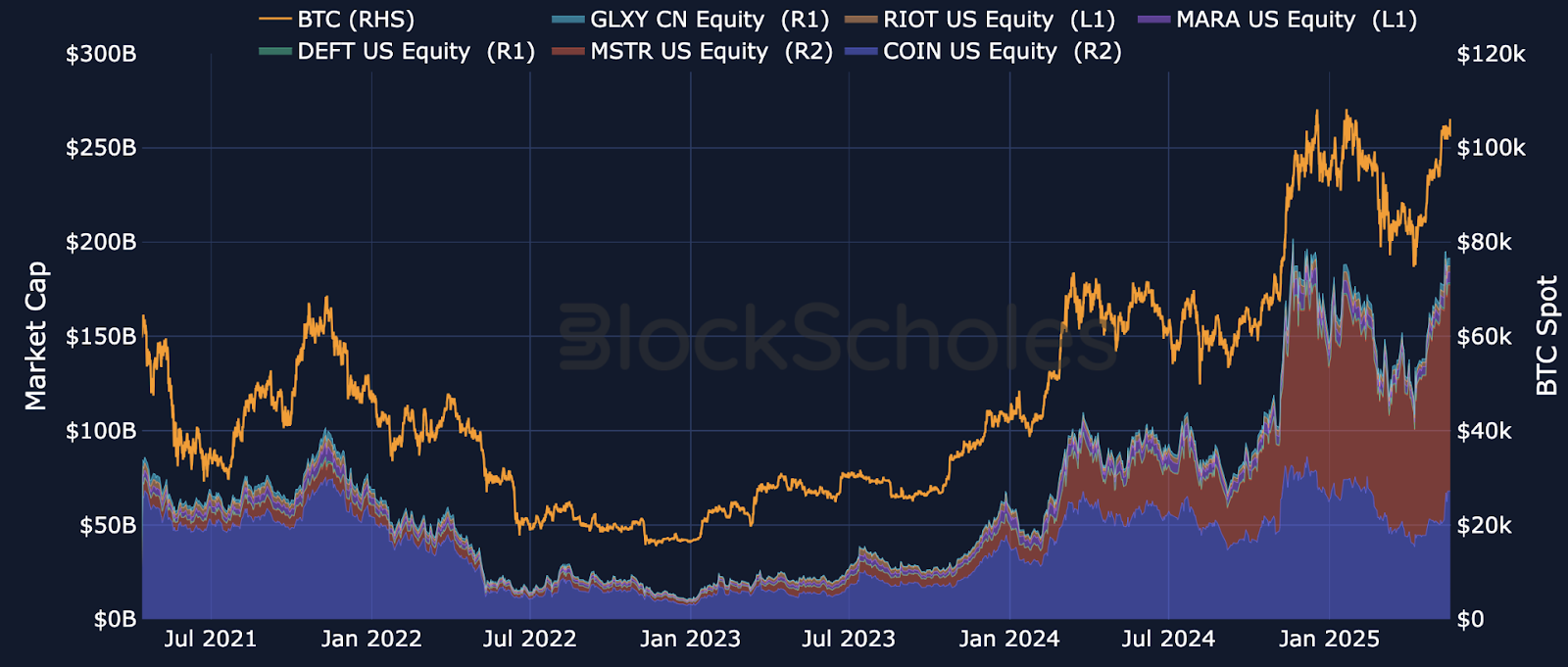

BTC’s spot price is a key driver of the combined market cap of top crypto-related equities. In a crypto bull market, rising token valuations, surging trading volumes and heightened on-chain activity significantly boost the revenue streams of firms dependent on transaction fees, asset custody and mining operations. This encourages investors to increase their exposure to equities whose fundamentals are, at least in part, tied to the performance of the crypto market.

A growing number of publically-traded companies have adopted crypto-focused treasury strategies. These companies view cryptocurrencies as alternative reserve assets generating revenue from their appreciation.

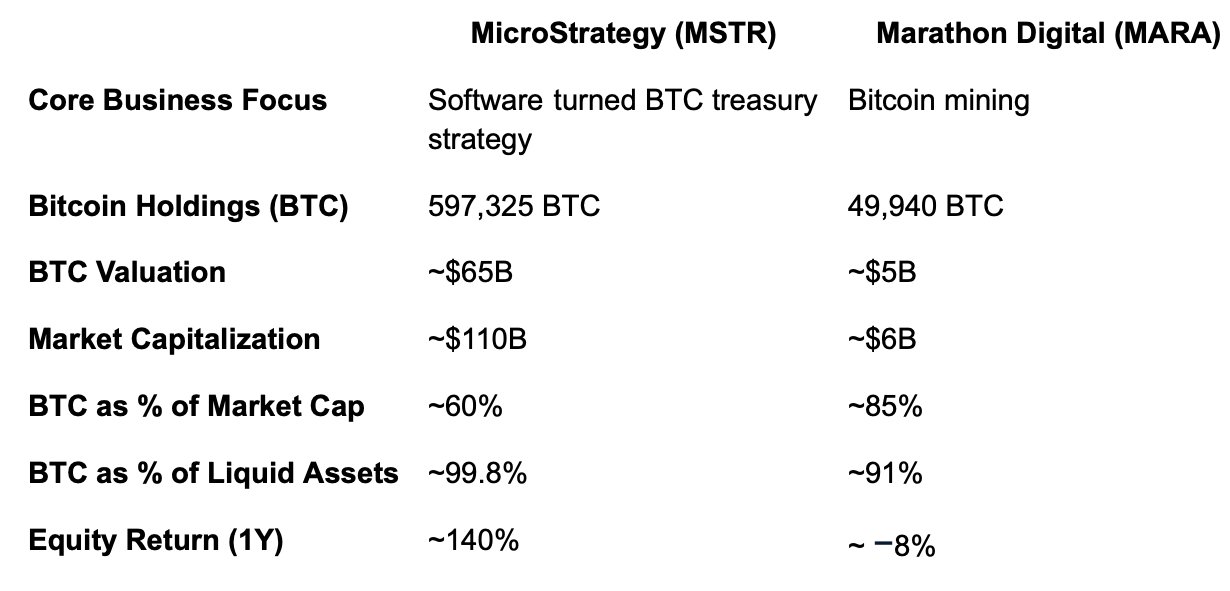

Strategy (MSTR) is the most notable and leading corporate holder of Bitcoin globally with approximately 597,325 BTC worth approximately $65B, as of July 2025. This stands at approximately 60% of MSTR’s $110B market capitalisation. MSTR is recognised as the first publicly traded company to adopt a BTC treasury and as with many emerging treasury strategies, announced a strategic pivot away from its core business in August 2020 with the announcement of a $250M long-term Bitcoin investment. When comparing these figures to their reported $38.1M in cash and other liquid assets, as per their December 31, 2024, 10-k SEC filing, this puts bitcoin at a staggering 99.8% of MSTR’s liquid asset base.

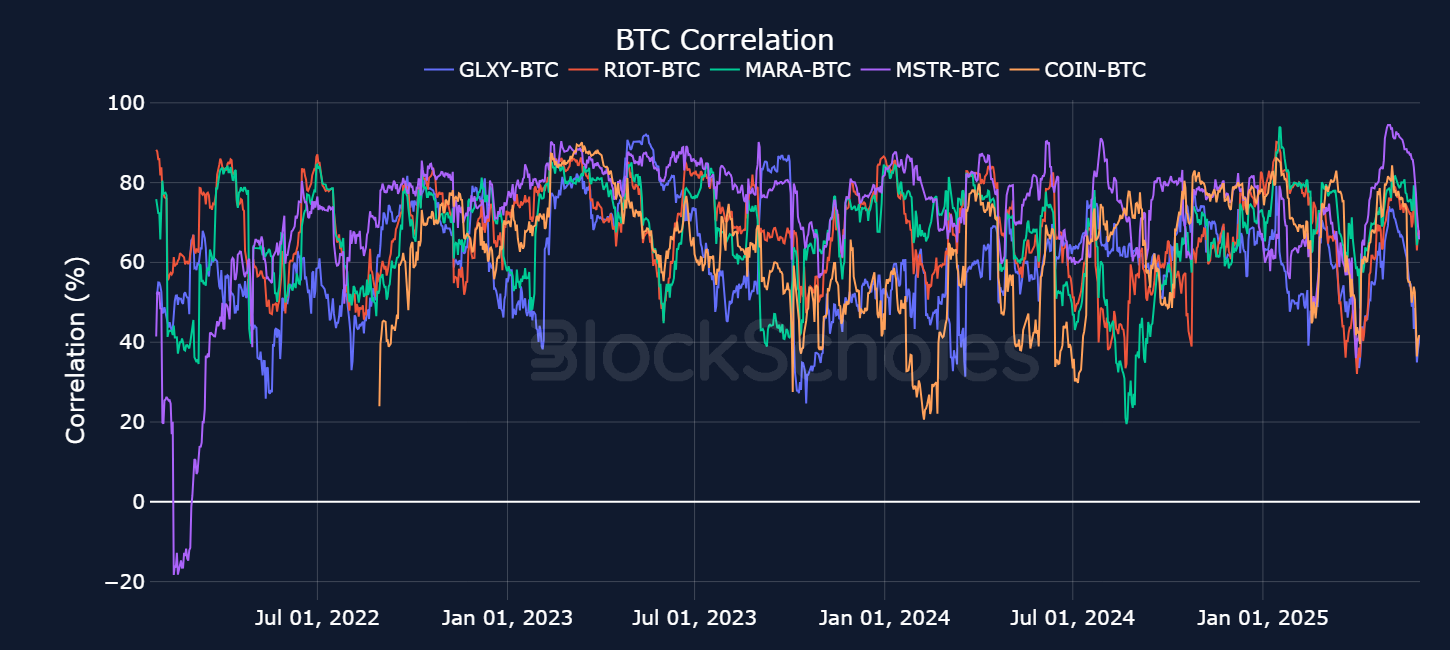

MSTR’s value proposition is primarily driven by its exposure to Bitcoin (BTC). As expected, this means MSTR’s equity returns is highly correlated to BTC returns as shown in Figure 2.

MSTR’s aggressive accumulation strategy aims to increase Bitcoin holdings per share with minimal dilution to shareholders, creating an almost leveraged exposure. This progress is measured by the BTC Yield YTD which currently stands at 16.9%.

As seen in normalised returns below, MicroStrategy (MSTR) business model shows a notable outperformance, up an astounding 2400% over the past 2 years and making BTC’s 500% gain look modest in comparison. This outperformance can partly be attributed to the pro-crypto movement that followed Trump taking office which we covered here and has continued with MSTR furthering their accumulation strategy.

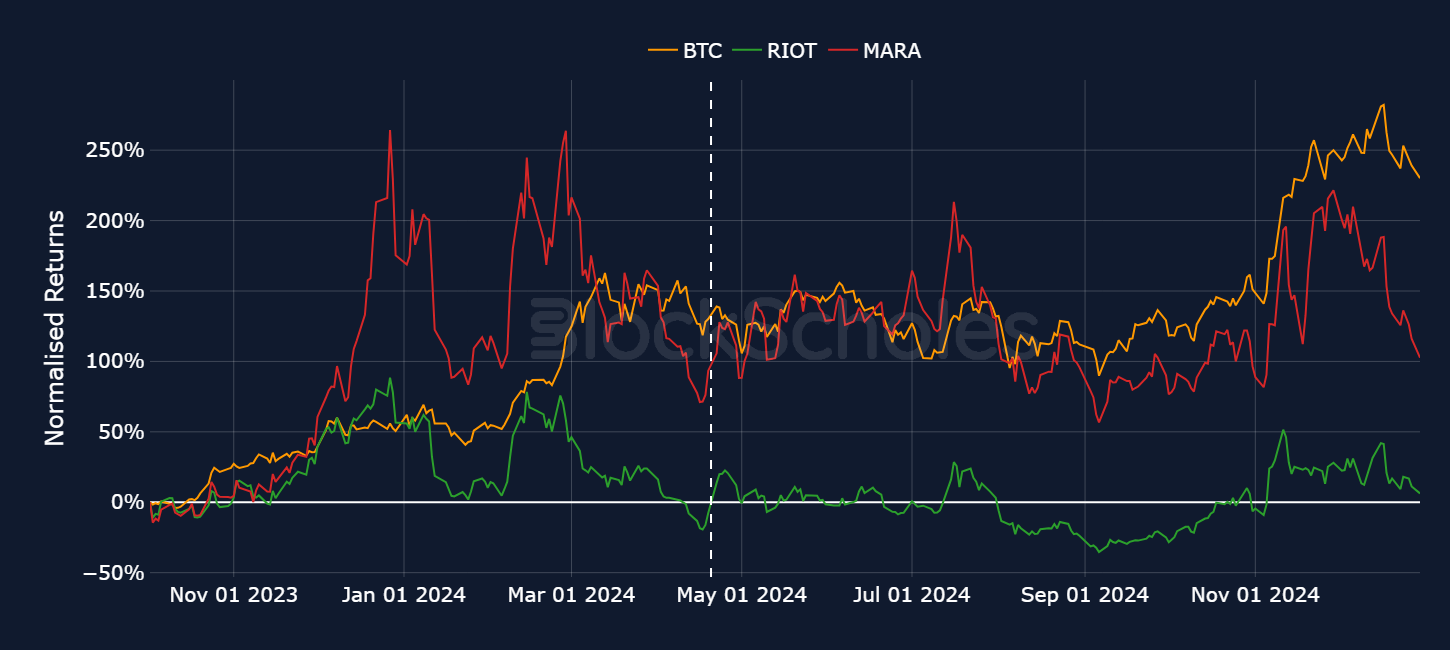

Bitcoin mining company, Marathon Digital (MARA), is currently the second-largest corporate holder of bitcoin after MicroStrategy, with a holding of 49,940 BTC as of June 30, 2025, valued at over $5B. Bitcoin accounts for approximately 91% of MARA’s total liquid holdings and stands at 85% of MARA’s $6B market capitalisation.

To be exact, MARA’s bitcoin mining operation generated a total revenue of $656.4M in 2024, a fraction of their BTC holdings. Marathon’s financial profile similarly reflects a business built around strategic BTC accumulation, yet translates to a different equity price return profile when compared to BTC returns. This aligns with their declared “HODL” strategy where they are “retaining all bitcoin mined in its operations and periodically making strategic open market purchases” through the use of convertible debt to purchase bitcoin, similar to MSTR.

The stark divergence in 1-year equity returns between MicroStrategy (MSTR) at ~140% and Marathon Digital (MARA) at ~−8%, despite both being major corporate holders of Bitcoin, could be attributed to market inefficiencies, where MSTR benefits from a sentiment premium, because of Michael Saylor’s high-profile evangelism and clear BTC-treasury identity.

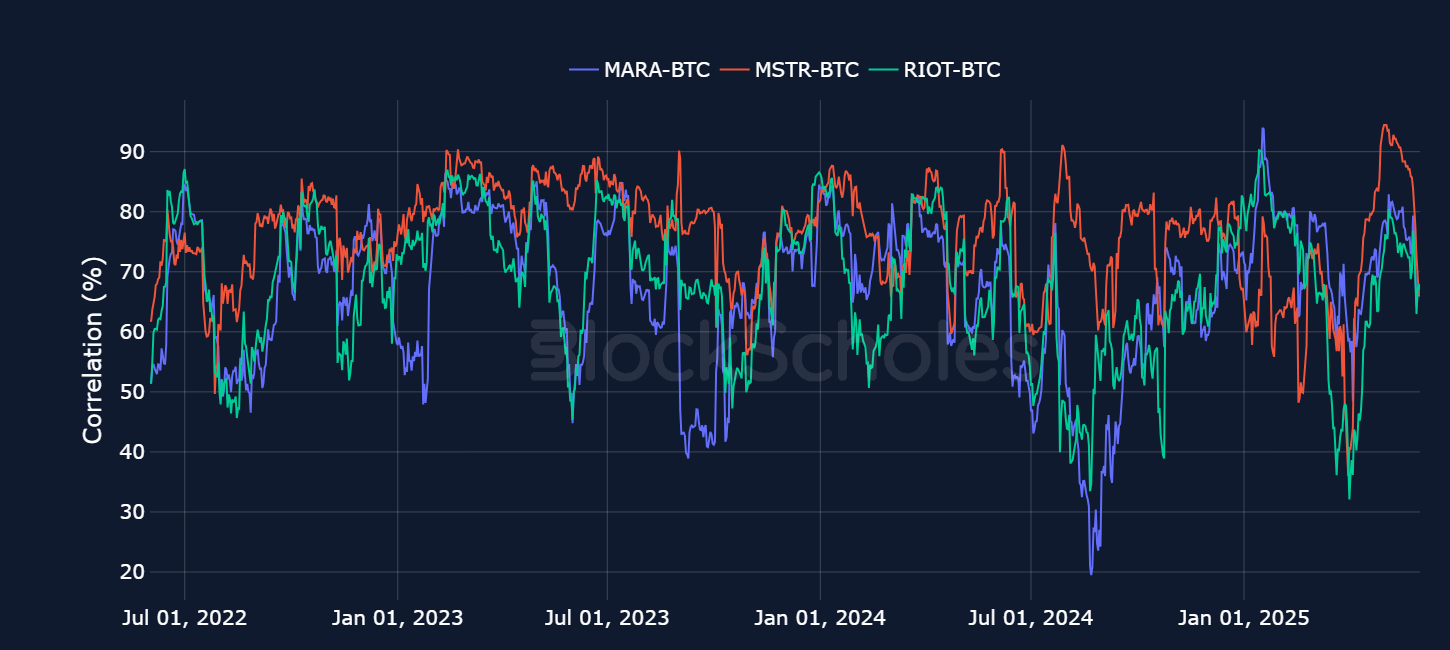

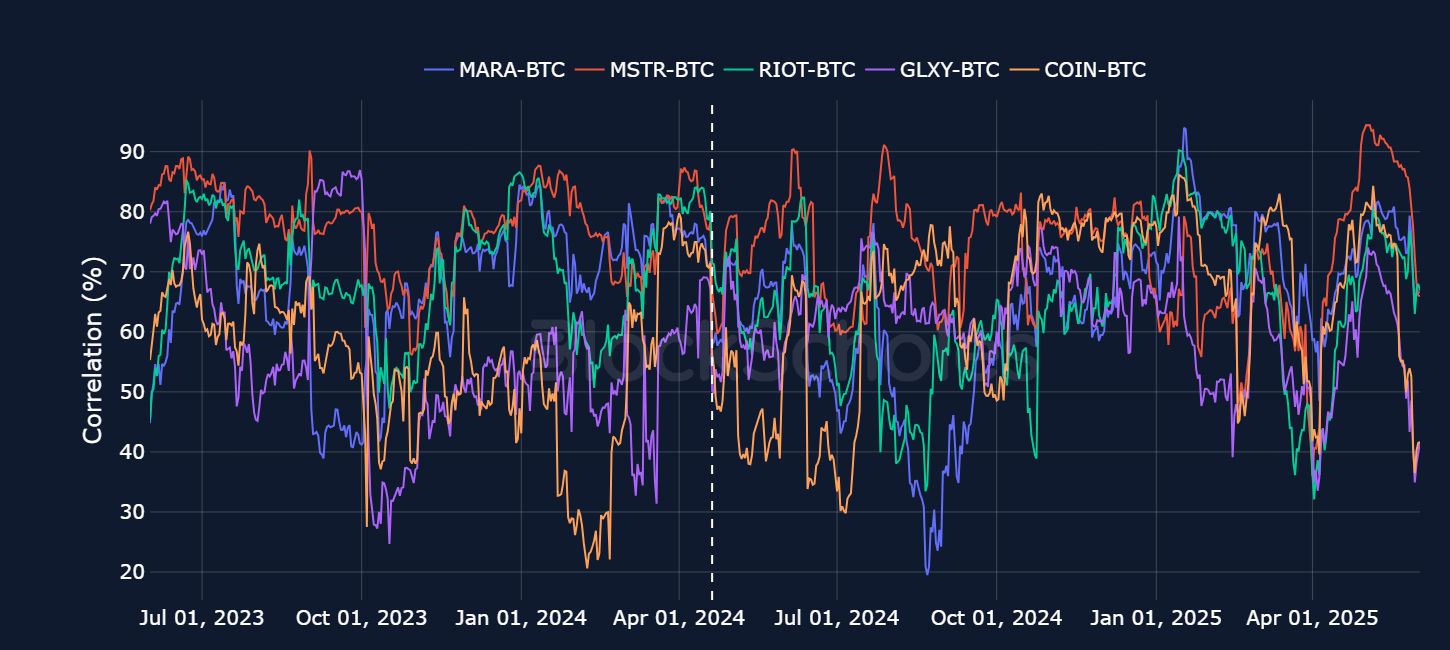

Whereas the market instead looks to define MARA as a bitcoin mining operation, despite it holding a BTC treasury, as seen below by its correlation and returns profile mirrored closely by the 2nd largest public BTC mining company, RIOT. MARA’s operational complexity as a mining company introduces uncertainties that dilute its perceived BTC exposure, leading to a sentiment discount.

In this case, the existence of a Bitcoin treasury alone does not outweigh other aspects of its business. We see the market responding to mining related events such as the BTC halving event on April 20, 2024, indicated by the white line below. Each ticker tumbled in correlation to BTC, post BTC halving. The key difference is that MARA and RIOT’s correlation continued tumbling into Q3 while the others recovered.

Halving events don't directly change the spot price of BTC but do impact miners by reducing the amount of BTC earned per block and lowering mining revenues. MARA’s June 2024 Press Release which accounts for the immediate aftermath of the halving, revealed a 40% decrease in Bitcoin mined year-over-year.

The BTC halving is a known event and can be expected to have been priced in ahead of time. As seen in figure 6, In march 2024, MARA and RIOT can be seen to drop in spot value while BTC gains and retains value. BTC was on a strong bull run during this period reaching an all-time high in March 2024. This translates to the period before the halving seeing both mining company equity returns have exaggerated movements on the back of BTC’s gains. Following the halving, the spot returns deliver a similar scale to btc returns. A big contrast.

There is a narrative that crypto-related equities are used as a proxy for BTC price movement on the equity markets. However, the advent of the first spot Bitcoin ETFs in the U.S. on January 10, 2024 removes the need for this.

Following this logic, we could see a big drawdown in equity returns following the introduction of the BTC ETF while the BTC spot rallies on the back of capital rotation into the ETF. BTC ETF inflows reached over $650M on the first day of launch, one of the highest values even in today's terms. Yet, as seen in the below chart, crypto related equities retained their value boasting positive returns 100 days after the ETF launch, in line with the crypto rally. This is with the exception of MARA and RIOT who suffered from the BTC halving.

There is a link between BTC spot returns and the spot returns of crypto equities as high correlations between their returns suggest. However Crypto-related equities do not provide a 1-1 exposure with the underlying spot of the crypto they’re exposed to and neither need to due to the introduction of the BTC and ETH ETF in Jan 2024. This can be seen in the drastic return profile difference between the top two corporate BTC holders. While BTC itself has delivered a ~75% return on its spot price, MSTR incredibly outperformed at ~140% while MARA majorly underperformed at ~−8%.

Crypto-exposed equities are evaluated using additional fundamental metrics beyond treasury holdings. This includes operating expenses, business specific risks, such as the bitcoin halving for miners and the influence of management control. These are factors that do not apply in the same manner within decentralised crypto markets. Therefore, while crypto token returns are not reliable indicators of long-term performance for crypto-exposed equities, their strong 30-day correlation with BTC suggests that token prices do significantly influence short-term equity price movements.